London macroeconomic scenarios (June 2022 update)

GLA Economics published its latest macroeconomic scenarios-based forecast for London on 21 June. These scenarios have formed part of wider work on the impact of the COVID-19 pandemic on London’s economy, and they have been informed by expert consultation and existing literature on pandemics and macroeconomic scenarios[1]. The two main outcome variables are real Gross Value Added (GVA) – a measure of London’s output – and workforce jobs (WFJ) – a measure of employment. We project both variables over the medium term (to the end of 2024) and we also project GVA over the longer term (to 2032).

In this context, we have developed three main macroeconomic scenarios for London founded on three sets of plausible narratives for the economy.

- Fast economic recovery (an optimistic but plausible scenario)

- Gradual return to economic growth (the GLA Economics baseline reference scenario)

- Slow economic recovery (a plausible pessimistic case)

These scenarios are not definite predictions about the only possible paths for the economy, nor do they necessarily incorporate optimal policy responses. Instead, they rely on judgements around several key assumptions. While previous scenario updates have focused on the public health and economic support response to COVID-19, focus is now shifting to broader questions on resilience to shocks and policy support[2]. The scenarios also do not capture the full range of uncertainty about the future, which is likely to be much wider.

Within this framework, we can set out the narrative and key results of the main scenarios. Scenario 2 is our baseline, involving a gradual return to economic growth. Following last year’s rapid recovery, this scenario is more cautious around the pace of growth from the second half of this year. With inflation at a 40-year high, this will squeeze real household incomes and consumer demand is likely to slow. As a result the economy still faces a spell of weak growth in late 2022 and early 2023 in our baseline forecast. However, we do not expect an outright recession in our baseline. This assumes that there will not be a further significant outbreak of COVID-19 with an adverse effect on the economy.

London’s lowest-income households may be particularly vulnerable to the cost-of-living crisis, with the capital having a higher poverty rate after housing costs than the rest of the UK. There is some evidence to suggest that London’s prices are rising faster than in other regions[3]. However, for a macroeconomic assessment, it remains important that London has higher average incomes than the rest of the UK and that London’s consumers are currently less pessimistic in confidence surveys. As a result, we have not cut our forecast by as much as the downgrade to the outlook in the Bank of England’s May Monetary Policy Report. However, that does not mean that the recovery will be straightforward from this point. Customer-facing sectors likely face a stark challenge in some of the quarters ahead – even if their annual growth rates are flattered by the strong recovery in 2021. And our forecast now sees it taking ten years for London’s output to return to levels consistent with the pre-pandemic trend.

Scenario 1, a plausible upside, involves a faster economic recovery. In this scenario, we assume London’s stronger aggregate incomes compared to the rest of the UK offer a buffer against inflation as richer households spend more of their pandemic savings. This is helped by the current level of fiscal policy support, which proves sufficient to meaningfully protect aggregate incomes. We also assume that still-positive business sentiment keeps labour demand firm, which means that tightening macro policy does not dampen the employment recovery. The boost to demand raises output and employment, prompting stronger business investment and mostly eliminating the medium-term output scarring in our baseline.

Scenario 3, a plausible downside, assumes that London slips into recession later this year. The drag on real incomes is going to hit the lowest-income households the hardest. But lower-income households also tend to spend more of their income, so this could prove critical for the overall demand picture. Yet despite weakening growth, the Bank of England is forced to take an aggressive approach to monetary policy tightening as global inflation pressures continue to climb. Amid slowing demand, higher borrowing costs and rising input prices, businesses hold back on investment and hiring plans. Taken together, these trends mean London’s output contracts across H2 2022 and early 2023, and job growth grinds to a halt. A fresh downturn and slow medium-term growth mean there is significant economic scarring, some of which persists in the long term, as firms close and workers lose their jobs.

Figure A1:

Figure A2:

Overall, while the medium-term paths for output and employment are mostly

higher now than expected at the peak of the crisis, the balance of risk is clearly

skewed to the downside. The downside potential for London’s economy is

significant, with GVA in the slow recovery scenario ending 2024 nearly 4% below

the baseline, while the upside ends 2023 just under 2% above baseline. The wide

gap between scenarios also demonstrates the high uncertainty around economic

conditions. While our baseline remains cautiously optimistic about the

recovery, the broader picture of our scenarios for London’s economy is more

subdued.

