The impact of rising interest rates and financial turbulence on London’s economy

Higher interest rates and quantitative tightening are reversing the post-2008 global policy regime, with broad-ranging consequences. Massive pandemic policy stimulus combined with stretched supply chains to spark cost pressures around the world, which became a crisis when energy prices surged after Russia’s invasion of Ukraine. Central banks have responded to these inflationary pressures by sharply tightening monetary policy. This shift will drag on economic activity, but the results may vary across UK regions and sectors. The sudden switch from easy money to tight lending is also generating turbulence in the financial sector, culminating in a set of bank failures. These trends look unlikely to overflow into a full financial crisis, but it is important to examine the risks, as financial services remain a major force in London’s economy – making up more than 20p in every £1 of its output in 2021[1]. This box sets out the macroeconomic and financial consequences of rising interest rates for London and highlights potential vulnerabilities.

London’s economy should be relatively shielded from the macro effects of higher rates

The Bank of England is not alone in hiking interest rates since the beginning of 2022. The European Central Bank (ECB) and the US Federal Reserve have hiked interest rates by 3.75 percentage points (ppts) and 5ppts respectively. Lying in the middle, the Bank has hiked from a policy rate of 0.1% to 4.5% in just over a year. This represents the sharpest rise in interest rates since the late 1980s[2], to match the largest UK inflation surge in over 40 years. While such a sharp tightening of policy should help inflation return to target sooner, this comes at the expense of slower economic activity. The transmission from interest rates to output is well-studied, and tends to come under four broad headings. There is a borrowing cost channel, a credit channel, an asset price channel and an exchange rate channel. The effects of the asset price channel are hard to differentiate at the regional level, and the exchange rate channel receives less conclusive support in data studies[3]. Exchange rate effects will also be hard to pick out when the pound is already fluctuating due to wider investor sentiment. As a result, we focus on the first two channels and what they could mean for London.

