UK investment between 2000 & 2019: distinction with a difference

While it is true that the UK has been lagging many OECD (Organization for Economic Cooperation and Development) and most G7 countries in gross capital formation, the picture becomes more mixed and complex as one scrutinises national, international and regional data trends. This supplement will examine these issues from a UK context in more detail.

The role of investment as an integral component of GDP and long-term economic growth is hardly in question. Many economists have pointed to the UK’s poor economic productivity since the 2008 Financial Crisis as a principal reason behind the country’s failure to sufficiently boost its people’s living standards since. This is hardly controvertible, as is the fact that the UK’s most productive regions (e.g., London) have experienced lower productivity growth since 2010 than most other (less) productive regions of the country, which does not bode well for national productivity growth in the near future.

UK Gross Fixed Capital Formation

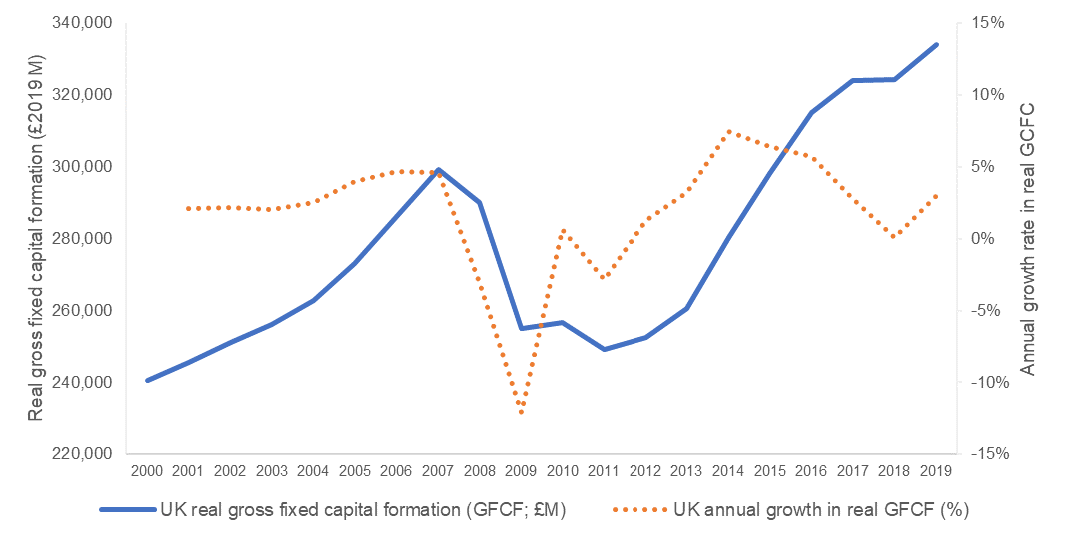

Amongst the many explanations provided for the feeble levels of productivity growth, one concerns chronic underinvestment in the UK. Figure A1 shows that annual growth rates of real gross fixed capital formation (GFCF) in 2019 were barely as high as they were in the early 2000s just before the 2008 global financial crisis, with annual growth decreasing since 2014 and that decrease generally picking up momentum since 2018.

Figure A1: UK real GFCF and annual growth rate

Source: Office for National Statistics

It took nearly two decades for GFCF levels to grow by just under 40%.