The main results are presented below:

Headline recovery in the medium term (2022

to 2023)

- Under the gradual return to economic growth scenario, our baseline, London’s real GVA is expected to grow by 4.5% this year. This is a firm pace of growth, but lower than December’s 5% forecast, and sharply down from 2021’s estimated growth of 8.5%. Weak demand in the second half of 2022 and early 2023 mean growth will slow sharply in 2023 (1.6%), before recovering a little in 2024 (2.3%) (Figure A3).

- Real GVA likely already reached its pre-crisis level in Q4 2021 (Figure A1), while workforce jobs only reach pre-crisis levels in mid-2023 in the baseline (Figure A2).

- Jobs will take longer to feel the impact of the recovery. After ticking up 0.3% last year, employment is set to see moderate growth this year (2.2%), before slowing in 2023 (1.1%) and maintaining a similar pace in 2024 (1.2%) (Figure A4).

- Under the fast economic recovery scenario, demand would remain resilient, though momentum is still weaker next year. In this scenario, output would rise 5.4% this year, before easing closer to long-term averages at 2% growth in 2023 and 2.6% in 2024. Employment would also see a firmer rebound this year, with growth of 2.6%, followed by a convergence to baseline growth rates from next year.

- In the slow economic recovery scenario, output faces a double-dip recession. GVA grows 3% in 2022, before a recession late this year and into 2023 means next year output averages at a 0.2% drop. Output growth then converges to its long-term pace at 1.9% in 2024. Jobs follow a similar pattern, with growth of 1.7% in 2022, just 0.4% in 2023 and 1.2% in 2024. These profiles do not return to pre-pandemic trends.

- GLA Economics projections had previously tended to become more optimistic for output and jobs over successive iterations of our forecasts/scenarios. But the latest iterations are seeing this trend reverse, especially in the later years of the forecast.

Figure A3:

Figure A4:

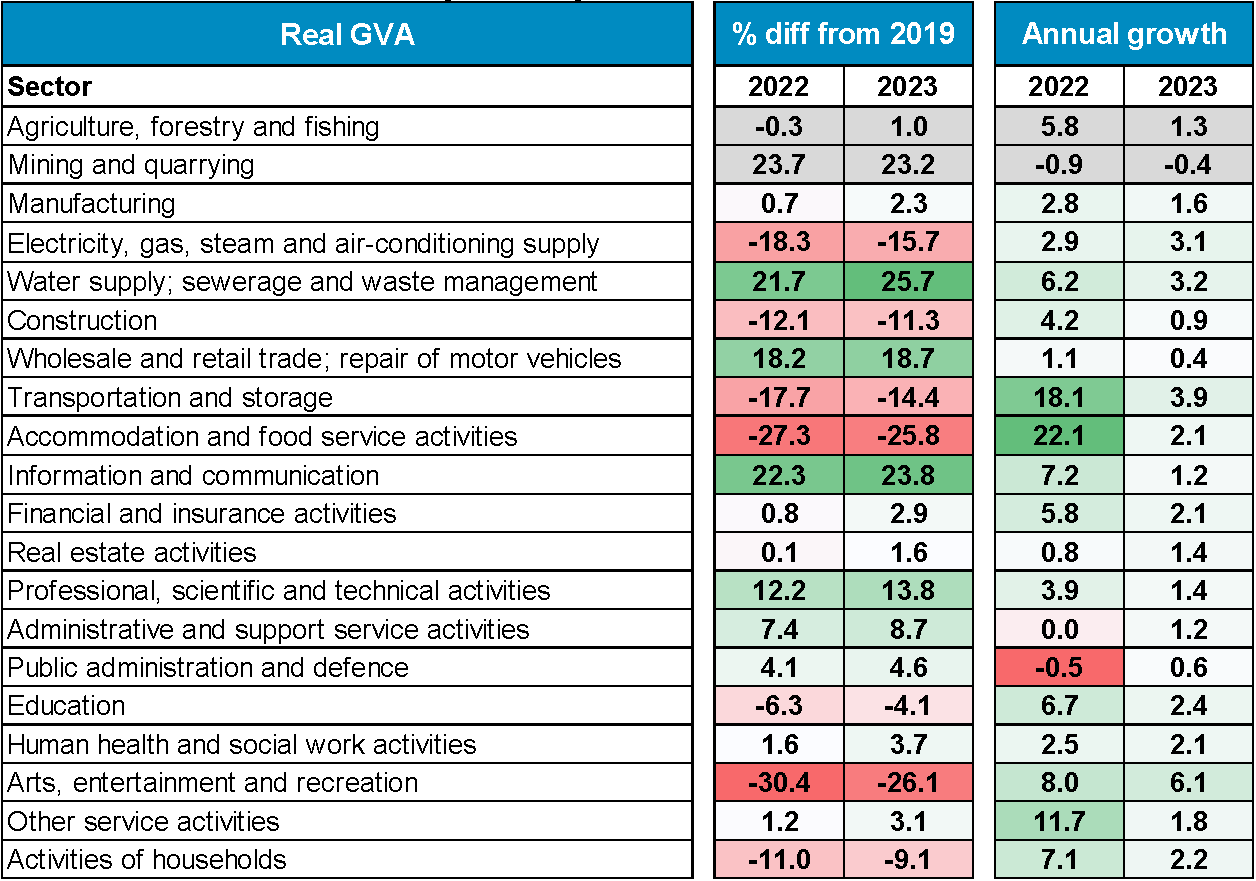

Sectoral output recoveries in the medium term (2022 to 2023)

- London’s economic recovery is set to vary widely across industries (Table A1).

- While we expect firm output growth in 2022 in much of the economy, the sectors most affected by the pandemic will see output remain below 2019 levels.

- Examples include Accommodation and food services, where output in 2022 will still be over 27% below 2019 levels, despite growing 22%. Transportation and storage and Arts, entertainment and recreation will also lag 2019 output in 2022 despite very strong growth, while Construction also faces an incomplete recovery.

- Other sectors are seeing firm growth despite reaching pre-pandemic output levels rapidly. This includes sectors that may have adapted faster to home working, such as Information and communication, Financial services or Professional services.

- While the consumer recovery continues in early 2022, Manufacturing does well out of the shift of consumer demand to goods from services during the pandemic.

- Wholesale and retail trade will see output remain well above pre-pandemic levels, but high inflation will pull growth well below the economy average this year and the sector will come close to a standstill in 2023.

Table A1: London’s real GVA by industry in 2022 and 2023

Source: GLA Economics. Note: colour coding shows the most negative results in red, the most positive results in green, and results in the middle in white. Primary industries are shaded in grey.