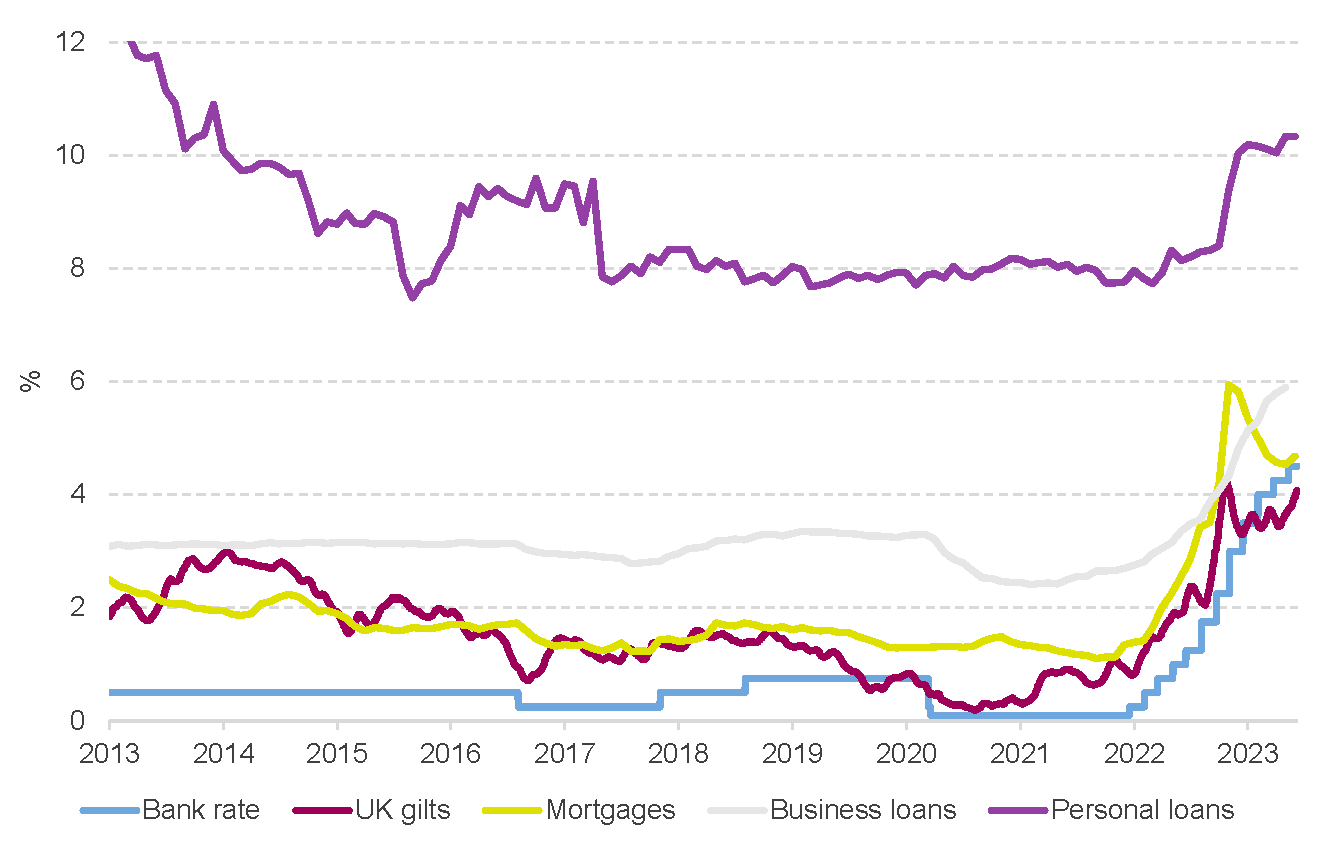

Borrowing costs are certainly up (Figure 1). UK government bond yields, after easing from the shock of last September’s ‘mini-budget’[4], have risen again after upside inflation surprises and Bank of England rate hikes[5]. This has had varied impacts across lending rates. Fixed-term mortgage rates are creeping up again, but are still below their peak from last September[6]. Yet personal loan interest rates never fell from their autumn spike. A loan for £5,000 averaged an interest rate of about 8% in the five years before September 2022, but this jumped to 10% by November, where rates have remained[7]. Business loan interest rates are averaging just under 6%, compared to a reasonably stable average of 3.1% from 2011 to 2019[8]. Higher borrowing costs will drag on significant parts of economic demand. For households, it is now much more expensive to borrow for major purchases, such as cars, furniture and appliances. For businesses, borrowing to invest is more costly.

Figure 1: Interest rates have risen across the board

Source: Bank of England; Note: Bank rate is official Bank of England policy rate, daily; UK gilt rate is the 10-year yield, 4-week average; Mortgages is the 2-year fixed rate 60% Loan-to-Value interest rate, monthly; Business loans is the weighted average interest rate on outstanding loans to private non-financial corporations, monthly; Personal loans is the average interest rate on a £5,000 unsecured personal loan, monthly

Higher borrowing costs will have varying effects across the UK’s regions. Studies have shown that the impacts are sharpest in areas where a larger share of output depends on durable goods[9]. While parts of the retail sector might be more vulnerable, the impact is strongest for durables manufacturing. London’s very low share of output from manufacturing should therefore dampen the macroeconomic impact of higher interest rates. While the UK economy as a whole gets just over 11% of its output from manufacturing, that share in London is just 2%. Overall, London’s output is less dependent on goods and production sectors, with services making up 92% of the capital’s economy, compared to 78% at the national level. On the consumer side, wholesale and retail also makes up a smaller share of London’s economy – just 6.4% compared to the UK average of 9.1%. And while London has the largest stock of household debt in the UK[10], its households also have a much higher average income[11]. At 94%, London’s ratio of total household debt to gross disposable income is middle of the regional pack. In fact, the ratio between total non-mortgage debt of households in the capital and its total income is the lowest in the UK. Overall, higher interest rates may matter less for London’s outlook, especially on the business side.

Meanwhile, borrowing will also become costlier through a credit channel. Higher interest rates lower firms’ net worth by cutting equity valuations, which reduces the amount of collateral firms can offer up for their loans[12]. This makes them less exposed to losses, which could increase their risk tolerance. As a result, lenders tighten their standards and charge a premium to compensate for the extra risk, again raising borrowing costs. This translates into fewer approvals and a slower pace of consumer and business loans. Business loans were contracting 5.2% on an annualised basis in the first three months of 2023[13], while personal loans were close to no monthly growth[14]. Tighter lending standards will have a sharper effect on businesses with less collateral to offer up as insurance against default. This tends to mean smaller, younger firms[15].

