London's Economy Today - editorial September 2023

UK GDP falls in July

Data published by the Office for National Statistics (ONS) this month showed that the UK economy contracted by 0.5% between June and July (Figure 1). Although a drop had been expected this was more than most economists had been predicting. Despite this monthly drop output was 0.2% higher in the 3 months to July.

Figure 1:

Output in the service, production and construction sectors all fell between June and July, by 0.5%, 0.7% and 0.5% respectively. Looking at the service sector, a sector of particular importance to London’s economy, the ONS observed that at the UK level “output in consumer-facing services showed no growth in July 2023, while all other services fell by 0.6%”. However, within that “the largest negative contributions came from retail trade, except of motor vehicles and motorcycles (down 1.2%) and travel agency, tour operator and other reservation service and related activities (down 3.2%)”. In attempting to explain the drop in GDP seen in July the ONS observed that “there were some common themes that were anecdotally reported” these included the impact of industrial action and the wet weather in that month.

The ONS revises up the UK’s post pandemic recovery

Still notwithstanding this poor news in recent GDP data the ONS did also produce revised estimates of the UK’s post pandemic economic growth. This significantly increased the rate of recovery for the UK economy in 2021, while also reducing the size of the drop in the economy in 2020. The ONS now estimates that GDP fell by 10.4% in 2022 rather than a previously estimated drop of 11.0%. Growth in 2021 is now estimated at 8.7% rather than the previous estimate of 7.6%. This means that the ONS now estimates that the UK economy was 0.6% above its pre-pandemic peak by the final quarter of 2021, rather than the previous estimate of it being 1.2% smaller. These revisions mean that rather than having the worst post pandemic recovery of any G7 economy, the UK’s recovery is now just behind France and Italy’s and ahead of Germany’s. Although it should be noted that these countries have not so far undertaken methodological revisions to their 2021 data.

Inflation unexpectedly falls in August

ONS data published this month showed that Consumer Price Index (CPI) inflation unexpectedly dropped in August. CPI inflation stood at 6.7% in the year to August down from 6.8% in July (Figure 2). Most economists had expected the figure to pick up in part due to rising oil prices.

Figure 2:

The ONS noted that the largest downward contribution to inflation “came from food, where prices rose by less in August 2023 than a year ago, and accommodation services, where prices can be volatile and fell in August 2023”. Whereas “rising prices for motor fuel led to the largest upward contribution to the change in the annual rates”. Core CPI which excludes energy, food, alcohol and tobacco also fell. It thus rose at an annual rate of 6.2% in August down from 6.9% in July. Services inflation, which along with core inflation is often seen as a good indicator of underlying inflation also dropped back to 6.8% in August down from 7.4% in July.

British Retail Consortium (BRC) data also showed slowing price rises in shops in August. Their data showed that prices in shops increased by 6.9% in August down from 8.4% in July. However, the BRC did note that increases in alcohol taxes had pushed up these figures with their chief executive, Helen Dickinson, observing that “these figures would have been lower still had the government not increased alcohol duties earlier this month”.

There was also good news on wages this month with ONS data showing in the three months to July the annual growth in UK average pay (excluding bonuses) stood at 7.8%. Including bonuses, the figure stood at 8.5%. Still, despite real wages now growing research by the Resolution Foundation published this month projected that there will be zero real growth for median non-pensioner household income in 2024-25. With them further seeing “zero growth also projected for 2023-24 and 2025-26… a three-year stagnation, following a sharp income fall in 2022-23”. This stagnation they said was due to the impact of higher taxes and mortgage costs and the end of government cost of living payments.

Majority of Londoners just about managing or struggling

Looking at the impact of the cost of living crisis in London, new polling by YouGov for the GLA[1] found that although the crisis may no longer be worsening it is still having a big impact on Londoners. Thus, it found that:

- The proportions of Londoners ‘struggling financially [2] (21%) and ‘just about managing’ (32%) have held in August compared to July.

- Whilst the top two ways to manage living costs remain spending less on non-essentials (51%) and buying cheaper products (50%), the next 8 actions are taken by significantly fewer Londoners (see Figure 3) and cluster around similar proportions (around a quarter of Londoners overall).

- ‘Financially struggling’ Londoners are around twice as likely to be buying less food and essentials than the average Londoner (52% versus 26%) and about three times as likely to be going without essentials (18% versus 6%).

- A much larger proportion of ‘Financially struggling’ Londoners are ‘looking for a better-paying job’ (24% v 15%), ‘using more credit or going into debt’ (26% v 11%) and ‘borrowing money’ (29% v 8%) when compared to all Londoners.