UK Business Investment

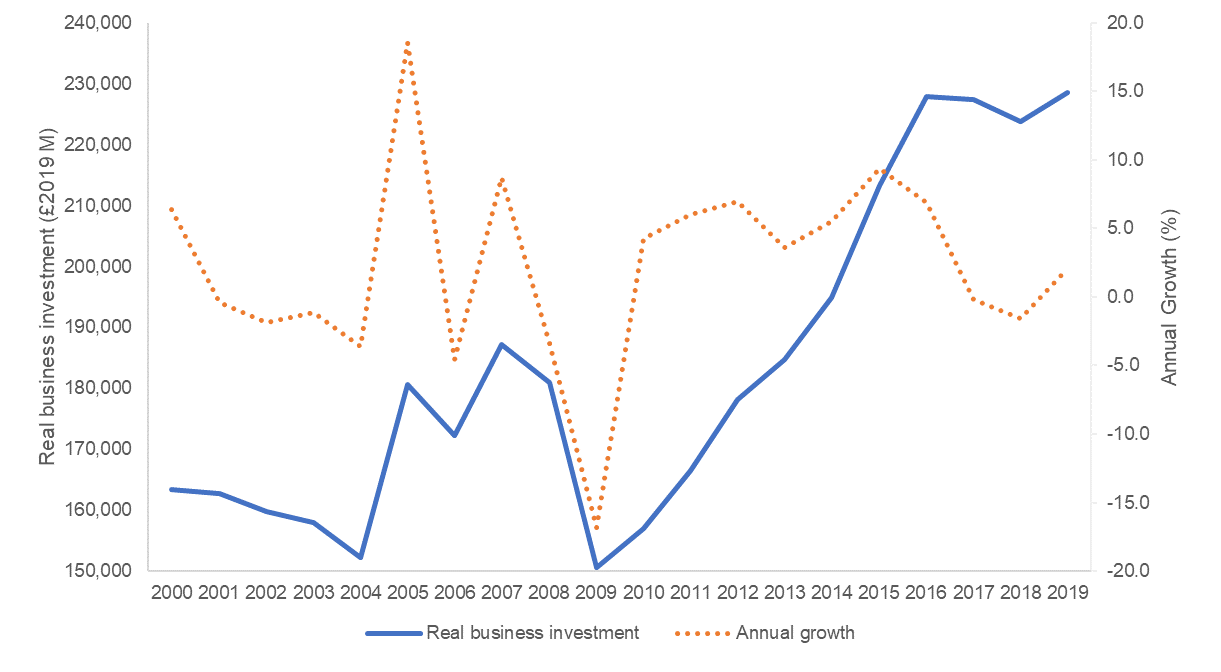

It is important to note that GFCF does not capture total investment. For example, it only accounts for the net amount added to an asset. Moreover, it includes fixed assets and hence excludes items such as financial assets, stock inventories, and land transactions. Therefore, while GFCF reliably captures a significant component of total investment in an economy, it should not be treated as synonymous to total investment.

Therefore, Office for National Statistics (ONS) data on business investment provides another useful indicator of UK investment performance. Figure A2 shows real business investment and annual growth over the same period (2000-2019). As with GFCF, annual growth rates in business investment in 2019 were similar to those in the early 2000s, with rates again dropping since 2015 and that drop picking-up pace in 2016.