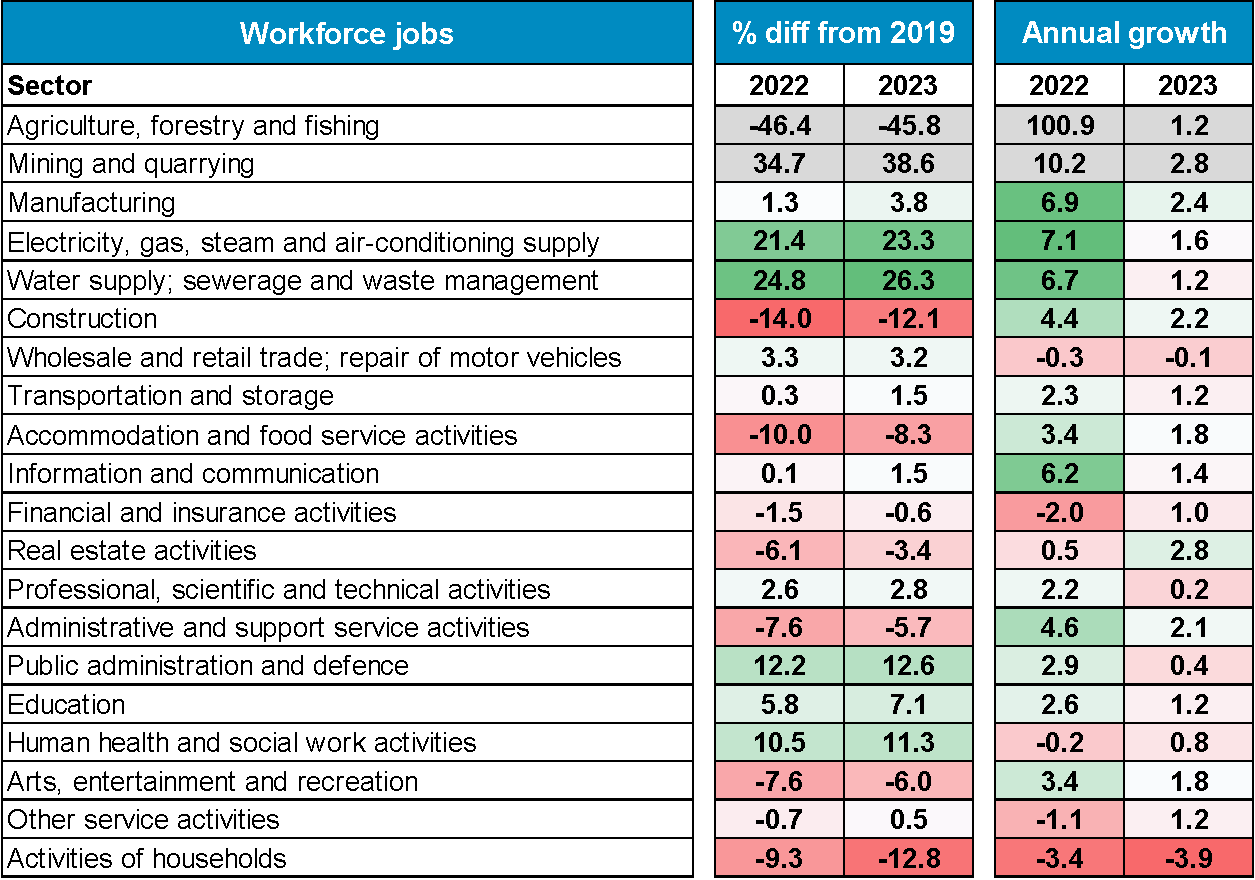

Sectoral employment recoveries in the medium term (2022 to 2023)

- Workforce job projections show that for a lot of sectors, London’s labour market recovery will still be incomplete this year (Table A2).

- Sectors hit hard by the pandemic are likely to take the longest to recover. This includes customer-facing service sectors like Accommodation and food services and Arts and entertainment, which now face headwinds from squeezed real incomes.

- Wholesale and retail trade jobs are set to fall this year and next amid rising inflation.

- London’s core specialist service sectors face a very mixed outlook for 2022 and 2023. Information and communication is set for firm job growth over the two years, while Financial services and Real estate see weak or falling employment in 2022 before picking up next year. Professional services follow the opposite pattern.

- Areas of the economy dominated by public sector jobs are projected to generally remain above 2019 levels of employment, though growth slows next year as spending plans are not increased in line with the rising pace of inflation.

Table A2: London’s workforce jobs by industry in 2022 and 2023

Source: GLA Economics. Note: colour coding shows the most negative results in red, the most positive results in green, and results in the middle in white. Primary industries are shaded grey to avoid them having an outsize influence on shading for the rest of the table.

Long-term projections (2024 to 2031)

- Looking at the longer term, GLA Economics projects that real GVA levels will return to pre-crisis trends (the post-Brexit counterfactual) but that it may take a decade. This does still mean there is no long-term scarring in our baseline (Figure A5).

- In our fast economic recovery scenario, output pushes above this pre-crisis trend as soon as 2025, helping push London’s growth back towards long-term averages.

- The slow recovery scenario sees London’s output well below the counterfactual in the long term. Heavy scarring in the medium term raises structural unemployment, cuts investment and hits agglomeration benefits, lowering long-term output growth.

- As discussed above, these scenarios do not reflect the full range of uncertainty and there could be more downside risk in the long term associated with the city’s ability to remain as attractive and competitive as in the two decades prior to COVID-19.

Figure A5:

The scenario results presented in this supplement come within a context of continuing unprecedented uncertainty. Overall, GLA Economics judges that risks are tilted to the downside, especially with the war in Ukraine potentially raising global commodity prices further even as consumer incomes already face a squeeze from rapid inflation. Other headwinds also skew risks to the downside, including heightened geopolitical tensions, the possible emergence of new COVID-19 variants, global supply chain challenges and the risk of skill and geographic labour mismatches due to remote working. Therefore, GLA Economics will continue to track the economic data to review these scenario outcomes in the future. Successive updates will be released on the London Datastore.

[1] See the list of GLA summaries on external research on COVID-19, which have frequently included summaries of macroeconomic scenarios and forecasts publications.

[2] For more detail on these assumptions see slides 8 to 11.

[3] The National Institute of Economic and Social Research have found that London’s underlying inflation is running as much as 1ppt higher than the rate for the UK overall. See NIESR, Monthly CPI Tracker, May 2022