Figure 3:

Bank of England ends its run of interest rate rises

With the surprising drop in the rate of inflation in August and some weakening national indicators such as PMIs the Bank of England’s Monetary Policy Committee (MPC) voted by 5 votes to 4 to maintain UK interest rates at 5.25%. This was the first time in 15 consecutive meetings at which the MPC chose not to increase rates.

Even before this hold in interest rate increases, some mortgage lenders had been reducing some of the rates on their products. This was in part due to financial markets anticipating the possibility of some cuts in rates starting next year. Despite this house price data from the Nationwide showed the average UK house price was down 5.3% in August compared to a year earlier. This was a drop of over £14,600 and the biggest fall since 2009. They also reported that mortgage approvals were 20% below their pre-pandemic levels. The Halifax also reported house price drops in August. They stated that average UK prices dropped 4.6% in the year or by around £14,000. However, it should be noted official ONS data still shows house price growth at the UK level, if not for London.

Although property prices may be easing this has not been accompanied by an easing in rental costs according to data from the estate agents Hamptons. This data showed that nationally monthly rents on new let properties were up 12% year-on-year in August to over £1,300 per month. While in London this was even higher with average rentals increasing by 17% to over £2,300. ONS data for all private rentals although showing high rental cost rises are less eyewatering with it finding London’s annual private rental prices increased by 5.9% in August. This was the highest rate in England and the highest recorded rate in the capital since data collection began in January 2006.

Forecasters become more pessimistic for the global economy next year

Internationally there remains concern for the prospects of the global economy. In an aggregation of forecasts for the global economy the consultancy Consensus Economics found that forecasters on average expect it to grow by 2.1% in 2024 down from an expected growth of 2.4% this year. This in part is due to a belief that inflation will be persistent for longer leading to central banks raising interest rates further, and holding them high for longer.

As an example of rising global interest rates and in a reaction to continued inflation in the Eurozone the European Central Bank (ECB) raised interest rates in the Zone to a record high in September. Rates now stand at 4% up from 3.75%. However, despite global expectations of further rate rises more rises in the Zone may not occur soon with the ECB stating that “the governing council considers that the key ECB interest rates have reached levels that, maintained for a sufficiently long duration, will make a substantial contribution to the timely return of inflation to the target”. Looking at the prospects for the Zone’s economy the latest forecast from the European Commission, which was published this month, expects its economy to grow by 0.8% in 2023 and 1.3% in 2024.

UK agrees deal to re-join the Horizon science programme

Beyond the current economic situation the adjustment to the UK’s post Brexit institutions continues with the UK agreeing a deal to rejoin the EU’s Horizon science programme in September. This deal, which has to be approved by all EU member states, will make the UK an associate member of the programme. The UK had negotiated associate membership back in 2020 but this had been held up due to disputes about Northern Ireland’s trading rules.

Elsewhere, research by the think tank UK in a Changing Europe has looked at the investments undertaken by the post Brexit UK backed public sector lenders set up to replace the investment from the European Investment Bank (EIB). This research found that these successor investment banks invested just 17% as much in 2022 as the EIB had been investing in the UK before it wound down its investments in preparation for Brexit.

Payrolled employee numbers stay stable in London

The national and international economic situation remains weak, but there remains strength in London’s economy. As an example, although, as shown in the indicators section of this publication, ONS employment data shows a decline, other indicators are more positive. Hence, the count of payrolled employees from HMRC’s Pay As You Earn (PAYE) RTI dataset, which offers a timely measure of labour market trends, shows that there were around 4.3 million payrolled employees living in London in August 2023 according to early estimates, unchanged on the previous month. This data although stable on the previous month represents an increase of 73,800, or 1.7%, on the previous year (August 2022) against a UK average increase of 1.5%. Relative to pre-pandemic (February 2020) levels, the number of payrolled employees in London was up by 165,000, or 4.0%. This compares to an increase of 3.9% across the UK on average.