Figure A2: Real business investment and annual growth

Source: Office for National Statistics

UK Gross Capital Formation

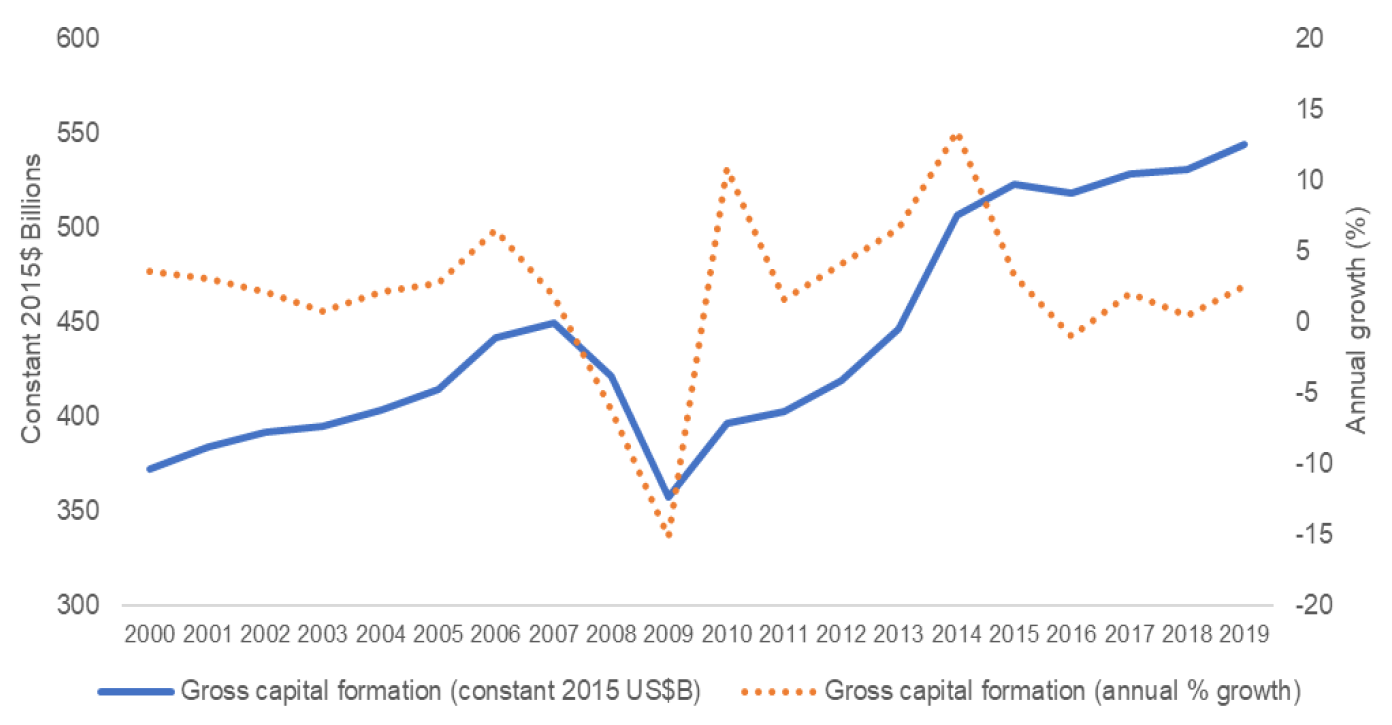

Going beyond GFCF to consider gross capital formation (GCF) as a whole does not change the trends much (Figure A3). Annual growth in 2019 was relatively feeble, and in fact slightly lagged that of the early 2000s. Here again, we notice annual growth getting relatively feeble around the 2015-2016 mark. It is also interesting to note that the UK’s GCF as a percentage of GDP in 2019 (18%) was exactly what it was in 2000 (18%). Over the entire two-decade period it ranged from 16% to 18%.

Figure A3: Real gross capital formation and annual growth

Source: World Bank

UK Investment vs. Comparable Countries

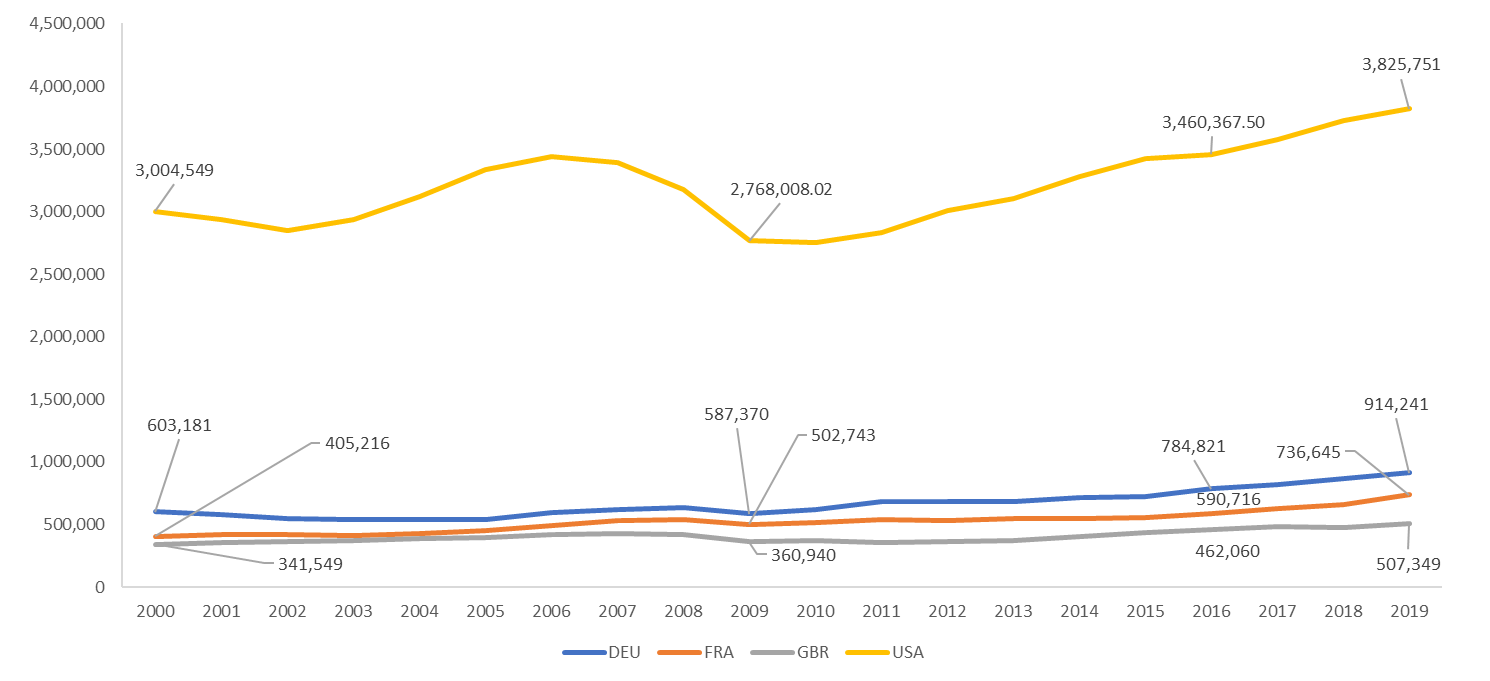

The picture becomes illuminating when looking at how the UK performs compared to other G7 and OECD countries[1].