The relative impact of the credit channel on London is tricky to isolate. Despite serving as a headquarter for many major national companies, overall London has a slightly larger than average share of small businesses by headcount. Across the UK, just over 78% of firms have less than five employees, while in London the figure is above 81%[16]. But this result may not be conclusive, as London’s distribution of firms by turnover size largely mirrors the UK average. And while London has tended to see higher business birth rates than the national average, its new firms’ survival rates tend to be in the middle of the regional pack[17]. London does seem to have a particularly larger-than-average share of small firms in manufacturing and construction. Two thirds of UK manufacturers employ fewer than five workers, but for London that share is over three quarters. So while those sectors matter less for London’s overall economy, they may face a particularly difficult outlook compared to producers and builders elsewhere in the UK.

Rising interest rates are also creating financial turbulence, but not yet a crisis

But the impacts of the sharp tightening in monetary policy are not only macroeconomic. The global financial sector has been thrown into turbulence as credit has dried up, with some firms’ business models exposed as unsustainable. The stress has culminated in a string of bank failures since March, with Silicon Valley Bank, Signature Bank and First Republic Bank going under in the US, while in Europe, Credit Suisse collapsed.

In the US, the failed banks were all mid-sized regional banks, which tend to have shared, unusual characteristics. Two key issues were rich clients with uninsured deposits, and an asset base too heavily dependant on government bonds. Silicon Valley Bank (SVB) is perhaps the starkest example. This bank was uniquely exposed to interest rate risks on both its assets and liabilities. SVB’s clients came mostly from the tech sector, and deposits more than tripled between the start of 2020 and 2022[18] as loose monetary policy flooded the financial system with funding. Yet the bank invested the bulk of this fresh money into interest-bearing securities rather than expanding its loan book. Securities went from 40% of assets to 60% in two years[19]. As a result, when interest rates rose, this simultaneously dampened lending to the tech sector – threatening SVB’s deposits – and cut the value of its bond holdings – threatening SVB’s assets. With only 6% of its deposits covered by the $250,000 Federal Deposit Insurance Corp (FDIC) guarantee[20], SVB’s clients were also unusually exposed to the bank failing. A ratings downgrade, a large bond sale, and a failed attempt to raise more capital[21] saw its clients increasingly withdraw their funds, generating a bank run. While Signature Bank and First Republic (the second-largest bank failure in US history) were less reliant on corporate deposits and bond assets, similar dynamics ultimately played out. Signature came under pressure partly due to its links with the cryptocurrency sector – itself under pressure following the collapse of crypto exchange FTX[22]. Meanwhile, First Republic stood out for having 68% of its deposits above the FDIC guarantee threshold[23].

More failures among regional or mid-sized US banks are plausible. Aside from tech exposure and under-insured deposits, two other risks stand out for these firms: exposure to commercial real estate (CRE) and a lack of stress tests. CRE stands out as an issue both because the future of offices is challenged by hybrid working, and because the sector is composed of illiquid, long-term assets, making it interest-sensitive. In its April 2023 Global Financial Stability Report (GFSR), the International Monetary Fund (IMF) remarked that “In the United States, banks with total assets less than $250 billion account for about three-quarters of CRE bank lending, so a deterioration in asset quality would have significant repercussions both for their profitability and lending appetite.”[24]

Banks with assets under $250 billion may also have had their vulnerabilities hidden by changing banking rules. After 2008, the Dodd-Frank Act financial regulations meant that all US banks with assets above $50 billion were subject to strict capital and liquidity requirements, along with ‘stress tests’. These involve banks running simulations for what would happen to their balance sheets under different macroeconomic shock scenarios that are set by the Federal Reserve. Such scenarios will usually include an interest rate shock. However, in 2018, new rules under the Trump administration meant US banks with assets below $250 billion were exempt from these rules. This meant mid-sized US banks could both increase their leverage and stop simulating how their balance sheets would react to an adverse economic shock. While this Trump-era deregulation is likely not the decisive factor in the recent string of failures, it made it harder to spot pockets of risk developing in mid-sized US banks. The KBW Regional Banking Index, which tracks US regional bank stocks, has seen prices fall by around 30% between February and May 2023[25]. More such firms could yet fail.

