The 2025 Budget: Overview and potential implications

On 26 November 2025, Chancellor Rachel Reeves delivered the 2025 Budget within a context characterised by fiscal pressures and growing international uncertainty. This supplement presents some of the Budget’s key announcements and potential implications for London and Londoners.

Macroeconomic outlook

The Budget echoed existing concerns about the UK’s challenging fiscal environment, as did the Office for Budget Responsibility (OBR) Economic and Fiscal Outlook.

The OBR projects that real GDP will grow by 1.5% on average over the forecast period, 0.3 percentage points slower than was projected in March, due to lower underlying productivity growth. GLA Economics’ most recent growth forecast for London’s economy estimated growth for 2025 at 1.9%. That said, year-on-year productivity growth in London has been lagging that of other UK regions in recent years, and with London contributing almost a quarter of national income, the national productivity slowdown is in part a result of London’s productivity slowdown.

The Budget’s announced policies increase spending in every year and by £11 billion in 2029-30, primarily to pay for the summer reversals to welfare cuts and to lift the two-child limit in universal credit. While this may seem large, the increased spending in 2029-30 represents just over 0.5% of the UK’s GDP, and just over 2% of London’s. The Budget also raises taxes by amounts rising to £26 billion in 2029-30, through freezing personal tax thresholds and a host of smaller measures and brings the tax take to an all-time high of 38% of GDP in 2030-31. It is likely that a disproportionate percentage of this 38% would come from London. For example, in the 2023-24 tax year, London residents contributed approximately 26.7% of all UK income tax. Meanwhile, London contributed approximately 21% of total UK public sector revenue in the financial year ending (FYE) 2023.

Moreover, the OBR reduced its central forecast for the underlying rate of productivity growth in the medium term to 1.0 per cent, 0.3 percentage points slower than in the March forecast. This renders the challenge to raise productivity in London to 2% growth year-on-year until 2035 (as set out in the London Growth Plan) more imperative in the national context.

Infrastructure and transport

An important announcement made in the London context was confirmation of the approval of funding for the DLR extension to Thamesmead. This is expected to lead to about 25,000 new homes being built in London – a major figure given our housing targets for the upcoming decade.

The Chancellor also announced that the 5p fuel duty cut that was brought in during the pandemic will be extended until September 2026. This is expected to cost £2.4 billion next year and £0.9 billion in the medium term. Londoners are significantly less likely to drive cars than those in other UK regions, with the lowest rates of car ownership and use in England. While 80% of households in the rest of England have a car, only 56% of London households do, and just under half of London households are car-free, a higher percentage than any other region. This is linked to London’s extensive public transport system, and in 2021, London residents made the fewest average miles and trips by car compared to other regions.

The Budget also announced the introduction of mileage-based charges for electric and plug-in hybrid vehicles (to be introduced in April 2028). It will be set at around half the fuel duty rate paid by drivers of petrol cars and raise approximately £1.4 billion.

Londoners are more likely to drive electric cars than those in other UK regions, due to factors like greater availability of charging infrastructure, incentives like the ULEZ (Ultra Low Emission Zone), and a higher percentage of drivers planning to switch in the future. London has the highest percentage of electric car ownership in the UK. Surveys show a significant portion of London drivers plan to buy an electric car as their next vehicle. For example, one survey found over a quarter (27%) of London drivers expected to buy an EV next, which is nearly four times the figure for the Southwest the lowest region.

According to Transport for London (TfL), in April 2025, there were around 193,000 plug-in electric cars and vans already registered in the capital. EV numbers on the road in London are projected to reach between 1-1.4 million by 2030, making up to 49% of London’s car and van fleet. Moreover, London had 21,600 charge points in April 2025, which is around a third of all EV charging infrastructure across the country and more than any other UK region. TfL estimate that by 2030, 40,000 to 60,00 chargers will be needed.

Devolution

A key decision announced in a pre-Budget Ministerial Written Statement is that the government is giving Mayoral Strategic Authorities (MSAs) the power to introduce local overnight visitor levies. A 12-week consultation was launched seeking views on the design of the new power. According to preliminary projections by GLA Economics, depending on the structure of the levy, it could raise anywhere between £62 million (if it’s a £1 flat rate per room per night) and £543 million (if it’s a 5% levy on accommodation costs).