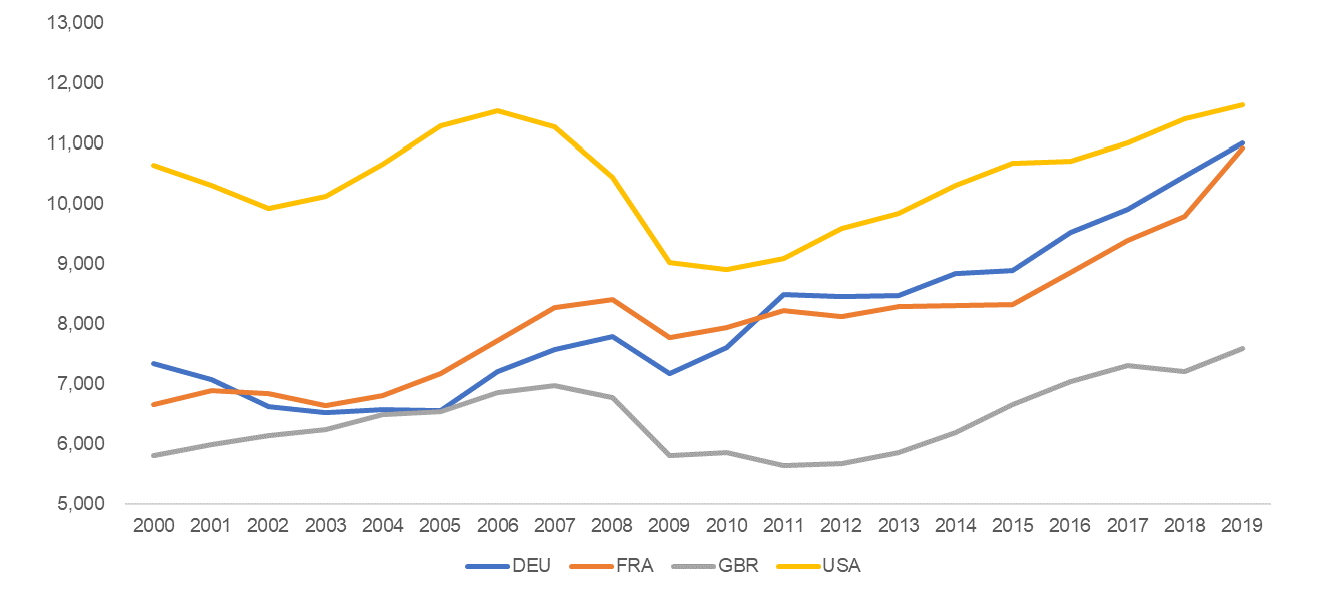

Figure A4: Real Gross Fixed Capital Formation by country – Real (2010), US dollar millions

Source: OECD and World Bank

Table A1: Percent change in real GFCF between 2000 and 2019 by country

| Country | Percent change in real GFCF (2000-2019) |

| UK | 48.5% |

| Germany | 51.6% |

| France | 81.8% |

| United States | 27.3% |

Source: OECD and World Bank

Figure A4 reveals that:

- The UK underperformed France, Germany, and the US on levels of real gross fixed capital formation throughout the bulk of this century.

- The gap between the UK and the other countries has grown even more over the past two decades, especially since 2008. By 2019, the UK’s total GFCF represented just under 70% (compared to over 84% in 2000) of France’s and 55% of Germany’s (compared to 57% in 2000).

