Regional, sub-regional and local Gross Value Added estimates for London, 1998-2017

In December 2018, the Office for National Statistics (ONS) released provisional estimates of regional, sub-regional and local gross value added (GVA) for 2017[1] and updated historic data from 1998. This supplement presents the main London findings from this release.

Using the balanced approach GVA(B), London’s total GVA was above £425 billion in 2017, up 3.0% in real terms on 2016. GVA(B) became a national statistic in November 2018, meaning that its methodology has been assessed by the Office for Statistics Regulation as fully compliant with the Code of Practice for Statistics. This approach takes both the income approach (GVA(I)) and the alternative production approach (GVA(P)) to measuring the economy and combines them into a single estimate which allows for more granular breakdowns and for the data to be presented in constant prices.

In 2017, London’s GVA(B) accounted for 23.8% of the UK’s total output – the largest share of the historic series which started at 19.2% in 1998 -. London was also the region with the highest GVA(B) per workforce job – the usual measure of labour productivity – in the UK at £72,371 for the same year, 41.1% higher than the UK average which was £51,297.

As can be observed in Figure A1, over two-thirds of London’s GVA(B) was produced in Inner London in 2017, with Inner London – West alone accounting for 44.4% of the total. Indeed, Inner London – West had a higher GVA(B) than all UK regions or nations except for the South East (and of course, London). Inner London – West also saw the greatest change in its relative importance to London’s economy having previously accounted for 39.5% of London’s GVA(B) in 1998. The increase in Inner London – East was only 2 percentage points. In contrast, all parts of Outer London declined in importance by 2-3 percentage points compared to 1998.

Figure A1: Geographic breakdown of headline[2] real London GVA(B) 1998 – 2017

Source: Regional Accounts, ONS

Going into the more detailed geographical breakdown provided by the balanced approach data, Figure A2 shows that Westminster and the City of London were the local authorities (LAs) with the highest output in London in 2017 (£62.5 and £59.6 billion, respectively). Only these two LAs accounted for almost 29% of the total London GVA(B). By contrast, Haringey with £4.2 billion and Barking and Dagenham with £3.4 billion were the London LAs with the lowest GVA(B) in the same year.

Figure A2: Real GVA(B) by London local authority in 2017

Source: ONS

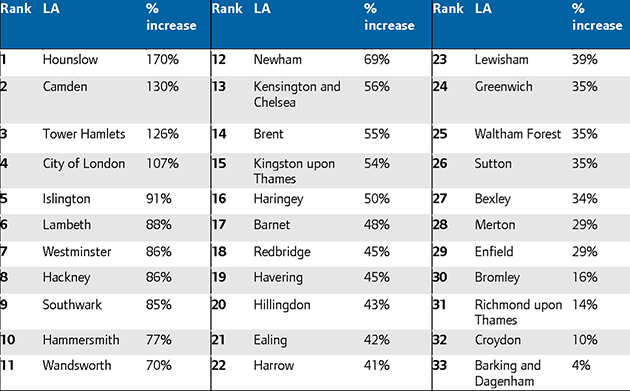

The real GVA(B) growth rates between 1998 and 2017 among the 33 London’s LAs are presented in Table A1. The fastest rates of real GVA(B) growth were seen in Hounslow and Camden at 170% and 130% respectively. In contrast, Croydon and Barking and Dagenham saw the slowest rates of real GVA(B) growth of 10% and 4%, respectively.

Table A1: Real GVA(B) growth rate of London’s LAs 1998-2017

Source: ONS and GLA Economics’ calculations

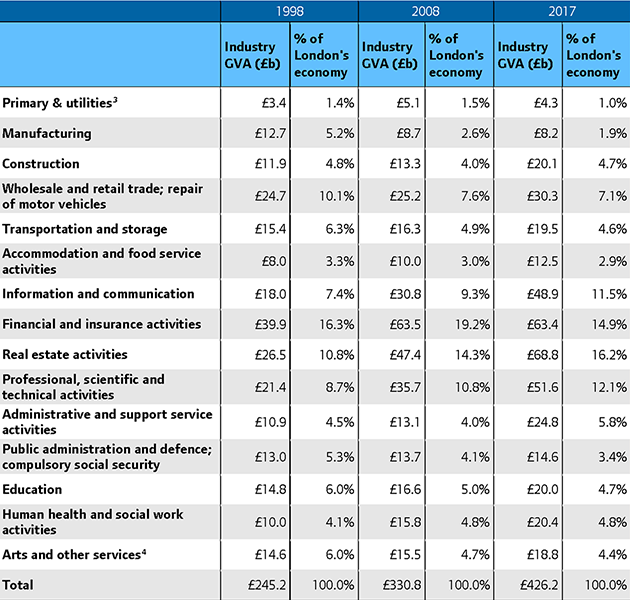

GVA(B) data by London sectors for the years 1998, 2008 and 2017 are presented in Table A2. In 2017, over 31% of London’s GVA was generated by the Real Estate activities (16.2%) and the Financial and insurance activities (14.9%) sectors combined, totalling £132.2 billion. The value of these industries represented 10.8% and 16.3%, respectively, of London’s total GVA(B) in 1998 indicating that Real Estate activities showed the largest increase as a share of the London economy between 1997 and 2018. Professional, scientific and technical activities and Information and communication industries have also played a larger role in London’s economy in the last decades, accounting for 12.1% and 11.5% of the output in 2017, respectively, compared to 8.7% and 7.4% of London’s GVA in 1998. In contrast, Manufacturing had the largest decrease from 5.2% in 1998 to 1.9% in 2017.

Table A2: Headline real GVA(B) in London by industry (£ billion and as per cent of total London GVA), 1998, 2008 and 2017

Source: Regional Accounts, ONS

The ONS GVA(B) data by industry also highlights predictable, major differences in sectoral spread between Inner and Outer London. In 2017, Manufacturing was concentrated in Outer London (accounting for 78.3% of all London’s manufacturing) while Inner London produced 95.3% of London’s GVA in Financial and insurance activities; 82.9% of Professional, scientific and technical activities; and 77.4% of the Information and communication output.

The above-mentioned analysis shows that London remains as the largest economy of any region or nation of the UK, with more importance than ever for the national economy. In 2017, London’s real output grew at a solid rate, continuing its historic upward trend. While, some industries such as Real estate; Information and communication; and Professional, scientific and technical activities especially contributed to this growth in the last decade.

If you found this overview of London’s output interesting further details on London’s economy can be found on our publications page.

[1] ONS, December 2018, ‘Regional economic activity by Gross Value Added (balanced), UK: 1998 to 2017’.

[2] UK includes Extra-Regio (which comprises compensation of employees and gross operating surplus which cannot be assigned to regions)

[3] This includes the following sectors: Agriculture, Forestry and Fishing; Mining and Quarrying; Electricity, gas, steam and air conditioning supply; and Water supply, sewerage, waste management and remediation activities.

[4] This category includes the subsectors: ‘Arts, entertainment and recreation’, ‘Other service activities’, and ‘Activities of households’.