The impact of ending tax-free shopping on the UK and London economies

Introduction

It is widely known that the tourism sector contributes considerably to the UK and London economies. Few events illustrate the extent of this impact better than the COVID-19 pandemic, which led to a series of restrictive lock-down measures that impacted severely on domestic and international tourism to London and the rest of the UK.

In the UK context, the picture is further complicated by a series of challenges related to the 2016 Brexit referendum, such as the ensuing political and economic uncertainty and the depreciation of Sterling. Another issue that is not cited as frequently is the UK’s decision to end its tax-free shopping scheme for international tourists- a decision that took effect on January 1, 2021. The UK ended a scheme (known as ‘VAT-RES’) that allowed international tourists to claim the value-added tax on items purchased during their stay in the country.

This supplement provides the context behind the UK government’s decision, before discussing its potential implications for both the UK and London economies.

Background Information

Tax-free shopping (TFS) is an arrangement whereby products bought but not consumed in the country of purchase are VAT-free. This can happen either via the product being tax-free at the point of purchase, or via the buyer having to obtain a VAT refund after buying it[1]. There are also restrictions on the types of goods that qualify for the relief[2]. The sales tax may be in the form of a goods and services tax (GST), value added tax (VAT), or consumption tax.

Unlike duty-free shopping (which allows consumers to buy products that would normally have excise tax on them tax-free and is usually found only at international terminals such as airports), TFS applies to the GST/VAT/consumption tax component only, and can apply to purchases made in high streets within a jurisdiction as well as at international travel points.

Several countries implement TFS schemes. A 2021 study by the Australian National University found that 63 countries globally, including the 27 EU member states, apply a TFS scheme[3]. EU member states are required to implement a TFS scheme under Article 147 of Council Directive 2006/112/EC (the EU VAT Directive)[4].

The UK was governed by this obligation until 31 December 2020. Under this arrangement, if a person lived outside the EU and travelled to the UK for leisure or business, they were eligible for a VAT refund on items purchased in the UK. The VAT-refund scheme was called the Retail Export Scheme (VAT RES), or tax-free shopping in colloquial terms. Under the UK’s VAT RES scheme, international visitors to the UK could reclaim the VAT they paid on goods that have been purchased but not consumed in the UK.

Why VAT RES was terminated by the UK government

In a move that coincided with the end of the Brexit transition period, the UK government ended VAT RES effective 1st January 2021. In September 2020, it explained its rationale for ending the scheme as follows[5]:

- VAT RES was not the only scheme through which WTO rules and OECD guidelines on paying tax in the country of consumption could be fulfilled. In other words, the officials did not see any risk in ending the scheme when it comes to international guidelines and rules on payment of consumption-related taxes.

- The impact of the scheme across the UK was unclear, and data suggested that a majority of purchases under the scheme happened in London and in Bicester Village. According to the officials, this would indicate that the scheme did not benefit the whole of the UK equally. The Government argued VAT RES was “a costly system to maintain with unclear economic benefits, and […] burdensome for exit points”[6].

- Concerns were raised about the administrative difficulties of VAT RES.

- It was argued that there was a risk that fraud and non-compliance would increase if VAT RES was extended to passengers travelling to the EU[7].

That being said, it is worth noting that VAT-free shopping is still available where a retailer ships goods out of the country at the time of purchase[8]. However, this raises questions about whether such an option would inconvenience tourists.

Government estimates of economic impacts of terminating VAT RES

When forecasting the impact of terminating VAT RES, the OBR said that VAT refunds worth about £500 million had been given via the scheme in 2019[9]. It did also note, however, that while terminating the scheme would generate revenue for the Treasury, it could also lead to reduced shopping by international tourists, especially for luxury items. The OBR forecast that terminating VAT RES would generate a £1.8b saving to the Treasury by the 2025/26 fiscal year, whilst adding the caveat that the figures are highly uncertain[10].

