London’s Economy Today editorial – May 2023

London accelerates ahead of UK in latest growth data

Output growth in London was the fastest in the UK, according to the latest regional GDP figures from the Office for National Statistics (ONS). And while the data only run to Q3 2022, more recent figures suggest the capital continues to grow ahead of the rest of the country.

London’s GDP was growing at a pace of 6.8% year-on-year in autumn 2022, by far the fastest pace of any region in England or UK nation. In a sharp contrast, the wider UK economy contracted in Q3 2022. And London’s output has now recovered to 4.4% above its pre-pandemic levels, while national GDP was still nearly 1% below its Q4 2019 levels (Figure 1). Taking an average across the year to Q3 2022, London’s growth was close to 10%, again by far the fastest of any region or nation.

Figure 1:

The biggest contributions to London’s quarterly growth came from IT, Retail and Restaurants & hotels, while Real estate, Education and Finance dragged on output. Despite the cost of living crisis, London’s consumer-focused services continued to recover strongly late last year. And some of London’s core business-focused sectors were also performing well, with even the drop in Finance output coming after strength in previous quarters. Meanwhile, goods sectors and Real estate are struggling for momentum as interest rates rise and costs for inputs and building materials remain very high.

London is a very unequal city, and the poorest Londoners are still facing stark challenges from the rising cost of essentials. Yet, it always seemed likely that London would be more resilient than the rest of the UK to the cost of living crisis. At the macroeconomic level, higher average incomes, lower average spending on energy, a robust labour market and more confident consumers and businesses have kept the capital growing. The wider UK economy has seen low, but positive, growth in the quarters since. Data released this month showed UK GDP rising 0.1% for the second quarter in a row in Q1 2023.

Meanwhile London data for the months since last autumn are also encouraging. The city’s workforce jobs have continued to grow ahead of the national average (see below). Consumer confidence in London has consistently been less pessimistic than the national average. Indeed, May’s figure saw Londoners push into positive territory for the first time since December 2021, so consumer-facing sectors should remain more resilient in London than at the UK level. More broadly, businesses are also expecting continued growth, with the May Purchasing Managers’ Index (PMI) surveys showing London as the fastest-growing region.

Looking forward GLA Economics will release fresh forecasts for London’s economy next month with our next London’s Economic Outlook report.

Bank of England and IMF raise growth projections, but expect higher inflation for longer

At the May meeting of the Monetary Policy Committee (MPC), the Bank of England revealed it now expects the UK to avoid a recession. But this positive news was tempered by projections that inflation will now stay higher for longer, and markets now expect higher interest rates.

The Bank of England raised the official policy interest rate to 4.5% in May, from 4.25% in March. In their Monetary Policy Report, policymakers cautioned that while they see inflation falling rapidly this year, they expect price growth to hold above the 2% target until 2025. But still-climbing food inflation and strong wage growth are starting to feed through into medium-term inflation forecasts. Based on their ‘fan chart’ of probabilities around the central forecast, the Bank thinks there is nearly a one in three chance that inflation will be above 4% by the end of 2024. And policymakers estimated a nearly 50% probability of inflation staying above 2% by mid-2026.

Two members of the MPC, Swati Dinghra and Silvana Tenreyro, disagreed with the decision. They voted to hold rates at 4.25%, observing that the effects of previous rate rises will not have had their full effect on the economy yet. In this light, further hikes now could risk squeezing the economy too far.

Even the improved news on the Bank’s output projections looks weaker on close inspection. The Bank expects the UK economy to expand just 0.4% on average this year, followed by 0.7% and 0.8% in 2024 and 2025 respectively. And the latest projections place the Bank quite close to average forecaster expectations for next year. This is a troubling sign of wide agreement that the cost of living crisis, and the delayed effects of higher interest rates, may yet drag on the UK’s medium-term prospects.

The International Monetary Fund (IMF) also released new, stronger growth forecasts for the UK economy this month. Releasing their annual UK country report, the IMF projected that the UK would now avoid recession and see positive growth across 2023. In annual terms, the IMF expects 0.4% growth this year, then 1% in 2024 and averaging 2% growth in 2025 and 2026. While offering a more optimistic medium-term growth forecast than the Bank of England, the IMF echoed their concerns around higher inflation. At the same time, the IMF cautioned that “elevated uncertainty about the macroeconomic outlook and inflation persistence merits continuous review of the pace and magnitude of monetary tightening”.

Pace of inflation down, but food concerns come to the fore

Inflation decelerated to single digits in April, but the cost of living crisis is far from over. ONS figures showed Consumer Price Index (CPI) inflation slowing to 8.7% year on year last month, down from over 10% in March. Under the headline, many important drivers of inflation are now easing, with prices for energy, food and hotels & restaurants all posting slower growth in April. However, some core parts of the spending basket are still accelerating, with inflation excluding food and energy reaching a new 31-year high of 6.8%.

Figure 2:

The contribution from energy shrank abruptly, but this was because the annual comparison is now the much higher April 2022 Ofgem price cap. While household energy costs are still the same as last October, they are set to fall later this summer. Ofgem confirmed today that the price cap will fall to levels consistent with annual average household bills of just under £2,100. Analyst projections suggest that the cap may remain close to this level in October, but wholesale gas prices have fallen to levels not seen since summer 2021.

