London's Economy Today - editorial - October 2022

Reverberations of mini-Budget continue to echo through the economy

Last month’s LET editorial discussed the tax cuts (worth £45 billion in 2026/27) announced in the mini-budget on 23 September 2022. The current Chancellor of the Exchequer, Jeremy Hunt, has reversed £32 billion worth of these measures, including the planned reductions in corporation tax, and the basic and additional rates of income tax. Remaining tax changes include the cut in National Insurance, which GLA Economics analysis shows would benefit higher earners disproportionately, and more growth-friendly measures such as cuts to stamp duty and an increase in the annual investment allowance for corporation tax.

Further, the Energy Price Guarantee will now only apply for six months, and not two years as stated last month. After this point, HM Treasury will implement a more targeted and less expensive scheme.

These measures take significant steps to address the gap in the government’s fiscal plans, and help put debt on a more sustainable footing. More will be needed. The Institute for Fiscal Studies (IFS) Green Budget suggested that tightening of around £60 billion was needed to have debt falling as a share of national income in the medium term. Press reports suggest that Office for Budget Responsibility (OBR) analysis points to a larger gap of £72 billion. The public finances have deteriorated since the last OBR forecast in March. This is not least because expectations of economic growth have worsened due to higher than expected inflation, as well as the response of central banks to raise interest rates. One other effect of the mini-Budget was that it was inflationary, and would have led the Bank of England to raise interest rates to levels higher than they would otherwise have been.

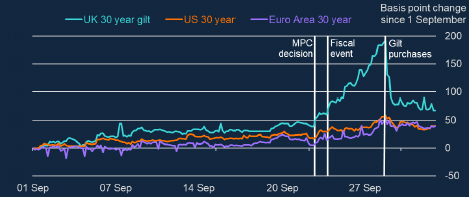

As noted in last month’s LET editorial, there was volatility in financial markets after the mini-budget. Thirty-year government bond, or gilt, yields rose markedly in a way which did not happen for other major economies (Figure 1). The Bank intervened to calm financial markets, and bring rates down towards previous levels, with a 14-day operation to buy gilts.

Figure 1: Cumulative change in long-term government bond yields since 1 September 2022

Source: Bank of

England calculations of Bloomberg data

The Government has also acted to re-assure financial markets. It has pre-announced certain measures (as described above) and been clear that there will be an OBR forecast to accompany its Medium Term Fiscal Plan which is now set for the 17 November having previously been scheduled for the 31 October. The OBR’s economic and fiscal forecast will provide evidence of the Government’s commitment to place debt on a more sustainable footing. With the next Monetary Policy Committee meeting of the Bank to review interest rates on the 3 November it is hoped fiscal and monetary policy will be more coordinated.

Despite this policy response, there have been longer-term effects from the uncertainty generated by the mini-budget. Three credit agencies – Fitch, Moody’s and S&P – have placed the UK on a “negative” outlook. The Bank has delayed its programme of selling bonds, or quantitative tightening. And mortgage interest rates are higher than they would otherwise have been. The average two-year fixed rate deal, which was priced at 2.43% at the start of December 2021, has now increased to around 6% according to Moneyfacts.

Household finances come under further strain as the cost-of-living crisis bites deeper

Inflation picked up to a 40-year high last month, with the Consumer Price Index (CPI) rising to 10.1% in the year to September 2022, according to figures from the Office for National Statistics (ONS). This comes before the Energy Price Guarantee (EPG) is set to raise the average cost of household energy bills by around 25% in the month of October, meaning higher readings are likely this winter.

The cost of living continues to increase, with prices for core essentials rising rapidly. Food price inflation soared to an annual rate of 14.8%, Figure 2, with prices for some staples rising even faster. Milk prices rose over 30% year-on-year, and flour prices were up 29.6%. Lower-income households devote more of their spending to food and energy, meaning these price increases are likely to worsen inequalities in London.

Figure 2:

While the EPG is set to freeze household energy costs from October for six months, we now know that the scheme will be scaled back from April 2023. Based on current projections using the Ofgem price cap methodology, abandoning any form of the EPG would add 3 percentage points or more to inflation from the spring. The deterioration of the pound against other currencies will also raise the cost of imported goods. The drop in the value of the pound since August alone could add another percentage point to the rate of inflation.

Housing costs are also set to increase. Asking rents in London are growing around 11% year-on-year according to HomeLet, while the rise in long-term interest rates following the mini-budget will start to feed through into mortgage interest payments. It will take time for these impacts to be felt fully – as households renew rent or mortgage contracts – but those households already facing the new costs will see a tight squeeze.

YouGov polling of Londoners commissioned by the GLA gives a picture of the challenges ahead. Already in September, one in five Londoners said they were financially struggling, with another one in three ‘just about managing’. This means that a majority of Londoners now fall under these two categories – a stark change from January, when nearly 60% of Londoners were either ‘coping OK’ or ‘comfortable’ financially. Around 11% of Londoners have fallen behind on bills and 13% have fallen behind on credit commitments. The polling also shows that while 9% of Londoners are starting to go without essentials to manage higher costs, that proportion rises to 28% among financially struggling Londoners.

Retail sales feeling the squeeze

As rising prices erode households’ spending power, this is impacting on consumer demand. UK retail sales volumes, excluding vehicle fuel, fell by 1.5% in September 2022, ONS figures indicate. Sales volumes have trended downwards since April 2022, with the latest reading falling below pre-pandemic levels.