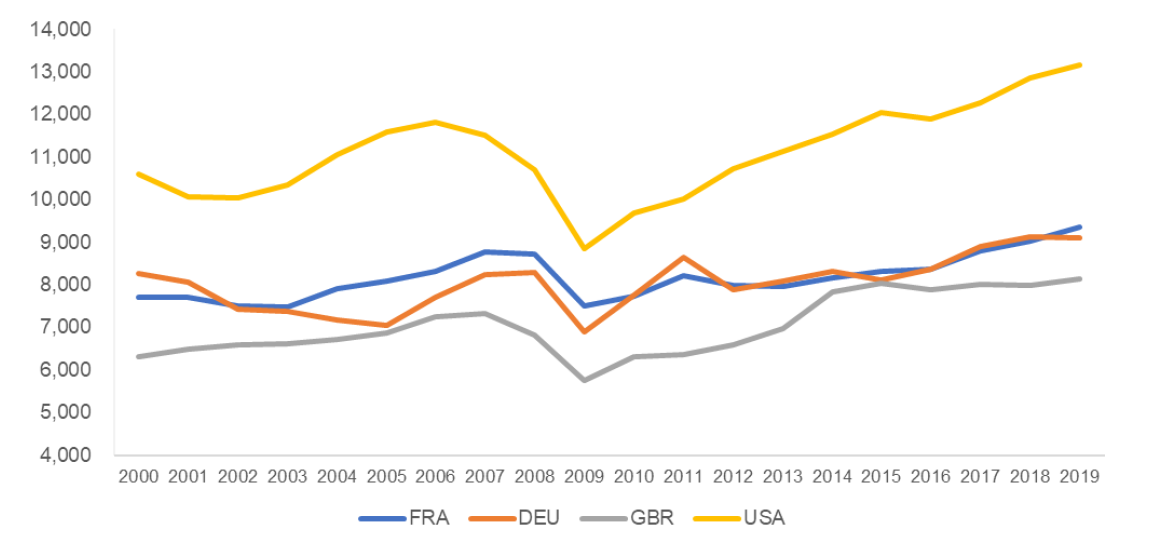

The UK’s underperformance is clear when accounting for real GFCF per capita (Figure A5). By 2019, the UK’s real per-capita GFCF represented less than 70% of both France’s and Germany’s. It is worth noting also that the gap with France and Germany has widened over the course of the two decades. Figure A6 reveals a similar trend when looking at real gross capital formation per capita.

Figure A5: Real GFCF per capita by country

Sources: OECD and World Bank

Figure A6: Real gross capital formation per capita by country

Source: World Bank

The picture becomes more interesting when looking at real GCF growth across different periods over the past two decades (Table A2). As can be seen, UK real GCF outgrew that of the US, France and Germany across the first two decades of this century, and in fact GFC growth in the UK outpaced both Germany’s and France’s from the Great Recession to 2019. The weakness in UK investment growth commences around 2016; growth over the three subsequent years lagged all three countries and by quite a margin.

Table A2: Real GCF of the US, France, Germany and UK, 2000-19

| 2000-19 | 2008-19 | 2016-19 | |

| USA | 44.4% | 32.8% | 12.4% |

| GERMANY | 11.4% | 11.2% | 10.0% |

| FRANCE | 34.1% | 12.2% | 12.8% |

| UK | 46.1% | 29.2% | 5.0% |

The picture is more or less replicated when looking at growth in real GCF per-capita (Table A3).

Table A3: Real per capita GCF of the US, France, Germany and UK, 2000-19

| 2000-19 | 2008-19 | 2016-19 | |

| USA | 24.1% | 23.0% | 10.6% |

| GERMANY | 10.2% | 9.9% | 9.0% |

| FRANCE | 21.2% | 7.2% | 11.7% |

| UK | 28.7% | 19.4% | 3.1% |

In sum, between 2000 and 2019, the UK experienced bigger growth in real GCF per-capita than the other three countries despite experiencing lower productivity growth. However, from 2016 to 2019, the UK’s real GCF per-capita growth was considerably lower than all three countries.

Several reasons could explain the weakening growth of the UK’s GCF since 2016. Part of the reason could be the outcome of the Brexit referendum and the ensuing political uncertainty resulting from it. Recent reports and analyses link that decision to poor aggregate investment (both domestic and foreign) as a result of the political and economic uncertainty that ensued following the referendum (see GLA Economics (2024), Cambridge Econometrics (2024) and NIESR (2023) for examples).

However, the Brexit referendum result by itself cannot fully explain what can perhaps be termed ‘structural challenges’ related to the nature of investment in the UK. Figures A7-A9 break down GFCF in the UK, France, Germany and the United States by ‘investment source’.

