London's Economy Today - October 2021 editorial

Budget and Spending Review

Yesterday, the Chancellor presented the October 2021 Budget and Spending Review, with both taxes and public spending set to rise firmly in the coming three years. While some of the most eye-catching policies had been previously announced (rising National Insurance Contributions) or revealed in the days before the speech (ending the public sector pay freeze), there were still some surprises. These ranged from extending existing policies, like cancelling the rise in fuel duty for another year, to comprehensive overhauls, like simplifying the alcohol duty system, to the surprise announcement of a larger envelope for overall departmental spending increases to £150 billion a year in cash terms by 2024-25.

The unexpectedly strong increase in public spending comes on the back of hefty upward revisions to economic and fiscal forecasts from the Office for Budget Responsibility (OBR). The OBR now expects real GDP to grow 6.5% in 2021, up from 4% in their March outlook, and with growth expected to hold at 6% in 2022 before returning to more normal levels, while the long-term scarring effect of the pandemic on UK GDP has been eased to 2% from a previous estimate of around 3%. Combined with a sharp increase in forecast inflation and the budget’s tax increases, the OBR suggested that the Chancellor had an extra £50 billion per year in fiscal headroom. With the budget deficit set to roughly halve both this year and next, by 2024-25 borrowing is set to be nearly £12 billion lower than expected even before the pandemic. This leaves debt, which was previously expected to climb to around 110% of GDP, stabilising below 100% of GDP this year and then falling gently across the forecast period.

With this forecast fiscal windfall in hand, the Chancellor opted to significantly increase spending across Whitehall, with average real terms spending increasing 3% in the coming three years. This included an estimated real-terms increase of 3% a year in core spending power for local authorities and a significant spending increase for the wider Department of Levelling Up, Housing and Communities’ local government mandate. Other highlights on the spending side included real average annual growth in the NHS day-to-day budget of 3.8%, £4.7 billion for the core schools budget bringing per-pupil spending in England back to 2010 levels, £3.8bn of extra spending on skills by 2024-25 and a 2.9% increase in public sector gross investment, including pre-announced infrastructure projects for regions outside London. On the revenue side, there was tax relief for cultural venues, R&D investment, HGV operators and domestic flights, while the bank corporation tax surcharge stayed in place and a new air passenger duty band was introduced for long-haul flights. There were also announcements on the labour market, with a well-telegraphed rise in minimum wages seeing the National Living Wage rising to £9.50 an hour, while a surprise came in the form of reducing the Universal Credit (UC) taper rate from 63% to 55%.

There were relatively few London-specific announcements, though some areas within the capital are set to benefit from levelling up and regeneration schemes. Six areas, including Brent and Tower Hamlets, are set to benefit from almost £65 million local infrastructure improvements through the Levelling Up Fund. Just over £3 million of the estates regeneration share of the Brownfield Land Release Fund will go to London areas. London will also get around a third of the spending from the Affordable Homes Fund, will see five Community Diagnostic Centres and some portion of the 10 new hospitals being built in London and the South East. The UC taper reform will also help some of the 390,000 Londoners currently receiving UC while employed, though it will not benefit the 600,000 unemployed Londoners receiving UC.

The Chancellor also set out new fiscal rules, including a falling debt to GDP ratio within three years, no borrowing to fund day-to-day spending within three years, public investment at no more than 3% of GDP and welfare spending conforming to an agreed cap. The OBR suggested that the budget and spending review were on track to meet all these targets (Figure 1) but noted that the headroom was around a sixth of the average forecast error for the debt to GDP ratio. With acute risks to the forecast for inflation and interest rates, it remains to be seen if the forecast-based fiscal windfall that the budget relied upon will ultimately materialise.