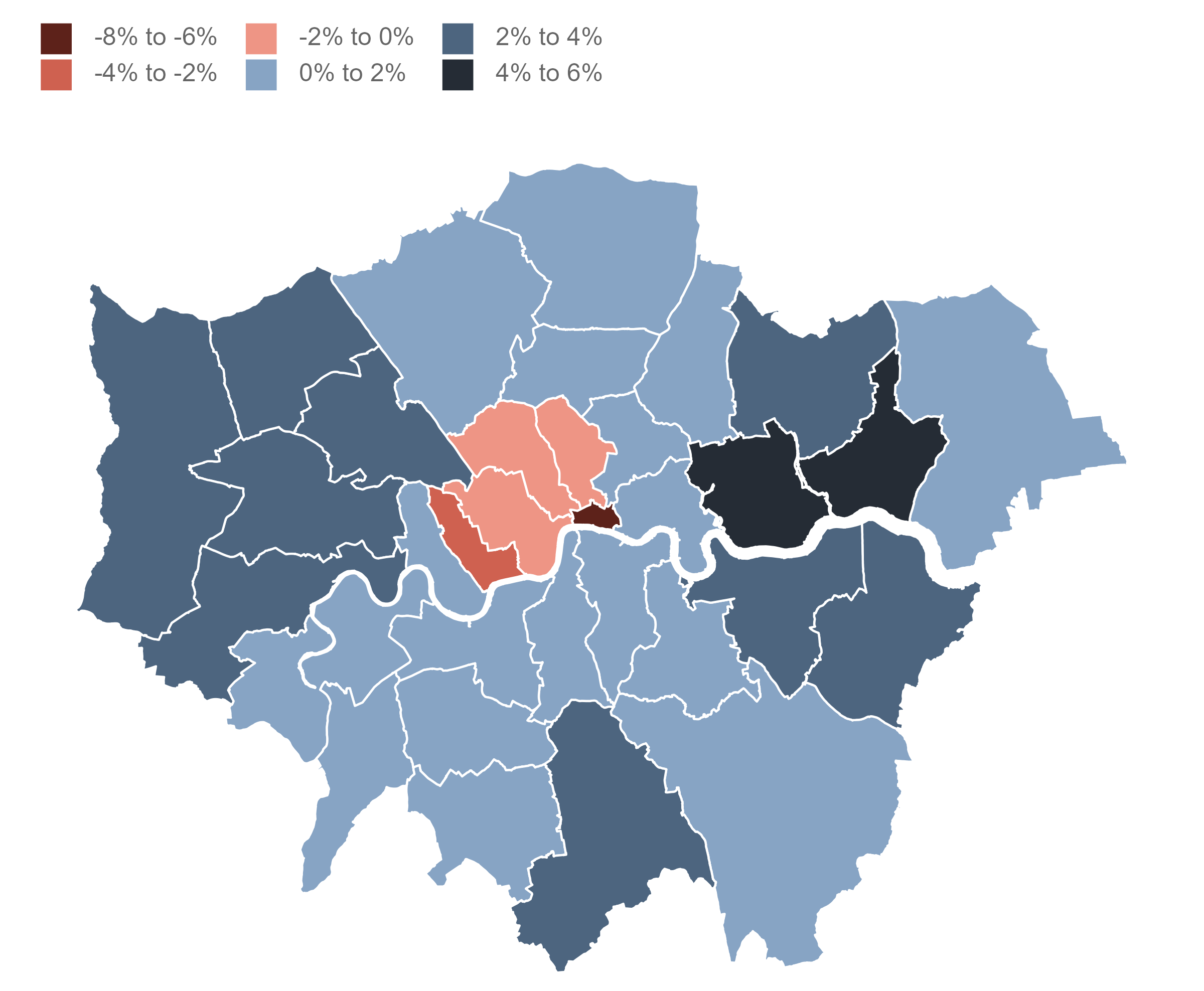

There is however a lot of variation in the change in payrolled employee numbers by London local authority (Figure 4). The number of payrolled employees living in Barking and Dagenham, the borough with the highest growth (excl. the City), was up by 4.7% on the year in August 2023. While, the borough with the lowest growth, Kensington and Chelsea, recorded a decrease of 2.6%.

Figure 4: Changes (%) in payrolled employees by London local authority, comparing August 2023 levels with the year earlier

Source: HM Revenue and Customs – Pay As You Earn Real Time Information. Contains Ordnance Survey data Crown copyright and database rights [2015].

Note: Estimates are based on where employees live.

The RTI dataset also provides information on the nominal monthly pay of payrolled employees living in London. This showed in August that median monthly pay in London was £2,700, an increase of 5.4% on the year. However, this increase was lower than the UK as a whole where median pay was £2,260, up by 6.7% on the year.

Looking at other data for London’s economy gives a mixed picture for its current performance. So, as shown in the indicators section for this publication, consumer confidence in London was very strong in September especially when compared to the UK. However, some of the PMIs for London were either stagnant or showed slight declines. GLA Economics will continue to monitor all these trends and other aspects of London’s economy over the coming months in our analysis and publications, which can be found on our publications page and on the London Datastore.

[1] All figures, unless otherwise stated, are from YouGov Plc. Total sample size was 1072 adults. Fieldwork was undertaken between 18th to 24th August 2023. The survey was carried out online. The figures have been weighted and are representative of all London adults (aged 18+). GLA cost of living polling can be found at https://data.london.gov.uk/gla-cost-of-living-polling/2/

[2] ‘Struggling financially’ comprises of those who responded ‘I am having to go without my basic needs and /or rely on debt to pay for my basic needs’ or ‘I’m struggling to make ends meet’ when asked about their current financial situation.