Figure A7: Household investment as a % of GFCF by country

Source: OECD

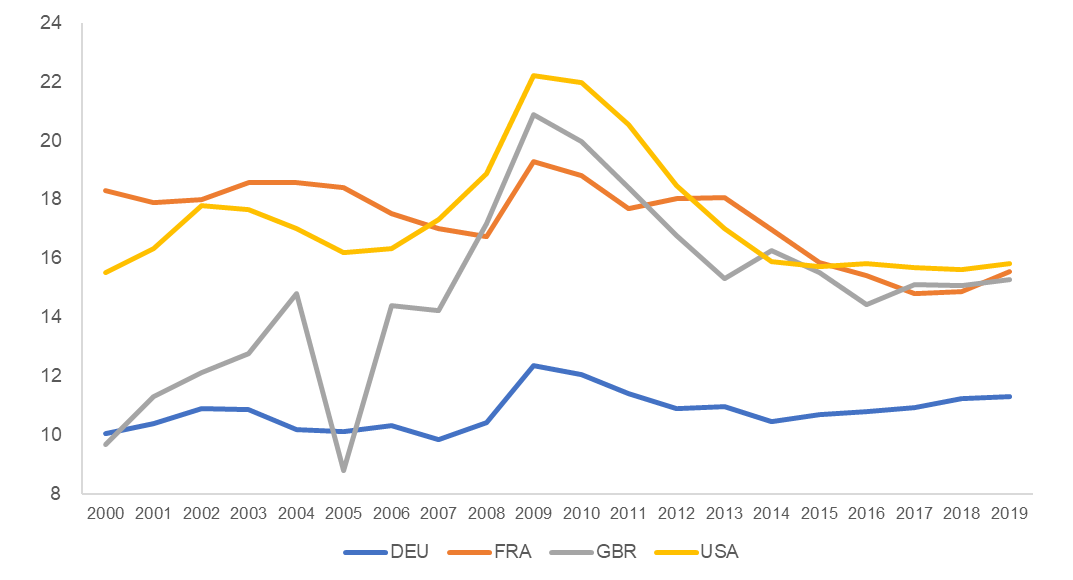

Figure A7 shows the value of acquisitions of new or existing fixed assets by households as a percentage of total GFCF. Back in 2000, UK households contributed just over a fifth of the country’s GFCF, compared to about a third for Germany and the US. While this gap has narrowed down as UK households started investing more in new or existing fixed assets, the country still lags other countries (notably Germany and the US) on that front.

Figure A8: Government investment as a % of GFCF by country

Source: OECD

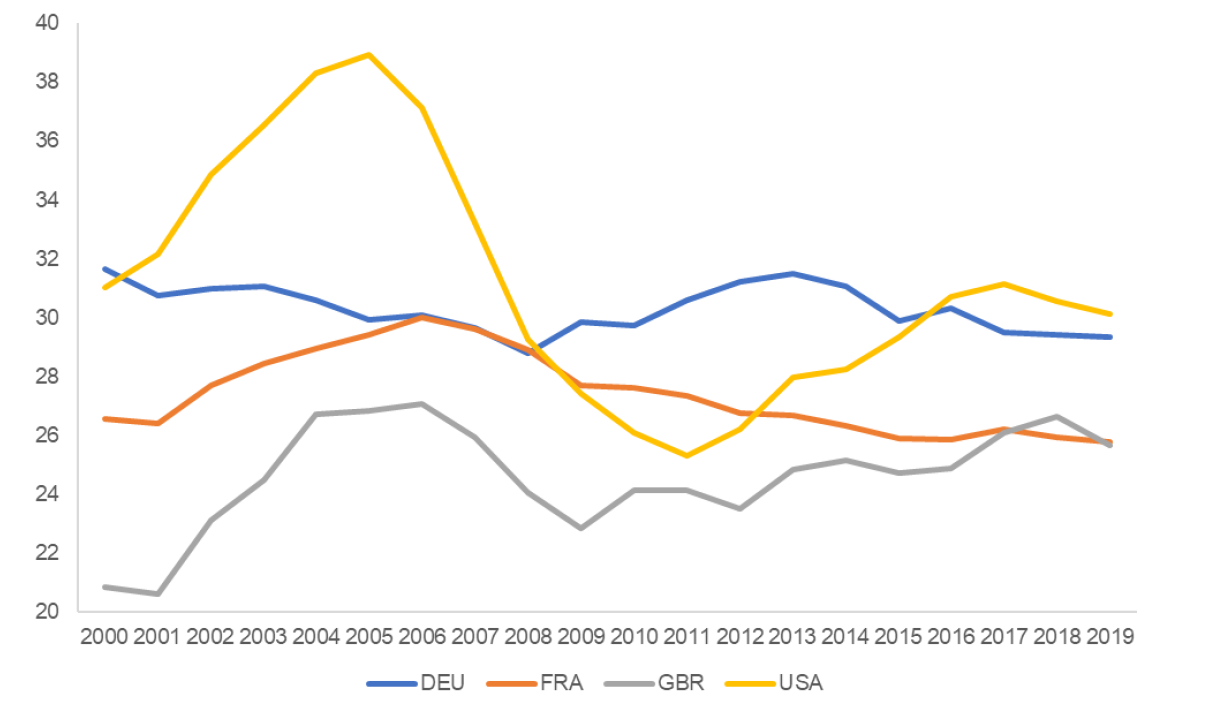

Figure A8 looks at government investment (which includes investment in R&D, military equipment, transport infrastructure and civil infrastructure such as hospitals and schools) as a percentage of GFCF. Interestingly, the UK nearly doubled the share of government expenditure in GFCF during the 2000s, before dropping by over 5 percentage points during the 2010s. By the time of the 2008 Financial Crisis, the UK’s share of government investment in GFCF was only exceeded by the US. By 2019, it lagged both the US and France.