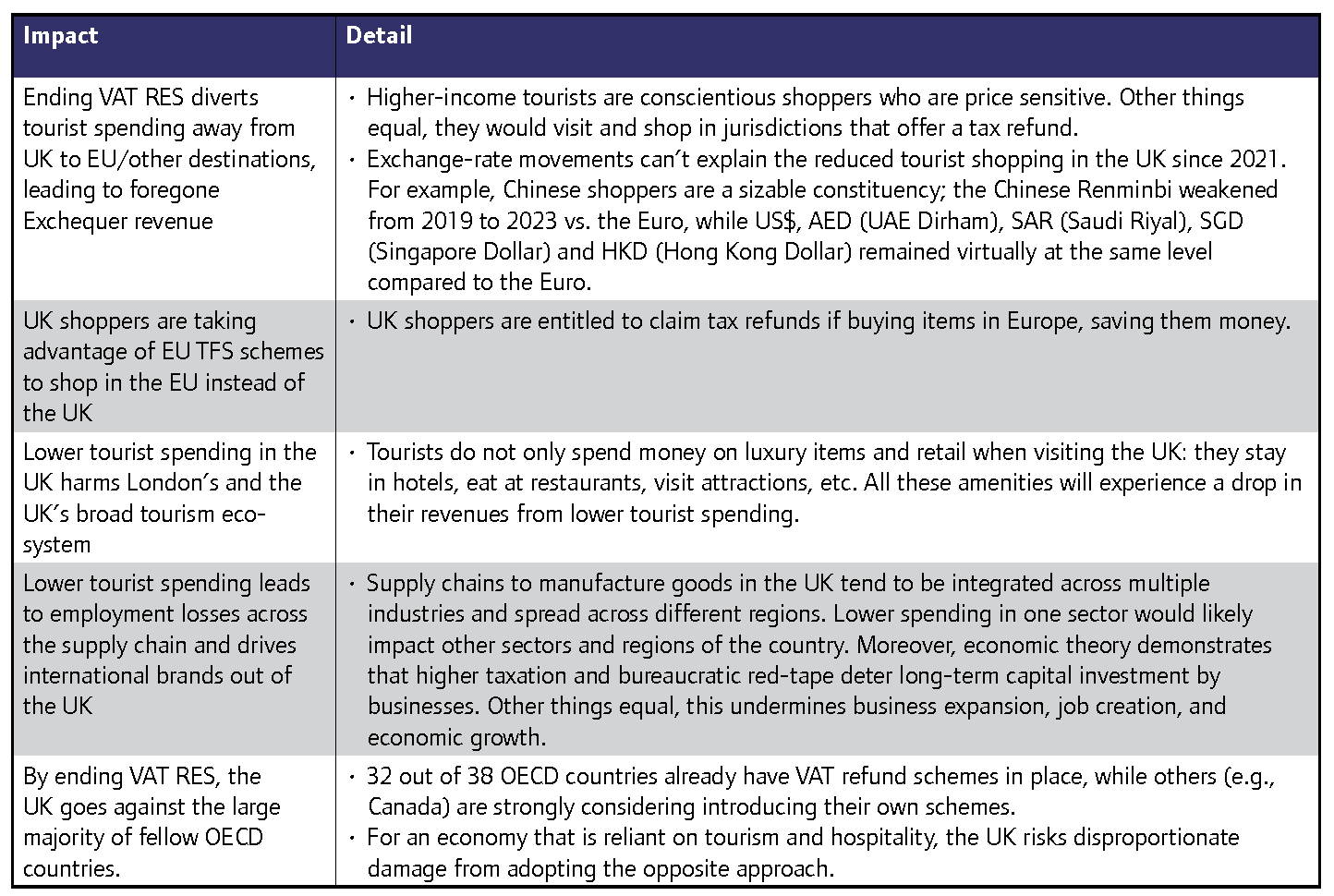

Ascertaining economic impacts of terminating VAT RES

A key challenge to the OBR analysis (typically highlighted by opponents of the government’s decision as well as other economic forecasters (e.g., Oxford Economics)) is that the work did not examine the impact of TFS schemes on retail expenditure and its broad multiplier effects (e.g., increased economic activity in other sectors beyond retail – for example tourism, and more job retention and creation). For instance, Oxford Economics’ modelling of the decision’s impacts suggests that the re-introduction of VAT RES will have a significant positive effect in terms of GDP, tax yield, and job creation[11].

Economic theory suggests that tax-free schemes boost retail spending by tourists[12]. By extension, the increase in consumer spending would increase a country’s GDP and stimulate job creation. Various studies suggest that these effects extend beyond the directly-affected sectors (e.g., tourism and hospitality) to include other sectors (which would form part of the supply chains for items tourists purchase) and regions (as supply chains tend to be dispersed).