With regards to Integrated Settlement (IS) funding arrangements for London for 2026-2030, Adult Skills Fund (ASF) funding for 2026-27 to 2028-29 amounts to slightly under £337m per annum, while Connect to Work funding averages £46m per year over that same period. Additionally, Growth Hubs funding averages £550k over that same period, while National Housing Development Fund allocation rises to just under £120m in 2029-30. In total, IS quantum funding is around £469m in 2026-27, £457m in 2027-28 and £516m in 2028-29.

Business rates

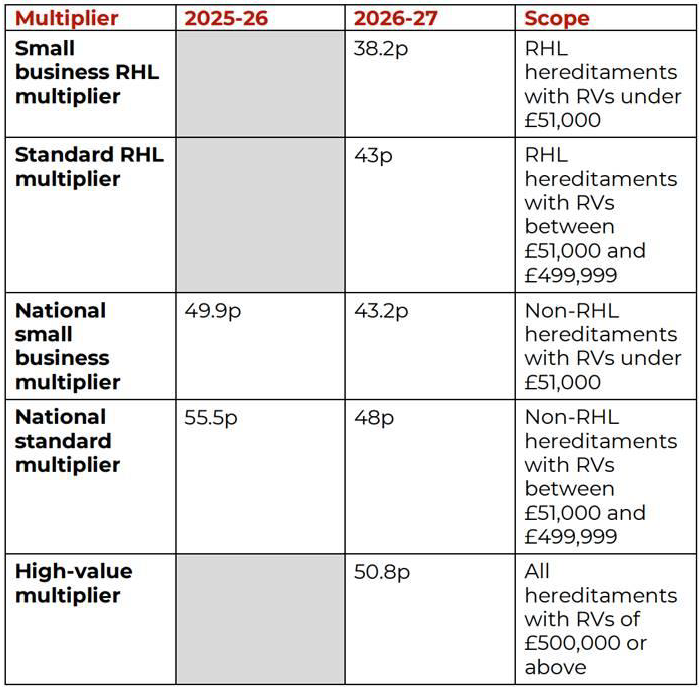

In Budget 2024, the government announced the intention to introduce permanently lower business rates multipliers (tax rates) for retail, hospitality and leisure (RHL) properties (hereditaments) with rateable values (RVs) under £500,000 from 2026-27. These multipliers will replace the temporary RHL business rates relief that is set at 40% (up to a cash cap of £110,000 per business) in 2025-26. In order to sustainably fund this, the government also announced at Budget 2024 the intention to introduce a higher multiplier on the most valuable properties from 2026-27 – those with RVs of £500,000 and above, which will be set at 2.8p above the national standard multiplier.

As part of the Budget, the government published analysis on the effects of the RHL and high-value multipliers when the rates were set. The table below shows the 2026-27 multipliers:

An estimated 110,900 properties in London are estimated to benefit from the new lower RHL multiplier (compared to 760,000 nationally) for RHL properties below £500k RV. Therefore, 15% of those ratepayers/properties benefitting from the changes are in London. By contrast 7,500 properties in London are estimated to be subject to the new higher multiplier (vs 21,100 properties nationally) on properties £500k+ RV which represents 36% of the national total.

Also published in the Budget is the transitional relief scheme to phase-in increases in business rates over the 3 years (2026-27 to 2028-29) (see table below). There are also extensions to measures which allow certain local authorities to retain a higher proportion of business rates revenue locally.

| 2026 Transitional relief scheme for business rates | |||

| Rateable value | Cap on increases 26/27 | Cap on increases 27/28 | Cap on increases 28/29 |

| Up to or including £20,000 (£28,000 in London) | 5% | 10% plus inflation | 25% plus inflation |

| More than £20,000 (£28,000 in London) and up to and including £100,000 | 15% | 25% plus inflation | 40% plus inflation |

| More than £100,000 | 30% | 25% plus inflation | 25% plus inflation |

| Notes: All caps are before other reliefs, local supplements and, in years 2 and 3, inflation. Actual bill changes may therefore vary from these percentages. Caps are cumulative year on year (e.g., for small properties the total cap over the 3 years before inflation is 44%). | |||

Together, the measures reduce receipts by £1.2 billion on average between 2026-27 and 2028-29, but are broadly neutral by the end of the forecast as the transitional relief package and local retentions are due to expire. Overall, tax receipts from business rates are expected to represent 1.1%-1.2% of GDP nationally (or between £20bn and £25bn annually).