While mid-sized US banks have proven unusually vulnerable, the crisis has generated a global ripple effect. The broad S&P 500 stock index was roughly flat from February to May 2023[26], but the S&P 500 Banking sub-index fell nearly 20%[27]. This shows that the global banking sector is coming under close scrutiny, with fears of contagion.

There has been one major bank failure outside the US. In March, Credit Suisse (CS) was taken over by rival Swiss bank UBS as it began to collapse. Yet while CS, with assets of around $575 billion at the end of 2022, was a large enough bank to be judged a Global Systemically Important Bank by international banking regulators[28], it was also uniquely vulnerable. The bank posted its biggest annual losses since the financial crisis in 2022, while accusations of mismanagement, sanctions violations and links to tax evasion and money laundering have plagued the bank for years[29]. After an admission of ‘material weaknesses’ in its financial reporting, share prices turned from a long slide into a collapse[30]. These unique challenges suggest that Credit Suisse’s failure follows a logic of ‘devil take the hindmost’ in the global banking system, and other major European banks are less troubled.

Central banks around the world have also responded to the global ripple effect of banking sector turbulence. In the US, the government guaranteed all deposits at SVB and Signature, and allowed JP Morgan to purchase First Republic, moving all deposits into the US’ largest bank. Meanwhile, the Federal Reserve opened a Bank Term Funding Program to back up liquidity requirements and help banks meet depositor needs[31]. In Europe, after approving the UBS purchase of Credit Suisse, regulators made up to $220 billion in extraordinary liquidity assistance available to the merged bank[32]. These activities seem to have stemmed the immediate crisis in both regions, but more bank failures remain a possibility. Indeed, the Federal Reserve recently warned of “a sharp contraction in the availability of credit” due to financial sector ructions[33]. Fed economists also warned that tighter financial conditions made a mild recession in the US later in 2023 likely[34]. So while central bank measures may have staved off a crisis, financial turbulence has a real impact on the global outlook.