Figure 1:

Higher inflation ahead, despite new data’s false peak

September’s inflation data appeared to offer a reprieve from growing price pressures, but this is likely to prove a false peak, with inflation set to rise further in the coming months. Data from the Office for National Statistics (ONS) showed that Consumer Price Index (CPI) annual inflation eased to 3.1% from 3.2% in August, but a key part of the decline was a softer contribution from restaurant prices due to the timing of the Eat Out to Help Out scheme in 2020. Without this distortion, August inflation would have been 2.7%, meaning September’s figure is better seen as part of a continued acceleration in price pressures.

In September, the biggest contribution to annual inflation came from transport prices, which were up more than 8% year-on-year (y/y). Once again, this was a mixture of higher fuel prices leading to 8.6% y/y inflation in operating costs and the ongoing semiconductor shortage pushing up the cost of purchasing vehicles to an even faster 9.6% y/y. The challenge faced from supply chains can be seen in other data, with the fortnightly ONS business survey showing 37% of importers reporting moderate or severe disruptions in October and the London PMI gauge for input prices hitting a record high of 70.6 in September.

Following the Bank of England’s (BoE) August projection that inflation would peak at around 4% y/y in the later part of this year, recent communications suggest concerns around inflation are growing at the Bank. This may mean a higher projection in the November Monetary Policy Report, which would increase pressure to raise interest rates. Outside the Bank, the OBR now expects inflation to peak at 4.4% in Q2 2022, while the Centre for Economics and Business Research (CEBR) forecast UK inflation to peak at 5.7% y/y in November – the highest since the early 1990s. In recently commissioned research, CEBR also used consumption data to rebalance the UK CPI components to match the mix of spending in London. Based on these calculations, CEBR expects London to see even higher inflation of over 6% late this year (Figure 2).

Figure 2:

While supply chain challenges may well persist for some months with periodic localised Covid outbreaks in major ports or production facilities around the world lengthening the problem, the consensus among commentators is that these will ease over the coming year. There are several reasons for this expectation. Firstly, higher prices should prompt suppliers to ramp up production, easing shortages. This may take longer in the case of particular industries, such as the highly-concentrated semiconductor industry. Secondly, market signals suggest that shipping costs should ease from early next year. Thirdly, some early examples of tight supply chains raising costs have already unwound, with one example coming from US lumber prices, which have eased from peaks in May. Fourth, global demand for goods is also likely to normalise as the pandemic comes under control. However, it is worth acknowledging uncertainty around these points. The strength of supply chain difficulties has already come as a surprise to most forecasters, including the Federal Reserve. Risks remain to the outlook, including persistent COVID-19 outbreaks disrupting shipping, a resurgence of tensions between the US and China disrupting technology supplies and Brexit raising costs for importers.

Rising wage costs offer risk of longer-lasting inflation

Beyond supply challenges, there are some signs that inflation is becoming entrenched in expectations, and that wage pressures may be rising ahead of productivity growth. Both these trends could make the acceleration of prices more permanent. Citi and YouGov polling points to rising year-ahead inflation expectations, up 1 percentage point (ppt) to 4.1% in September. Meanwhile the ONS vacancies survey found in September that around one in eight businesses across all industries have found vacancies harder to fill than usual, and BoE data suggests that this is leading to higher pay awards. The Q3 2021 Agents’ Summary of Business Conditions survey saw the index for recruitment difficulties reach its highest level since the early 2000s, while the index for labour costs per employee hit a record level (Figure 3).

Figure 3: Bank of England recruitment difficulties and labour cost indexes, standardized

Source: Bank of England, GLA calculations

At a sectoral level, vacancies are also generally higher where there were large numbers of furloughed workers towards the end of the scheme. Given we might otherwise expect these workers to be rehired, leaving no need for a posted vacancy, this positive correlation points to skills mismatches or geographical mismatches between available labour and vacancies. This suggests a reallocation of labour within and between sectors ahead, which may push up wage growth as employers try to attract workers to fill specific workforce gaps.