Skills and education

The Chancellor announced that apprenticeships for under 25-year-olds will be free for small and medium-sized enterprises (SMEs). This change could support apprenticeships for under-25s in London, where apprenticeship starts for 19-24 year olds have been falling since 2021-2022. In 2022-2023, 12,710 (29%) of apprenticeship starts in London were in SMEs (i.e., enterprises with less than 249 employees). Meanwhile, in 2023-2024, 44% of apprenticeship starts in the capital were for those under-25.

An announced allocation of £725 million for the Growth and Skills Levy was made to help support apprenticeships for young people, including a change to fully fund SME apprenticeships for eligible people under-25. There have also been proposed changes to the apprenticeship system to make it more efficient, including for example:

- Short courses to be introduced from April 2026, including removing the additional uplift to levy accounts.

- Changing the government’s co-investment rate to 75% for levy-paying employers once they have exhausted all their funds.

- Working with employers to streamline the suite of apprenticeship standards available.

£820 million has also been allocated to the DWP’s Youth Guarantee programme. The guarantee is a UK-wide program that aims to provide a pathway to work, training, or an apprenticeship for young people, but statistics on its specific benefits to London are not yet available. The program is being rolled out in response to high youth unemployment, which affects many areas, including in London, and aims to ensure that fewer than 10% of young people are NEET i.e, not in education, employment, or training. The support includes offering a guaranteed six-month paid work placement for every eligible 18-to 21-year-old who has been on Universal Credit and looking for work for 18 months.

According to the Labour Force Survey, in the final quarter of 2024, 15.2% of 16–24-year-olds in London were classified as NEET compared to 13.6% in England. These are the highest percentages seen in both areas in the final quarters of each year since 2014.

Taxation and National Insurance

There have been many taxation-related announcements in this Budget. The highlight announcement is the continuation of the existing freeze on income tax thresholds for another three years from the current freeze period’s end (in 2028).

Initial modelling by GLA Economics – which does not factor in behavioural changes resulting from this freeze – suggests that in the first two years, up to the end of this parliament, London taxpayers will contribute an additional £1.7bn due to the freeze in personal allowance, higher and additional rate and NI thresholds. In terms of breakdown by financial year, that is £560 million in 2028-29 and £1.14 billion in 2029-30.

The Chancellor also announced a set of personal tax rises that would collectively raise £15 billion in 2029-30. These include:

- The aforementioned freeze of tax thresholds from 2028-29 onwards, which raises £8.0 billion in 2029-30 and contributes to around 780,000 more basic-rate taxpayers, 920,000 more higher-rate taxpayers, and 4,000 more additional-rate taxpayers by 2029-30 than in the March forecast (nationally).

- Charging National Insurance on salary-sacrificed pension contributions from April 2029 (any amounts over £2,000 that are annually contributed to salary-sacrifice schemes would be subject to employee and employer NI levies), raises £4.7 billion.

Londoners are among the most likely in the UK to use salary sacrifice schemes for pension contributions, particularly for investing bonuses. The higher cost of living and prevalence of high-paying jobs in the capital likely contribute to the appeal of these tax-efficient methods. A 2024 report found that London and Birmingham had the highest percentage of workers paying some or all of their bonus into their pension pot through salary sacrifice (57% in London).

- Increasing tax rates on dividends, property and savings income by 2 percentage points, raising £2.1 billion. Londoners are arguably to be disproportionately affected by these increases as they are more likely to earn dividends, property and savings income.

Other tax changes have also been announced that will raise £11 billion by 2029-30, such as:

- A reduction in the ability to write down allowances in corporation tax (£1.5 billion).

- Reforms to gambling taxation (£1.1 billion). From April 2026 there will be an increase in remote gaming duty from 21 to 40% and abolition of bingo duty from its current 10% rate. From April 2027, a new rate of general betting duty for remote betting will be introduced at 25% , excluding self-service betting terminals, spread betting, pool bets, and horseracing. The government has also announced a freeze in casino gaming duty bands in 2026-27 with the usual RPI uprating thereafter.

Recent data suggests that Londoners are more likely to gamble than people in most other parts of the UK. For example, A June 2025 survey found that London had the second-highest monthly gambling participation rate among UK cities, with 71.9% of residents gambling at least once a month, just behind Cardiff (72.5%), while London and Manchester tie for the highest rate of monthly online sports betting, at 31% of the population, a higher percentage than any other UK region. This suggests a disproportionate impact of these changes on Londoners.