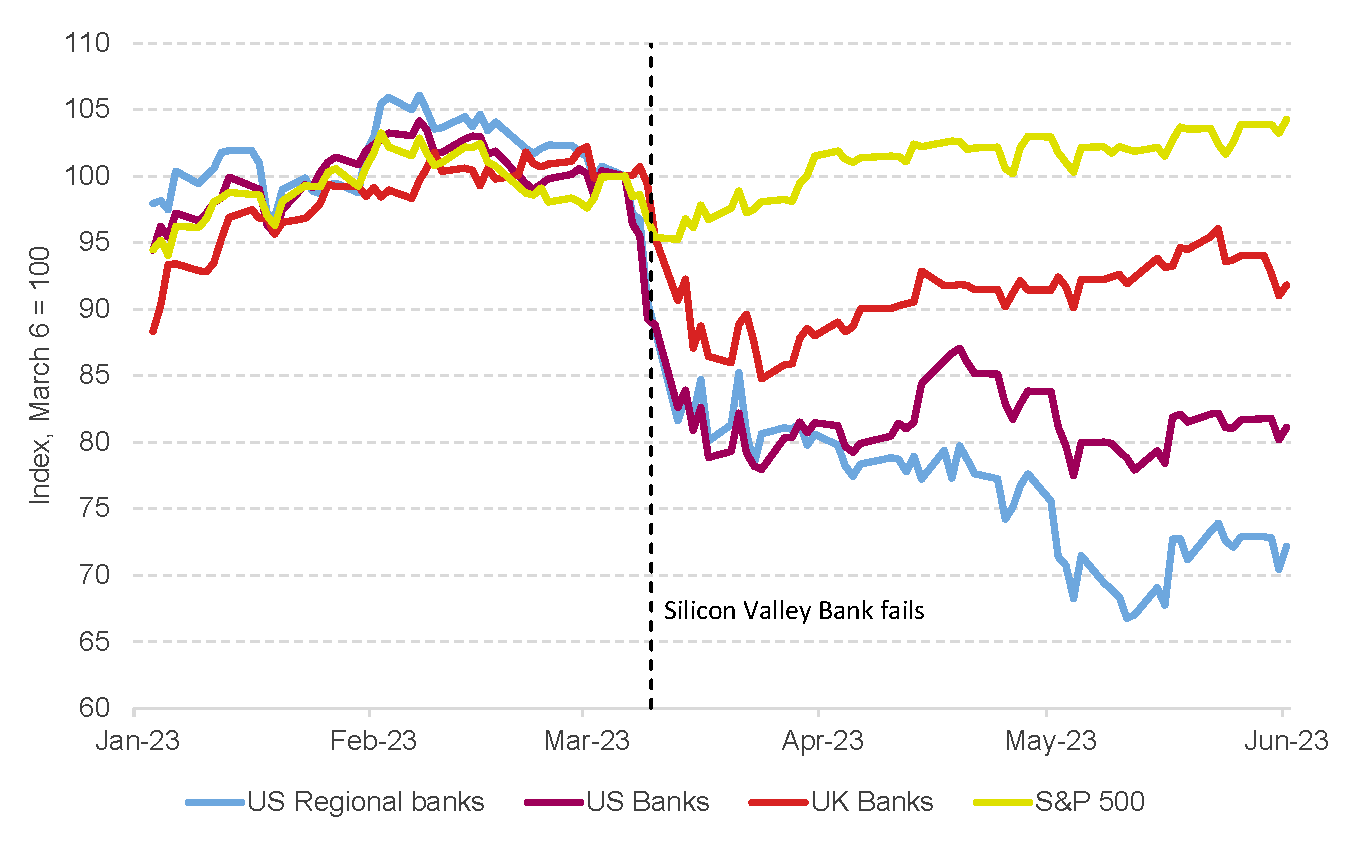

Amid this global uncertainty, the UK financial system looks relatively resilient. Stocks for UK banks are down less than global averages, with the FTSE 350 Banking index falling 10% between February and May[35] (Figure 2). There are also many differences between UK banks and the US regional banks that have been most under pressure. In contrast to US deregulation, UK banks continue to be closely supervised, and stress tests indicate their balance sheets should be robust to rising interest rates[36]. Some estimates suggest commercial real estate makes up as much as 40% of loans from smaller US banks[37], while the share is just 6% for UK banks[38]. Overall, there are plenty of reasons why the Bank of England found the UK banking system “has the capacity to support the economy in a period of higher interest rates even if economic conditions are worse than expected”[39]. A UK generated banking crisis looks unlikely.

Figure 2: UK bank stocks are under less pressure than global benchmarks

Source: MarketWatch, GLA Economics

Non-bank finance represents a further risk, with gaps in regulation and data

But crises rarely happen the same way twice, and there are other parts of the financial system that could spur a crash. Policymakers are turning attention to non-bank financial intermediaries (NBFIs). Sometimes referred to as ‘shadow banking’, these are the areas of the financial system where money managers look to generate yield on their clients’ savings deposits by taking risks. The IMF’s GFSR observes that “fragilities in the [non-bank finance] sector stem from the use of financial leverage, poor liquidity mismatches, and high levels of interconnectedness”[40]. Anil Kashyap of the Financial Policy Committee explained how ‘liquidity multipliers’ can build up cash claims in the sector in a 2020 speech[41]. He applies this framework to the March 2020 ‘dash for cash’ when US bond markets see-sawed in response to the initial shock of the pandemic. These multipliers also explain why central bank liquidity measures needed to be larger than implied by the notional cashflow of the target markets.

Closer to home, the pension fund crisis in September 2022 also took place in market-based finance. As UK Gilt yields rocketed in response to the ‘mini-budget’, pension firms found themselves subject to large collateral calls to back up bond-based hedges as part of ‘liability-driven’ investment strategies[42]. Again, central bank action was required to stem a potential crisis. The Bank of England temporarily injected up to £5 billion a day into the Gilt market to ease forced selling, less than a week after announcing quantitative tightening bond sales[43]. With the Financial Policy Committee judging that inaction would have meant a “material risk to financial stability”[44], this episode again lays bare the risk from non-bank finance. And while UK banks issue the largest share of UK commercial real estate loans, non-bank involvement has tripled between 2012 and 2022[45]. This could create links between economically vulnerable sectors and non-bank financial instability as interest rates rise.