Even as the energy squeeze loosens, the pace of food inflation is a stark reminder of the pressure still faced by households. Prices for food grew 19.3% year on year in April, ticking down only slightly from 19.6% in March. While several core staples such as bread, milk, cheese and eggs saw inflation slow, the squeeze from food bills is still tight. And across the UK, recent ONS polling shows that more households may now be concerned about paying their food bills than energy costs. Indeed, the Resolution Foundation recently released modelling analysis suggesting that by Q3 2023, 16 million households (56%) are set to face a bigger food than energy cost shock since 2019-20.

These trends will hit the poorest households the hardest, as food and energy both make up larger shares of spending at the bottom of the income distribution. As a result, the same analysis also found that “inflation is currently more bottom heavy than at any point on record”. Most troublingly, ONS polling has also found that 61% of the poorest fifth of the UK population are cutting back on food and other essentials – compared to 35% in the richest fifth. GLA-commissioned polling shows that just under one in ten Londoners (9%) are going without essentials. But this rises to one in four (25%) among Londoners who are ‘financially struggling’. For as long as the price of core essentials remains so high, the cost of living crisis will still take a toll on the poorest Londoners.

Global central banks continue to raise interest rates

Internationally interest rates have also continued to rise in both the Eurozone and US over the past month. The European Central Bank (ECB) increased rates in the Eurozone by 0.25 percentage points (pp) to 3.25% in May, although this was a smaller increase than previous increases in the rate. However, Christine Lagarde, the president of the ECB, indicated that rate rises would continue with her noting that “we have more ground to cover and we are not pausing, that is extremely clear”. The Federal Reserve in the US also increased interest rates in May. Its Federal Open Market Committee increased its target rate by 0.25pp to a new target range of between 5% and 5.25%. However, the Fed softened its messaging around future rate rises. Thus, after this increase it observed that it was “determining the extent to which additional policy firming may be appropriate”, whereas after the previous increase in March it had said it “anticipates that some additional policy firming may be appropriate”. This was supported by the Fed’s chair, Jay Powell, who said that “there is a sense that we’re much closer to the end of this than to the beginning”.

The recent problems at banks also continued into late April and the beginning of this month with another bank, First Republic, getting into trouble before it was taken over by JPMorgen. Looking at these recent banking sector problems the Federal Reserve has warned that they could lead to banks cutting back on credit which would slow the economy. They observed that “a sharp contraction in the availability of credit would drive up the cost of funding for businesses and households, potentially resulting in a slowdown in economic activity” in the US.

Mixed signals in London’s labour market

Data published by the ONS this month showed a mixed picture for London’s labour market. Thus, in positive news the capital’s inactivity rate was down on both the year and the quarter, while the employment rate is up. London’s inactivity rate (the measure of those not looking and/or not available to work) was estimated at 20.9% in the three months to March 2023. This was down 0.5pp on the previous quarter and down 0.2pp on the previous year, and is similar to the UK-wide estimate of 21.0%. The employment rate in London was estimated at 75.4% for the three months ending March 2023, up 0.3pp on the previous quarter and up 0.1pp on the same period in the previous year. Although, London’s employment rate remained lower than the UK average (75.9%).

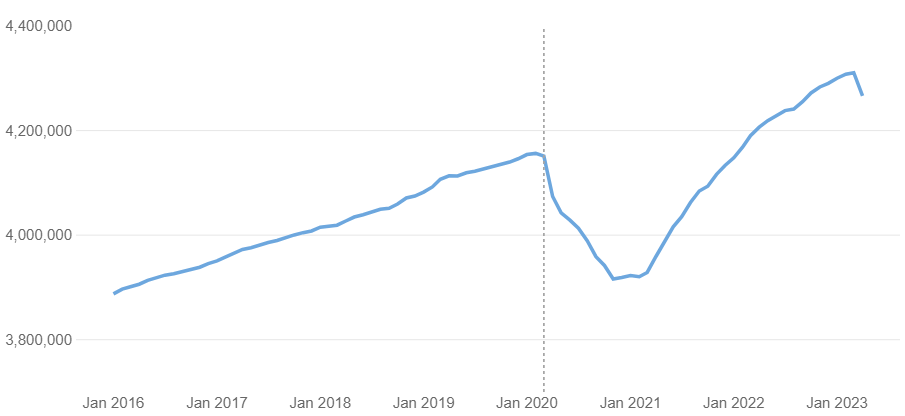

However, other measures of London’s labour market showed a more concerning picture with the unemployment rate estimated at 4.7%, which was up 0.2pp on the quarter although unchanged from a year earlier. London’s unemployment rate remains above the UK’s which stood at 3.9%. Payrolled employees also fell sharply in the capital between March and April 2023 after growing for the previous 26 months (Figure 3). Thus, payrolled employees decreased by around 44,600, or 1.0%, in London between March and April 2023 but still saw an increase of 1.4% on the year. Further, although all UK regions recorded a decline in this measure London saw the largest fall of all regions, and the number of employees living in the capital is now below the count recorded in October 2022. It should however be noted that this measure is often subject to sizeable revisions by the ONS so this decline may later be reversed to some extent.

Figure 3: Payrolled employees in London Latest data for April 2023

Source: HM Revenue and Customs Pas As You Earn Real Time Information; Note: Estimates are based on where employees live. March 2020 indicated by dotted line.

GLA Economics will continue to monitor London’s economy over the coming months in our analysis and publications, which can be found on our publications page and on the London Datastore.