- Changes to capital gains tax reliefs on employee ownership trusts (£0.9 billion)

- Tax administration, compliance and debt collection measures (£2.3 billion).

The government will also consult on removing customs duty relief for low-value imports worth less than £135, which mimics the ‘de minimis’ exemption introduced by the Trump administration to target low-value imports from businesses such as Temu. While this is likely to generate revenue for the Exchequer, it could also augment cost-of-living pressures that Londoners face as inflation continues to persist across the UK.

The government is introducing a new UK Listing Relief- a three-year exemption from Stamp Duty Reserve Tax for companies listing in the UK. Currently a 0.5% SDRT on share trades for newly listed UK companies applies; the removal of this aims to make the UK (and London) a more attractive place for initial public offerings (IPOs).

The main Writing Down Allowance (i.e., tax deductions businesses can claim for the depreciation of capital assets) will fall from 18% to 14%, meaning businesses can deduct a smaller percentage of the asset’s value from taxable profits. Balancing this, a new allowance of 40% for main rate assets will be introduced, meaning businesses can deduct 40% of the cost of a qualifying asset in the first year, aimed at incentivising investment. Such changes could be beneficial to help London and the rest of the UK boost business investment at a time when it significantly lags that in other G7 countries. Low business investment in London and the UK is a major factor behind the productivity slowdown in recent years.

Housing and planning

A key housing-related announcement relates to the so-called ‘mansion tax’. A “high value” council tax surcharge will be introduced on an estimated 100,000 properties in England with a value above £2m – this will be collected alongside local council tax (i.e., on the same bills) by local councils but 100% of the revenues will be transferred to central government. The surcharge is designed as a flat rate with four bands: 1) a £2,500 a year charge on homes worth £2-2.5m, 2) a £3,500 a year charge on homes worth £2.5-3.5m, 3) a £5,000 a year charge on homes worth £3.5-5m, and 4) a £7,500 a year charge on homes worth above £5m. This will be consulted on, including options to allow people to defer payment (e.g., until sale of property/death).

Broadly speaking, properties worth over £2m are likely to be in Council Tax Band H (though not necessarily). Council Tax Band H are those typically valued over £320K in 1991 (or £2.1m in 2025 adjusting for inflation). Using this as a rough guide, there were just over 68,000 properties in London that belong to this category. Collectively, they are expected to pay over £200m in council tax in 2025-26, and most of them would potentially incur this extra charge.

An announcement was made to invest an extra £48 million of additional funding to boost capacity in the planning system. This includes investment to recruit an extra 350 planners in England and funding improvements to the performance and speed of environmental regulators. This will take the total number of recruitments across the planning system to 1,400 by the end of this Parliament. The government also announced that it decided not to proceed with converging the two rates of Landfill Tax, as consulted on earlier this year. Instead, it will prevent the gap between the two rates of Landfill Tax from getting any wider over the coming years. The government will also retain the tax exemption for backfilling quarries to ensure that housebuilders and the construction sector continue to have access to a low-cost alternative to landfill.

Other things equal, this would be important for London to realise its housing construction targets as the sector continues to experience high supply-side pressures due to labour-market shortages and the rising cost of materials used in construction (which are mainly imported).

The government will confirm in Jan 2026 how the Social Rent convergence will be implemented. Social rent convergence is a government policy aimed at bringing social housing rents into alignment with a national “formula rent” based on factors like property value and local earnings. The policy was active between 2002 and 2015, and the government has recently proposed reintroducing it to help social housing providers fund investment in their properties.

Convergence allows rents for Social Rent homes that are below ‘formula rent’ (nationally set rent) to increase by an additional amount per week (over and above the Consumer Price Index +1% limit), so rents gradually converge towards formula rent. It is worth noting that while the government consulted on a £1/£2 per week uplift, London’s affordable housing sector has called for a £3 per week uplift to support investment in improving existing social and affordable housing stock and gradually increase the supply of new social and affordable homes.

The government will shortly consult on the reform to VAT rules to incentivise development on land intended for social housing, which could provide much-needed support to boost affordable housing supply in London. The government will also carry out a review of homelessness services to improve value for money and the availability of good quality temporary accommodation and supported housing.

Benefits and children

The Chancellor confirmed the abolishment of the two-child benefit cap from April 2026. The two-child limit currently restricts financial support in Universal Credit to the first two children in a household, except for limited exemptions. Nationally, 1.67 million children in 470,000 households are affected by the policy.