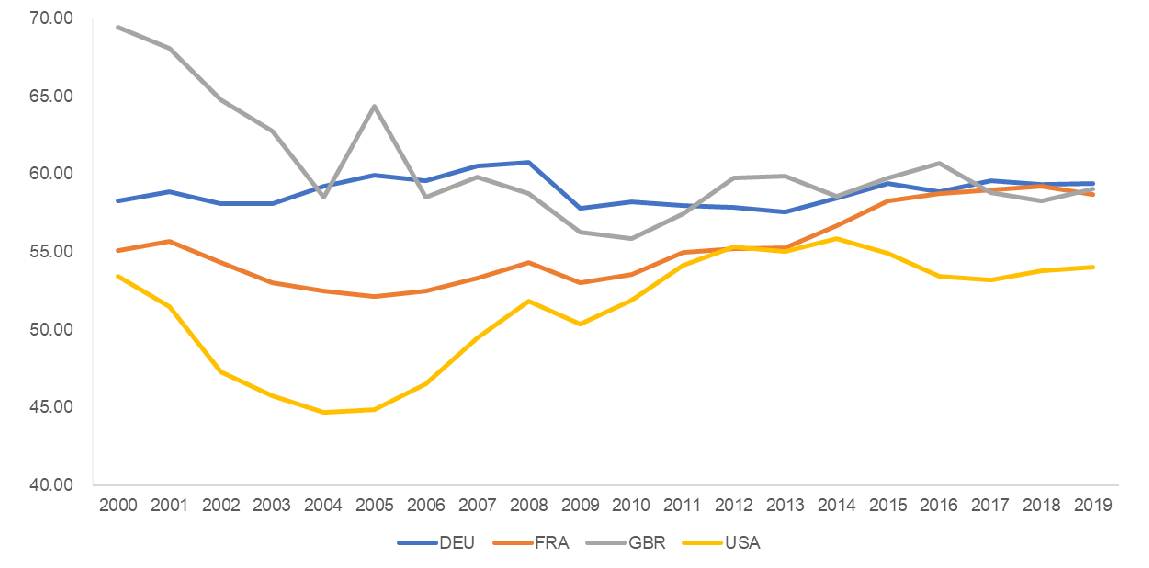

Figure A9: Corporate investment as a % of GFCF

Source: OECD

Figure A9 looks at corporate investment’s share of GFCF by country, where corporate investments tend to represent the largest share of GFCF. In 2000, 70% of the UK’s GFCF came from corporate sources; by the financial crisis, it drops to under 60% and fluctuated around the 60% mark ever since. In 2019, only Germany had a larger share of corporate investment.

What Figures A7-A9 collectively show is that traditionally, the UK has been more reliant on corporate and government investment for its total GFCF stock than most countries in the above sample as well as the OECD average; in 2019, 75% of the stock came from these two sources, compared to 70% in the US, 71% in Germany, and 74% in France. Stated differently, the sources of GFCF investment in the UK are slightly less diversified than they are in other OECD countries, which could suggest a greater sensitivity of its investment flows to fiscal/budgetary realities and geopolitical situations. That is also not so surprising when we consider the fact that the UK is a relatively open economy that is much more integrated globally than most other OECD countries (including Germany and France).