It is currently hard to quantify how serious the risk is from these sectors. Part of the issue is a lack of clear information. However, global financial regulators are now looking to build both a better understanding of the risks in market-based finance and fresh regulation to address the biggest hazards[46]. The IMF recommends surveillance, regulation and supervision as the “first line of defense”[47], but also points to central bank liquidity support as the way to contain a crisis. Temporary large-scale liquidity can help stem market-wide turbulence, heavily conditional standing lending facilities can help prevent spillovers between markets, and stepping up as the lender of last resort can stabilise systemically important NBFIs. While this playbook would not completely prevent stresses in market-based finance, it should help prevent market-specific instability spilling into a wider financial crisis.

A financial crisis would hit London’s growth in both the near and long term

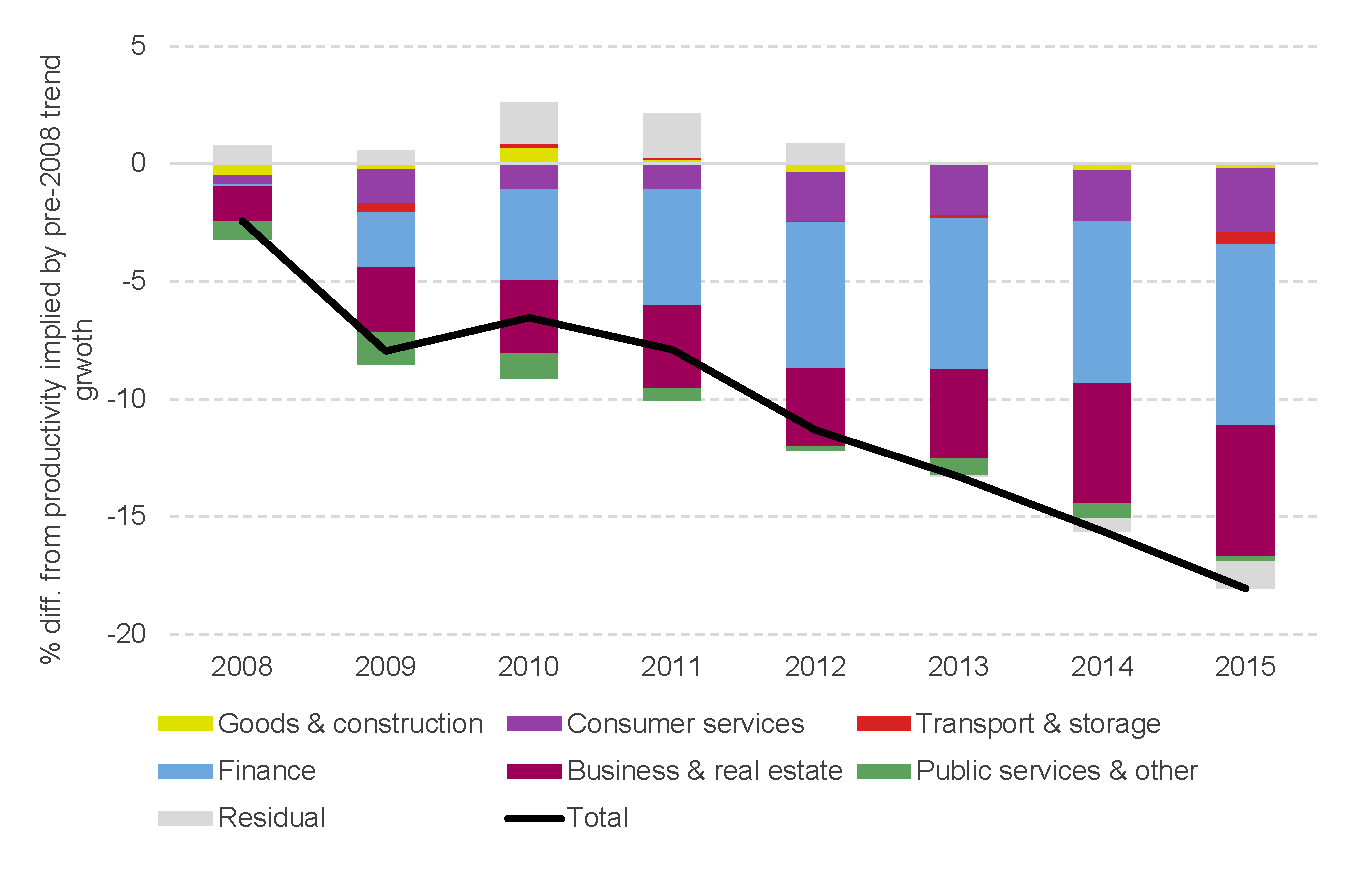

Given the possible pockets of risk, it is worth asking what impact a crisis would have on London. A useful starting point would be the effects of the last major crash. The global financial crisis of 2008 prompted a sharp recession across the UK, and trend growth has never fully recovered. London’s job market recovered better than the rest of the UK[48], but GDP outperformed less. Trend growth was particularly affected for certain sectors. By 2015, Finance was still 20% below its pre-crisis output, Manufacturing 5% and Transport 4%. Whether due to reduced risk-taking in finance or labour hoarding in other sectors, output growth failed to keep up with the job recovery. London’s productivity fell sharply below its previous trend growth rate. By 2015, London’s output per job in the financial sector was still falling, reaching 22% below 2008 levels (Figure 3).

Figure 3: Real productivity compared to pre-2008 trend, broken down by sector

Source: ONS, GLA Economics; Note: residual is due to changing patterns of sector shares in real data

And any financial shock that sucks liquidity out of the system will add to the conventional investment-damping effects of tighter monetary policy. London’s fastest-growing major sector in the five years before the pandemic was IT – a sector which has also recovered strongly since 2021[49]. Yet across the UK, this is also the most investment-hungry sector outside primary industries[50]. Excessive tightening of credit due to financial instability could therefore drag on the potential of sectors that underpin London’s long-term growth.