In London, 260,000 children in 70,000 households are affected – the highest number of any region. According to the Institute for Fiscal Studies, removing the two-child limit entirely would, in the long run, bring around 630,000 children out of absolute poverty, at a cost of roughly £5,700 per child. Compared with other levers in the benefit system, reversing the limit is one of the most cost-effective ways to reduce child poverty.

GLA analysis suggests that the percentage reduction in poverty is smaller in London than across the UK, though the numbers affected in London remain significant. According to our estimates:

- the overall poverty rate in London falls by 0.6 percentage points, equivalent to around 50,000 fewer people in poverty (compared with a 1.1-point fall UK-wide)

- the child poverty rate in London falls by 1.7 percentage points, equivalent to around 40,000 fewer people in poverty (compared with a 3.6-point fall UK-wide).

While the reduction in poverty rates is smaller in London in percentage terms, the estimated increase in mean weekly disposable income across households is similar in London and across the UK (up £2.23). This pattern likely reflects London’s higher income inequality. The poorest London households start from lower income levels (after housing costs) than similarly placed households elsewhere in the UK. As a result, the policy raises incomes for many low-income Londoners but not always by enough to lift them above the ‘poverty line’.

In London, removing the two-child limit particularly benefits lower income households, working households, households with young children, and households headed by a Black adult. Higher-income households see little or no change.

It is important to be mindful of caveats and limitations to these estimates:

- Results reflect changes in benefit entitlements only and do not capture behavioural responses.

- Regional results rely on pooled HBAI (Households Below Average Income) data, which improves robustness but may smooth short-term variations.

- Poverty is measured using a fixed baseline poverty line

- The modelling used pooled HBAI data for 2021-22 to 2023-24 for London analysis, and the single-year 2023-24 dataset for UK analysis.

- Results should be seen as indicative. They rely on survey data that may have small sample sizes for London, use simplified assumptions for some tax and benefit rules, and there are differences between model baselines and the latest administrative data.

The Chancellor also announced reforms to Motability tax reliefs, including the removal of premium car brands. It is difficult to say definitively whether Londoners are more likely to use the Motability scheme, as there is no specific data comparing London-specific usage rates to the rest of the UK.

Furthermore, the maximum amount that can be reimbursed for childcare costs for eligible Universal Credit claimants will increase by £736.06 for each additional child above the current maximum cap for two children. Meanwhile, to improve work incentives, the government is reducing the financial cliff edge for claimants in supported housing and temporary accommodation from Autumn 2026.

Pensions and ISAs

The government reaffirmed its commitment to upholding the Triple Lock. However, from April 2027, the £20k annual ISA allowance will remain, except that £8k of the £20k will be exclusively meant for investment in a stocks-and-shares ISA (meaning that one could only invest up to £12k in a cash ISA). This is intended to boost investment in the economy by channelling more retail money into equities, which policymakers hope will deepen the pool of capital available to listed companies and help revive London’s markets. That said, anyone over 65 will still be able to place the full £20,000 into a cash ISA.

More than 40% of current cash ISA users deposit over £12,000 a year, so a sizeable group will be prodded into investing whether they planned to or not. HMRC data shows that the Southeast and Southwest regions have among the highest proportion of adults holding ISAs at 45.6% and 46.4% each, while London has the lowest at 37.4%.

One potential implication from cutting the cash ISA limit is higher mortgage rates. Cash ISAs are a key source of funding for banks and building societies, which use the deposits to fund loans to households and businesses. For example, Nationwide Building Society has said that cutting tax breaks on the accounts would reduce the availability of mortgages for first-time buyers.

There is also the possibility that people who are unfamiliar with stock market investing would be deterred from saving in ISAs as a result of the change, which would produce the opposite effect to what the policy was originally intended to do.

It is also worth noting that according to Hargreaves Lansdown, only 23% of Brits invest in the stock market in general, compared to 66% in the US for example. Whether this change would increase that percentage to levels seen in countries such as the US remains to be seen.

Interestingly, polling 3,000 people nationally, interactive investor found that more than half (58%) of Britons, around 31.4 million people, have low ‘emotional’ capacity for risk (meaning they are unwilling to face the prospect of incurring short-term losses on investments). Despite this fact, 32% of these – over nine million people – have the financial resilience to take on risk, but are held back by this emotional capacity for risk leading people to ‘underinvest’.