With furlough coming to an end and the economy continuing to recover, labour shortages are expected to ease in the medium term. Institute for Fiscal Studies (IFS) analysis also finds that a majority of jobseekers face sharp competition for each vacancy, so higher pay awards may be concentrated in areas of scarce skills. These points are consistent with the fact that real wages are up less than 2% in annualized terms compared with 2019. However, in this area, as with supply chain risks, there is uncertainty around the outlook. If skill shortages are more structural, perhaps due to home working-related geographical reallocation of services or lower immigration, inflationary wage pressures ahead of productivity growth may prove more persistent.

Growth in UK output recovers

Outside of concerns around inflation there is evidence of the continued bounce back of the economy. Thus, the ONS first estimate for GDP growth in August was 0.4%, up from a revised estimate for July of -0.1%. Output remains 0.8% below its peak in February 2020. The largest contributions to growth were in Accommodation and food services at 0.28ppt, Arts, entertainment and recreation at 0.13ppt, and Information and communication at 0.13ppt. There was, however, an offsetting fall in Health activities of -0.42ppt. The lifting of lockdown restrictions in July would have been of particular benefit to the first two sectors.

Business confidence remained positive in August, as apparent from the indicators section later in this report. Although, as discussed above, there are downside risks to growth in the coming months from supply chain and labour market constraints curtailing activity and feeding into inflation. The possible re-introduction of restrictions as COVID-19 cases rise is also a risk, while the latest ONS retail sales show that sales volumes fell by 0.2% in September and have fallen each month since April when non-essential retail re-opened. Indicative of the shift in spending towards goods they are still 4.2% higher than their pre-pandemic February 2020 levels.

End of the furlough scheme may have had

a soft landing

The latest ONS data shows that London and UK unemployment rates continued to fall in the three months to August, as reported in the indicators section. For the UK, in July to September, the estimated number of vacancies recorded was at its highest level since records began, with the majority of industries growing on the quarter. In the same period there were 3.7 vacancies for every 100 employee jobs, also a record high.

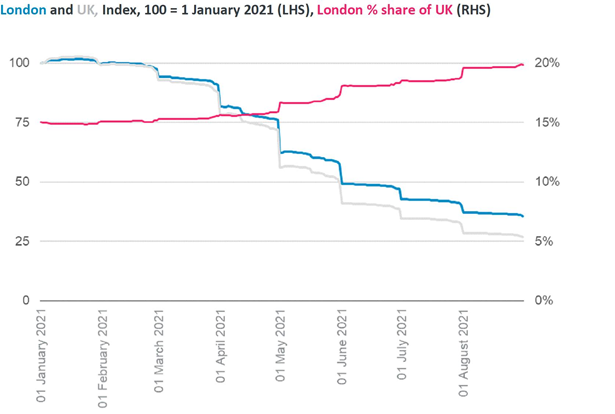

One concern, particularly for London, is that the Coronavirus Job Retention Scheme (the furlough scheme) ended on 30 September. Over 2021 in the months to August, people on furlough in London fell by nearly two-thirds, and across the UK by nearly three-quarters. The return of people to work has made a significant positive contribution to the economy, alongside some of the out-of-work finding jobs. At the same time, there were around 263,000 London residents on furlough at the end of August whose future was unclear. With furlough numbers declining more rapidly in the rest of the country, London’s share of UK furloughed employments had risen from 15% to 20% over the course of the year (Figure 4).

Figure 4:

Positively, the evidence is that larger businesses have predominantly taken back staff on furlough. The number of employers planning 20 or more redundancies in September remained close to record lows. Just over 200 firms in Great Britain notified the Insolvency Service of their plans with a total of slightly under 14,000 jobs at risk. Major travel and transportation companies reported not making redundancies because of the end of the furlough scheme despite making extensive use of the scheme. This includes British Airways, Easyjet, Jet2, Ryanair, Tui, Virgin Atlantic, Hays Travel, Airbus, DHL, air traffic controller NATS, baggage handler Swissport, as well as Gatwick, Heathrow, Manchester and Stansted airports.