The risks to London’s economy from tighter monetary policy and financial sector turbulence are wide-ranging. Higher interest rates should drag on London less due to its low dependence on manufacturing. Yet there will still be a material drag, and higher interest rates will raise housing costs further in the middle of a cost of living crisis. But sectors exposed to durable goods may fare even worse in London than elsewhere due to a higher share of small firms. The evaporation of cheap credit and higher yields on safe assets have exposed cracks in the global financial system, but these look unlikely to prompt UK bank failures. At the same time, non-bank finance poses complex risks to stability, especially where it interacts with troubled real economy sectors like commercial real estate. A UK financial crisis still looks unlikely, but if one did emerge, it threatens another blow to London’s long-term economic potential. While we do not think a new financial crisis currently warrants detailed modelling, our downside forecast scenario incorporates some of the effects of further financial instability dragging on investment and output. We will be closely monitoring the impacts of rising interest rates, the vulnerability of different sectors and the implications for growth.

[1] ONS (2023), “Regional economic activity by gross domestic product, UK: 1998 to 2021”, April 2023.

[2] Bank of England database, Official Bank Rate series, indicators IUQABEDR and IUQLBEDR

[3] Choi, Willems & Yoo (2023), “Revisiting the monetary transmission mechanism through an industry‑level differential approach”, Bank of England Staff Working Paper No. 1,024, May 2023.

[4] Following the Truss Government’s decision to announce a series of unfunded tax cuts without an official forecast in September 2022, UK government bond yields surged, also driving up mortgage interest rates.

[5] Bank of England database, 10 year nominal par yield on British Government securities, indicator IUDMNPY

[6] Bank of England database, 2 year fixed rate 60% LTV household mortgage interest rate, indicator IUMZICQ

[7] Bank of England database, Interest rate on personal loan of £5k to households, indicator IUMBX67

[8] Bank of England database, Interest on non-variable loans to non-financial corporations, indicator CFMHSDC

[9] Durante, Ferrando & Vermeulen (2022), “Monetary policy, investment and firm heterogeneity”, European Economic Review Vol. 148, September 2022.

[10] ONS (2022), “Personal financial & property debt by age and region: April 2018 to March 2020”, January 2022.

[11] ONS (2022), “Regional gross disposable household income: all ITL level regions”, October 2022.

[12] The foundational paper on this channel is Bernanke and Gertler (1989). “Agency costs, net worth, and business fluctuations.” American Economic Review 79, no.1, March 1989: 14-31.

[13] Bank of England database, 3 month growth rate (annualised) of bank loans to business, indicator RPMZO8F

[14] Bank of England database, Monthly growth rate of lending to individuals, indicator LPMBZ2E

[15] Durante, Ferrando & Vermeulen (2022), “Monetary policy, investment and firm heterogeneity”, European Economic Review Vol. 148, September 2022.

[16] ONS (2022), “UK business; activity, size and location: 2022”, September 2022.