While these figures were impacted by the bank holiday for the state funeral of HM Queen Elizabeth II, broader trends are also at play. Food stores were the biggest negative contribution to retail sales over this time, with food retailers pointing to rising prices as a key driver in falling sales. Non-store retail sales also fell sharply, but remain well above pre-pandemic levels as consumer preferences have shifted towards online shopping.

The outlook for retail sales looks bleak at the national level, with consumer confidence falling to another record low of -49 in September. Households in London are less pessimistic, with a score of -29, but this is still one of the worst readings since the financial crisis. And after continuing to climb firmly for months, counter to national trends for retail spending, card spending data for London may be showing signs of levelling off (Figure 3).

Figure 3:

Forecasts of global growth fall further

There are pressures on the world economy stemming from the recovery from the pandemic, the effects of the war in Ukraine, and higher food and energy prices. In its latest World Economic Outlook, the International Monetary Fund revised downwards its projections. It now forecasts the lowest global growth profile since the global financial crisis and the acute phase of the COVID-19 pandemic. This reflects significant downturns for the largest economies with a US GDP contraction in the first half of 2022, a Eurozone contraction in the second half of 2022 from rising energy prices, and weakness for China from prolonged COVID-19 outbreaks and lockdowns (as well as mounting challenges in the property sector). A particular downside risk to the outlook is if monetary policy by the leading central banks miscalculates the right stance to reduce inflation. Global growth is forecast to slow from 6.0% in 2021 to 3.2% in 2022 (as in the July update), and 2.7% in 2023 (0.2 percentage points down from the July update). The UK economy slows over these years from 7.4% to 3.6% in 2022 (up 0.4 percentage points) to 0.3% in 2023 (down 0.2 percentage points).

The UK economy is contracting

According to the ONS, UK economic output (Gross Domestic Product) fell by 0.3% in August, after increasing by 0.1% in July. Health made the largest contribution to the decline of 0.11 percentage points, followed by the Arts at 0.08 percentage points, and Accommodation and food services at 0.06 percentage points. Activity increased in other sectors with Professional services contributing 0.1 percentage points, and Information and communication contributing 0.05 percentage points.

Over the three months to August, UK GDP fell by 0.3%. However, the UK economy is not yet in recession going by the technical definition of two successive quarters of negative growth.

Labour supply continues to shrink restraining the productive potential of the economy

Despite this, the unemployment rate in London fell to a record low (4.0%) in the three months to August 2022, according to the ONS. The UK unemployment rate also fell to a new record low in this period (3.5%). London’s employment rate for June to August 2022 was 75.1%, while the UK rate was 75.5% – both little changed from a year earlier. More worryingly, the inactivity rate, the measure of those not looking and/or not available to work, rose for both the capital and the UK, reaching 21.7% for both geographies in the three months to August. For London this represented an increase of 1.3 percentage points from a year earlier, and for the UK an increase of 0.5 percentage points on the year (Figure 4).

Figure 4: Economic inactivity rates, London and the UK, 2015-2022

Source: ONS Labour Force Survey

Note: The margin of error is not published for London, the UK margin is +/- 0.4%. March 2020 indicated by dotted line.

This marks a reverse of pre-pandemic trends, when inactivity rates were declining. According to analysis by the Financial Times (FT) if trends at the UK level from January 2015 to 2020 had continued there would be 0.7 million fewer inactive people aged 16-64 than there currently are. The UK is the only country in the developed world where people have continued to drop out of the labour market in ever greater numbers beyond the acute phase of the pandemic.

The number of working age people unable to work due to chronic pain has climbed by almost 200,000 over the past two years relative to its former trajectory, reports the same FT article. Almost 40% of the rise in economic inactivity is explained by people with a mental health issue that limits their ability to work.

Increased illness due to COVID-19 will also be impacting on labour supply, although not everyone with the virus is of working age. An estimated 2.3 million people in private households in the UK (3.5% of the population) were experiencing self-reported long COVID as of 3 September reports the ONS. In contrast, 1 in 35 people in England, 2.78% of the population, were suffering from COVID-19 in the week ending 3 October.

London’s economy feels the strain

The LET indicators of business confidence in London remain positive in September. However the latest London Chamber of Commerce and Industry (LCCI) Q3 quarterly survey for London finds that the external headwinds to the economy have resulted in a decidedly pessimistic outlook. Business confidence has waned with weaker domestic sales, lower cashflow, and high cost pressures. Two thirds (66%) of companies expect the UK’s economic growth to worsen over the next 12 months and only 13% of firms believe the UK’s economy will improve, down from 19% in Q2. A third (32%) of companies now think their own profitability will worsen over the coming year, up from 26% in Q2. Pessimism in overall company economic prospects dropped to its lowest level since before 2018.

London’s service exports buck the national trend during the pandemic

Restrictions on movement during the pandemic have contributed to a fall in both goods and services exports at the UK level in 2020, according to ONS analysis. Total UK exports fell by £75 billion to £572 billion, with a fall of £59 billion in goods exports, and a fall of £15 billion in services exports. London exports fell by £3 billion to £180 billion, with a fall of £12 billion in goods exports offset by a rise in services exports of £8 billion (Figure 5). The capital benefited from a £15 billion increase in Finance exports, of which £10 billion came from Inner London West, where the City of London is located.

Figure 5:

GLA Economics will continue to monitor these and other aspects of London’s economy over the coming months in our analysis and publications, which can be found on our publications page and on the London Datastore.