As the UK ended the scheme relatively recently, data on the effects is limited. Moreover, the COVID-19 pandemic’s impact on global tourism complicates the picture. Nevertheless, there is recent data that would suggest that the UK is losing out economically to rival jurisdictions as a result of the decision to end VAT RES. The case for the detrimental impact of this decision (and thus, to reinstate tax-free shopping) can be divided into several categories (see table below):

Summary of recent data findings

- According to Global Blue, the world’s largest strategic technology and payments partner within the Tax-Free Shopping, Payment and RetailTech ecosystems, the recovery in tourist spending during 2022 vs pre-pandemic trends has been much lower in the UK than France, Italy, and Spain. Moreover, GCC (Gulf Cooperation Council) tourist spending in these EU countries is at least 1.5x pre-pandemic levels, but is less than 0.7x for the UK.

- Global Blue data also shows that almost 10% of UK spending in 2019 has already been relocated to the EU27 by international shoppers. Meanwhile, Non-EU/UK shoppers who used to shop in the UK and EU27 in 2019 have increased their tax-free spending in the EU27 in 2022 by 30%.

- Chinese tourists typically represent 22% of tourist spending in the UK annually. In a recent Global Blue survey, the UK was shown to be the least favoured destination for Chinese tourists among the large five European countries for their future trips. Moreover, only 42% of Chinese people planning to visit Europe in the next 12 months are planning to visit Britain, down from over 70% in 2019.

- Approximately €500M was spent by UK shoppers in Continental Europe in 2022, representing an increase of about 200% vs. 2021 (£160M).

- According to Value Retail, The Dorchester Group has just announced that its London hotel is underperforming its Paris hotel, which they attribute purely to the end of VAT RES. Meanwhile, Mulberry has just announced the closure of its Bond Street store due to the ending of tax-free shopping.

- According to the New West End Company, 57% of all West End spend was international in 2019, compared to 44% in 2023. 71% of their international visitors said they would spend more if they could claim back VAT on their purchases. This proportion increases to 93% for the highest-spending customers.

- The Canadian government is considering its own TFS scheme, and commissioned a study by CEBR to forecast potential economic impacts. The study revealed that a TFS scheme could have increased 2019 GDP by CAD 810 million. In terms of labour market benefits, the boost to visitor spending would support an additional 32,100 jobs in the travel and tourism industry and its supply chains. This would bring a potential net gain of CAD 127 million in overall tax revenue. Equivalently, for each dollar lost through lack of VAT, CAD 1.90 would be recouped in other taxes. The estimate of total additional tourist spending due to TFS is CAD 407 million.

Final considerations

During 2023, several media and retail-led campaigns were started to reinstate VAT RES. For example, in August, the Mail on Sunday stated that 350 brands, including Harrods, Marks & Spencer, Burberry, and Harvey Nichols, had backed its campaign, alongside 40 Conservative MPs[13]. It’s also worth noting that should the UK reinstate VAT RES, it would become the only major European country where EU residents could shop tax-free, opening-up a whole new market for regional airports and the areas they serve.

Therefore, it is safe to suggest that the impact of terminating VAT RES extends beyond a few London-based luxury retailers: it will negatively affect a broad range of London’s business population and workforce, in addition to suppliers and manufacturers across the whole of the UK – with long-term economic costs that would far outweigh any short-term accrued savings.

[1] Wang T and Stewart M. The law and policy of VAT tourist tax refund schemes: A comparative analysis (PDF; Working Paper 19/2021), Tax and Transfer Policy Institute, November 2021

[2] Ibid.

[3] Ibid.

[4] EUR-Lex – 02006L0112-20200101 – EN – EUR-Lex (europa.eu)

[5] HM Treasury and HMRC, A consultation on the potential approach to duty- and tax-free goods arising from the UK’s new relationship with the EU: Summary of responses (PDF), GOV.UK, September 2020.

[7] Ibid.

[8] Tax on shopping and services: Tax-free shopping – GOV.UK (www.gov.uk)

[9] https://obr.uk/docs/dlm_uploads/CCS1020397650-001_OBR-November2020-EFO-v2-Web-accessible.pdf

[10] Ibid.

[11] Oxford Economics, Assessing the impact of tax-free shopping in the UK – a report for the Association of International Retail (AIR), November 2022.

[12] Dimanche (2003).

[13] https://www.dailymail.co.uk/news/article-12005245/Business-leaders-call-Chancellor-Jeremy-Hunt-reinstate-tax-free-shopping-overseas-visitors.html