London's Economy Today - January 2022 editorial

The omicron wave in London has begun to decline

After peaking at over 26,000 towards the end of December the seven day average of people testing positive for COVID-19 has been declining in the capital, with it dropping to around 11,000 by mid-January. Although the infection rates in London and the rest of England remain above the levels seen before the surge in infections from the Omicron variant, the Government announced that “Plan B” measures such as compulsory face masks in enclosed and crowded places and covid passes for large venues would not be renewed when they ran out yesterday, 26 January, while the advice for workers to work from home ended last week.

This announcement is likely to provide some boost to businesses which had seen a decline in confidence due to the emergence of the Omicron variant. This was shown in the Bank of England’s Decision Maker Panel for December 2021, which showed that UK businesses expected sales to be 7% lower in Q1 2022 than would have been the case without the pandemic with employment expected to be 4% lower. While, in London the Q4 2021 Capital 500 survey of businesses for the London Chamber of Commerce and Industry (LCCI) found that around a third of surveyed businesses felt that the economic prospects for London would worsen. Commenting on the results Richard Burge, Chief Executive of the LCCI said the survey “shows the severity of Omicron’s impact on London business and business leaders’ outlooks on the local and national economies. Against the period of growing optimism witnessed in the third quarter, the results of this survey are a stark reminder of the tumultuous conditions businesses are trading in”.