What has actually happened in smaller businesses is not clear at the present time, but workers at smaller employers may not have been so fortunate. In January, employers with under 20 employees accounted for 40% of furloughed employees, but this proportion had risen to 60% by the end of August.

There are concerns for the small business sector

The Bank of England BoE has published an updated assessment of the financial stability of the UK and its corporate sector. It judges that UK corporate debt vulnerabilities have increased moderately over the pandemic so far. It has, though, been concentrated in some sectors and types of businesses, in particular in Small and Medium-sized Enterprises (SMEs). Debt held by SMEs increased by 25% between December 2019 and March 2021, compared with less than 3% for large enterprises. The BoE estimates that around 757,000 of around 2 million SMEs now hold debt, and that the share of SMEs with debt has more than doubled over the pandemic. In summary, the BoE notes, “as the economy recovers and government support, including restrictions on winding up orders, falls away, business insolvencies are expected to increase from historically low levels”.

Tensions escalate between the UK and the EU

Almost three months after the UK demanded far-reaching reform of the Brexit deal’s trading arrangements for Northern Ireland, (the protocol), the European Commission proposed more limited changes. The UK wanted to eliminate most checks on goods going from Great Britain to Northern Ireland, while the EU has made proposals which could end as much as 80% of current checks. The UK has rejected the proposals as not going far enough, and not meeting its demand for an end to the role of the European Court of Justice in oversight of the Northern Ireland protocol. If the UK and the EU fail to find an accommodation, and the dispute escalates, there is a risk of a trade war with each side imposing tariffs on goods imports.

UK services trade with the world, and the EU, has fallen since the start of the pandemic reflecting the effects of restrictions on activities. The UK left the Single Market at the beginning of this year after the conclusion of the transition period, and restrictions on trade with the EU came into effect. Services trade, both exports and imports, continued to fall both with the EU and beyond suggesting that the effects of the pandemic continue to have the most effect. For example, services associated with travel and transport have fallen this year. The aggregate trend seems to have stabilised, though, in Q2 of this year. Curiously, it is service imports from the EU which have fallen most (Figure 5).

Figure 5:

The global recovery is becoming more

imbalanced

The International Monetary Fund (IMF) in its latest World Economic Outlook reports that the momentum behind the global recovery has weakened because of the pandemic – so far, there has been close to 5 million deaths. Global growth has been revised down marginally to 5.9% in 2021 (from 6.0% in July), and is unchanged for 2022 at 4.9%. Expected UK growth has also been revised down in 2021 to 6.8% (from 7.0%) and marked slightly up in 2022 to 5.0% (from 4.8%).

The IMF reports, though, a divergence in economic prospects across countries. There are more difficult near-term prospects for advanced economies, in part due to supply disruptions. The outlook for low-income developing countries has deteriorated considerably due to worsening pandemic dynamics. Partially offsetting these changes, projections for some commodity exporters have been upgraded on the back of rising commodity prices. These economic divergences are a consequence of large disparities in vaccine access and policy support.

Business confidence in London remains positive

The indicators below show that business confidence in London has remained positive in Q3. The latest Capital 500, the Quarterly Economic Survey by the London Chamber of Commerce and Industry provides some more granularity. Two fifths (39%) of firms expect profitability to increase over the coming 12 months, while the share expecting a decline shrunk from 25% to 17%. As COVID-19 restrictions were lifted the cashflow of businesses jumped sharply. 26% of businesses reported an increase in cashflow in Q3 compared with the previous three months, similar to the proportion in the Q2 survey. The proportion reporting a decrease fell from 33% in Q2 to 27% in Q3. More than two-fifths (43%) of firms said that they were operating at full capacity in Q3, a two-year high and back in line with the pre-pandemic average. It may be worth noting that fieldwork for the survey was completed prior to the latest round of gas price increases, and the shortage of tanker drivers became apparent.

GLA Economics will continue to monitor these challenges over the coming months in our analysis and publications, which can be found on our publications page and on the London Datastore.