Forecasts of future gross fixed capital formation: UK vs OECD countries

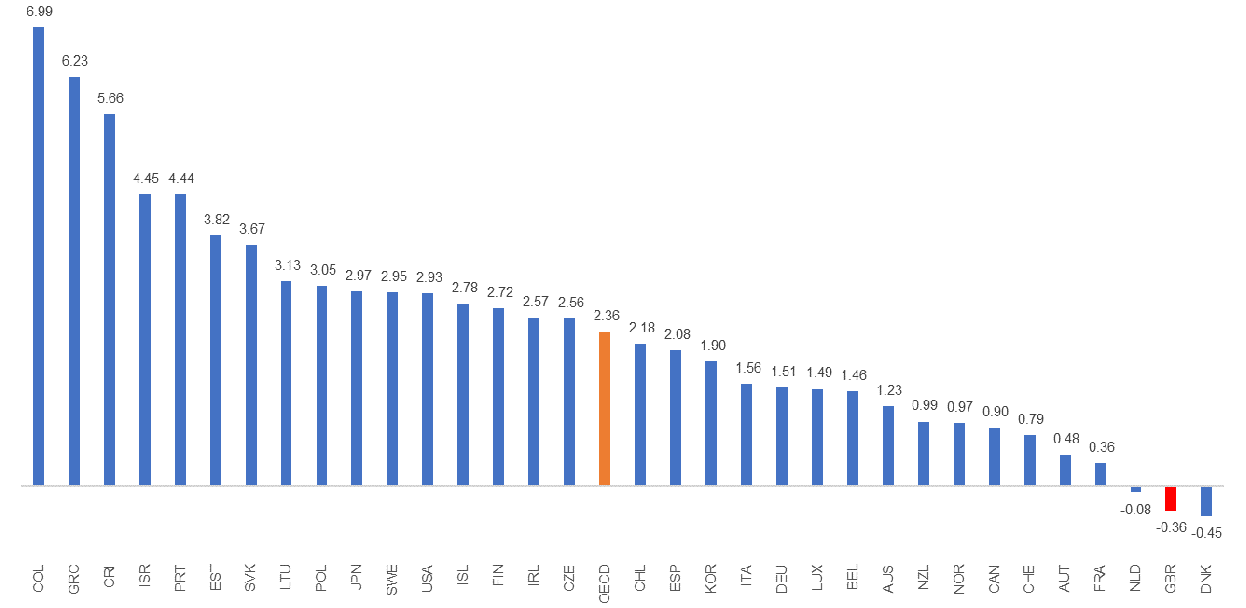

OECD forecasts of gross fixed capital formation by quarter paint a worrying picture for the UK (Figure A10).

Figure A10: Average quarterly GFCF growth forecast by OECD country (Q1 2024 – Q4 2025)

Source: OECD

The UK’s average quarterly growth in GFCF from Q1 2024 to Q4 2025 is expected to be -0.36%, which is nearly 3 percentage points worse than the OECD average and is bettered by all other countries except Denmark.

Similarly ominous forecasts for UK investment were made by the Office for Budget Responsibility (OBR) in its March 2024 Economic and Fiscal Outlook (see Table A4):

Table A4: Annual forecast of percentage change in investment parameter (%)

| 2024 | 2025 | 2026 | 2027 | 2028 | |

|---|---|---|---|---|---|

| Fixed business investment | -5.1 | 1.4 | 2.5 | 2.0 | 1.2 |

| Fixed general government investment | -1.5 | -2.4 | -2.0 | -2.0 | -3.0 |

Source: OBR

Curiously, the OBR forecasts that government investment, whose share in total UK GFCF has already dropped substantially over the past decade, will continue to decrease, while growth in fixed business investment will remain relatively modest. On that basis, a rise in GFCF would require a noticeable rise in share of household fixed investment as a percentage of GFCF, which on present trends seems unlikely in the short-to-medium term.

Summary and concluding thoughts

In this supplement looking at investment in the UK and London, we focussed on the broad and general trends underlying investment in the UK and how it compares to similar countries as well as the wider pool of OECD and G7 countries. In sum:

- In line with what many pundits and economists have been saying, measures of investment (whether gross fixed capital formation, business investment, or gross capital formation) reveal that annual growth has been weaker in recent years than in the 2000s, with that weakness exacerbating since 2016.

- Across the first two decades of this century, the UK underperformed France, Germany, and the US on measures of real gross capital and real gross fixed capital formation (both on aggregate and per-capita).

- That said, the UK actually did not always underperform these countries. In fact, until the mid-2010s, the UK was generally outperforming these countries and most of the G7 and OECD on both aggregate and per-capita measures of investment. The underperformance begins from 2016 onwards.

- While the Brexit referendum added to the uncertainty that undermined investment, there are other factors behind this malaise- one of which is the UK’s overreliance on certain sources of investment that are themselves sensitive to political and economic uncertainty (e.g., corporate investment) than many OECD countries. There are other reasons of course, and those will be covered in upcoming articles.

The last section revealed rather worrying forecasts for investment in the UK on current trends. This makes it all the more necessary to invest more effort into analysing this issue in greater detail.

[1] Henceforth, DEU in the charts refers to Germany due to OECD country nomenclature.