[17] ONS (2022), “Business demography, UK”, November 2022.

[18] Robert Armstrong (2023), “SVB is not a canary in the banking coal mine”, Financial Times, March 2023.

[19] Evgueni Ivantsov (2023), “Strategic risk failure is what unites Credit Suisse and SVB”, FT, May 2023.

[20] Caitlin Gilbert, Alyssa Fowers, Jacob Bogage and Daniel Wolfe (2023), “These companies had billions of dollars at risk in Silicon Valley Bank”, Washington Post, March 2023.

[21] Alexandra Scaggs (2023), “Silicon Valley Tank(s)”, FT Alphaville, March 2023.

[22] IMF (2023), “A Financial System Tested by Higher Inflation and Interest Rates”, GFSR, April 2023, page 4.

[23] Reuters (2023), “Factbox: Top five U.S. regional banks with most uninsured deposits”, March 2023.

[24] IMF (2023), “A Financial System Tested by Higher Inflation and Interest Rates”, GFSR, April 2023, page 4.

[25] MarketWatch, KBW Regional Banking Index data, Ticker KRX

[26] MarketWatch, S&P 500 Index data, Ticker SPX

[27] MarketWatch, S&P 500 Banks Industry Group Index data, Ticker SP625

[28] Financial Stability Board (2022), “2022 List of Global Systemically Important Banks”, November 2022.

[29] Kalyeena Makortoff and David Pegg (2022), “Crooks, kleptocrats and crises: a timeline of Credit Suisse scandals”, The Guardian, February 2022.

[30] Owen Walker, “Credit Suisse finds ‘material weaknesses’ in financial reporting controls”, March 2023.

[31] Federal Reserve (2023), Press release, March 2023.

[32] IMF (2023), “A Financial System Tested by Higher Inflation and Interest Rates”, GFSR, April 2023, page 8.

[33] Federal Reserve (2023), “Near-Term Risks to the Financial System”, Financial Stability Report, May 2023.

[34] Federal Open Market Committee (2023), Staff Economic Outlook, FOMC Minutes, May 2023.

[35] MarketWatch, FTSE 350 Banks Index GBP, Ticker 189731

[36] Bank of England, “Banking sector resilience”, Financial Policy Summary and Record, March 2023.

[37] Marc Jones (2023), “Europe’s banks in ‘better place’ than U.S. in terms of commercial property risk – JPMorgan”, Reuters, March 2023.

[38] Matthew Pointon, Capital Economics, via Julia Kollewe (2023), “Could office blocks be the next big casualty of the banking crisis?”, The Guardian, March 2023.

[39] Bank of England, “Banking sector resilience”, Financial Policy Summary and Record, March 2023.

[40] IMF (2023), “A Financial System Tested by Higher Inflation and Interest Rates”, GFSR, April 2023, page 15.

[41] Kashyap (2020), “The Dash for Cash and the Liquidity Multiplier: Lessons from March 2020”, Speech at London Business School, November 2022.

[42] Breeden (2022), “Risks from leverage: how did a small corner of the pensions industry threaten financial stability?”, Speech at ISDA & AIMA, November 2022.

[43] However, financial stability operations eventually amounted to less than £20 billion in total, compared to the nearly £900 billion total peak size of QE. See Bank of England (2022), News Release on unwinding financial stability gilt purchases, or for a graphical illustration, Hauser (2023), “Looking through a glass onion: lessons from the 2022 LDI intervention”, Speech at University of Chicago Booth School of Business, March 2023.

[44] Bank of England (2022), News Release “Bank of England announces gilt market operation”, November 2022.

[45] Daniel Cunningham (2023), “Strong lending volumes, more defaults: Bayes’ key 2022 UK market findings”, Real Estate Capital Europe, April 2023.

[46] Financial Stability Board (2022), “Enhancing the Resilience of Non-Bank Financial Intermediation: Progress Report”, November 2022.

[47] IMF (2023), “A Financial System Tested by Higher Inflation and Interest Rates”, GFSR, April 2023, page 46.

[48] ONS (2023), “JOBS05: Workforce jobs by region and industry”, March 2023.

[49] ONS (2023), “Quarterly country and regional GDP”, May 2023

[50] ONS (2022), “Business investment by industry and asset”, August 2022.