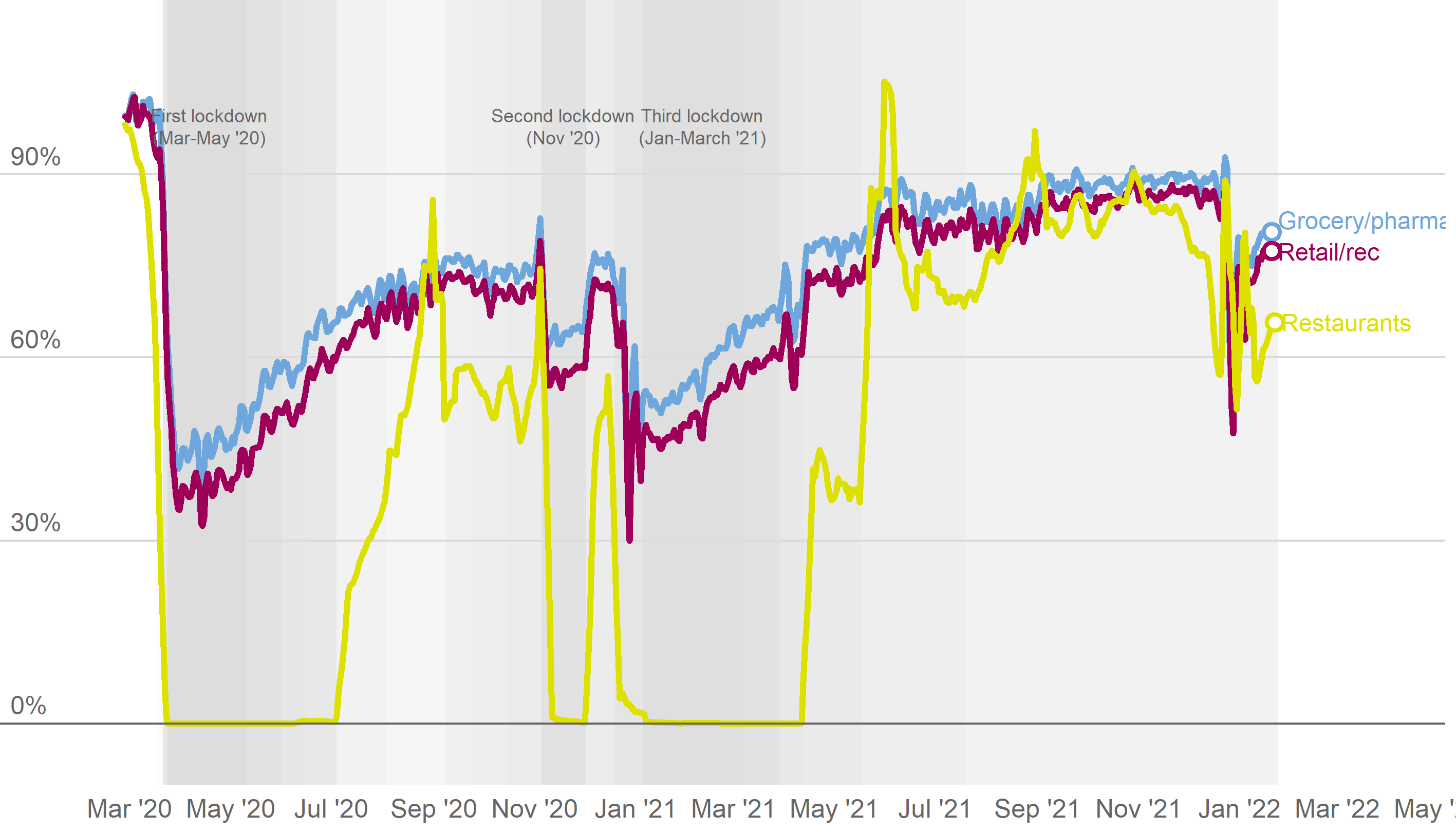

Parts of the capital’s economy also face ongoing challenges such as the hospitality sector with the estimated number of diners in London restaurants remaining below pre-pandemic levels according to OpenTable data analysed by the Office for National Statistics (ONS). Thus, on 2 January the ONS found seated diners at London restaurants stood at 91% of the level seen on the same day in 2020. This compares unfavourably to the UK as a whole which saw levels at 134% on the same period. On the other hand, London may not have seen quite as sharp a fall in retail sales as the rest of the UK, with Mastercard anonymised transaction data showing retail spending declining by around 0.6% in London compared to the national contraction of 3.1% in retail sale values. Nevertheless, other consumer-facing indicators for London also remain below pre-pandemic levels (Figure 1).

Figure 1: Individual personal activities in London, March 2020 – January 2022, relative to pre-COVID-19 baseline

Source: Grocery and retail metrics from Google Mobility, social venues (bars, event spaces etc) from Purple public Wifi and restaurant bookings from OpenTable

Unemployment continues to fall in London

Data published by the ONS in January showed that unemployment in London continued to fall towards the end of last year. In the three months to November 2021 London’s unemployment rate was 5.4%, a decrease of 0.4 percentage points (pp) on the previous quarter and a fall of 1.7pp from a year earlier. However, this was still above the UK unemployment rate of 4.1%, which decreased by 0.4pp on the previous quarter and a by 1.0pp on the year earlier.

Looking at more timely data on payrolled employees from HMRC’s Pay As You Earn (PAYE) Real Time Information (RTI) dataset also showed an improving labour market in December. There were around 4.2 million payrolled employees living in London in December 2021, an increase of around 30,500 or 0.7% on the previous month. This was an increase of 239,000 or 6.1% on the previous year (December 2020) against a UK average increase of 4.8% (Figure 2). Relative to pre-pandemic levels (February 2020), the number of payrolled employees in London was up by 6,780 or 0.2%. This compares to an increase of 1.4% across the UK on average.

Figure 2:

Nationally the ONS’s Business Insights and Conditions Survey showed a tight labour market particularly in certain sectors. Thus in late December “15% of businesses reported a shortage of workers, which has remained broadly stable since late October 2021” with the highest percentage being in the accommodation and food service activities industry.

UK inflation at a near 30-year high

December’s inflation reached 5.4% year-on-year, the fastest price growth in nearly 30 years (since March 1992). The increase in prices was broad-based, but the largest contributions came from vehicle fuels (0.7ppts), second hand cars (0.5ppts), electricity (0.4ppts) and gas (0.3ppts); this reflects the influence of supply chain challenges and rising global energy costs.

In terms of the sharpest current price pressures, Londoners ordinarily devote a similar share of outlays to energy bills as an average UK household and spend less on owning and operating vehicles. Yet by some measures, London still faces a worse inflationary outlook. The National Institute of Economic and Social Research (NIESR) estimates of trimmed-mean inflation, which seeks to cut out the most volatile prices using a regionally collected dataset, was running at 5% year-on-year for London, compared to 4% for the UK overall. This placed London as the UK region facing the highest inflation – which has been the case in NIESR’s figures since April 2021. London’s inflation has at times run as much as 2.5 percentage points faster than the UK average.

There are good reasons to expect current high inflation to dissipate over time. Shipping costs and business survey gauges of backlogs have both eased, pointing to some improvement in supply chain challenges. Market signals from futures contracts point to oil and natural gas prices easing in the coming months, if gradually. However, with cost challenges having spread across the entire economy and even service price inflation above 3% year-on-year, price increases are still likely to run well above the Bank of England’s 2% target for more than a year. What’s more, with the Ofgem standard tariff set to increase by around £400 for the average annual gas bill in April, CPI inflation may well not peak until the spring.

The Bank of England’s November 2021 projections anticipated inflation ending 2022 at 3.4% year-on-year and communications from them in December indicated that they have revised up their expectations of the April inflation peak by around 1 percentage point. As a result, February’s Bank forecasts are likely to project inflation above 3% well into 2023.

UK GDP returns to pre-pandemic levels

In more positive news for the economy, the UK’s output level had surpassed in November 2021 its pre-pandemic level. Thus, with the economy growing by 0.9% in November, compared to growth of 0.2% in October, it went above its February 2020 level for the first time by 0.7% (Figure 3).

Figure 3:

All major sectors of the economy grew between October and November 2021, with services output increasing by 0.7%, production by 1.0% and construction by 3.5%. The output of the services and construction sectors are now both 1.3% above their pre-pandemic levels but the production sector’s output remains 2.6% below its February 2020 levels. However, within the services sector although it grew by 0.8% in November, the output in consumer-facing services are still 5.0% below their pre-pandemic levels.

IMF downgrades its global growth forecast for this year

The latest World Economic Outlook report from the International Monetary Fund (IMF) has firmly downgraded global growth in 2022 as ongoing virus disruptions, reduced fiscal and monetary stimulus, and high inflation drag on the prospects for growth. The IMF’s forecasts envision global growth of 4.4% in 2022, down 0.5pp from its October projections, and 3.8% in 2023. While the 2023 figure is a 0.2pp upgrade, the IMF observed that this is largely a mechanical effect as headwinds to global growth ease in the second half of 2022.

Advanced economy inflation is projected to average 3.9% this year (up 1.6pp from October) and 2.1% in 2023 (up 0.2pp), while emerging market inflation is forecast at 5.9% and 4.7% in 2022 and 2023 respectively (up from 4.9% and 4.3%). The IMF estimates that the shocks to energy prices and supply chains last year have pushed up estimates of global core inflation by 1pp.

Across the world, the main drags on growth come from the US, whose projected 4% growth in 2022 is down from an October expectation of 5.2%, and China, where the IMF sees growth of 4.8% this year, down 0.8pp from October. The US faces reduced fiscal stimulus expectations after President Biden’s Build Back Better bill ran into what may be insurmountable roadblocks, alongside high inflation leading to a much more rapid expected pace of monetary tightening from the Fed. Meanwhile China’s continuing ‘Zero COVID’ policy may disrupt the economy as retrenchment in its property sector also drags on aggregate demand. More broadly, the IMF sees advanced economies growing an average of 3.9% this year (from 4.5% in October) and 2.6% in 2023, while emerging economies are set to average 4.8% growth in 2022 (from 5.1% in October) and 4.7% growth in 2023.

Within the wider pool of advanced economies, the UK receives a more modest downgrade to its growth prospects, with the IMF envisioning a GDP increase of 4.7% in 2022 and 2.3% in 2023. The 2022 figure is down 0.3ppts from its October projections, while the 2023 forecast receives a 0.4ppts boost. While the 2023 figure might be encouraging, the IMF’s projection for Q4/Q4 growth at the end of next year is just 0.5%, pointing to limited momentum moving into the medium term.

London’s tourism sector continues to face a challenging time

New analysis of visitor nights in London has recently been published. This indicated that in the final quarter of 2021 domestic and international visitor nights in London were down 40% on the equivalent quarter in 2019, while associated spend was down by 60%. Looking forward the numbers of overnight stays and associated spend is not expected to reach pre-pandemic levels until at least 2025. The boss of Heathrow airport, John Holland-Kaye, has also warned that a return to normal travel “could be years away” as data showed there was just 19.4 million passengers who passed through Heathrow in 2021, 12.3% below the 2020 number. To aid the recovery of air travel the Government has announced plans to encourage airlines to increase the number of flights they provide, with them having to use their landing slots 70% of the time from 27 March or hand them back to the airports. Currently airlines only have to use their slots 50% of the time, this compares to a pre-pandemic requirement of 80%.

Looking at the wider impact of the pandemic the Centre for Cities has published analysis looking at the impact of the pandemic on sales on the high street. This found that between March 2020 and September 2021 London lost the equivalent of 47 weeks of sales. Still, despite these challenges it is likely that with the easing of the latest wave of COVID-19 infections, London’s economy will see continued growth into the new year. GLA Economics will continue to monitor this situation over the coming months in our analysis and publications, which can be found on our publications page and on the London Datastore.