London's Economic Outlook: Spring 2023 Executive Summary

GLA Economics’ 42nd London forecast[1] suggests that:

- London’s real Gross Value Added (GVA) growth rate is forecast to be 1.1% in 2023 as the cost of living crisis slows down the post-pandemic economic rebound. Growth is expected to improve to 1.8% in 2024 and 2.2% in 2025.

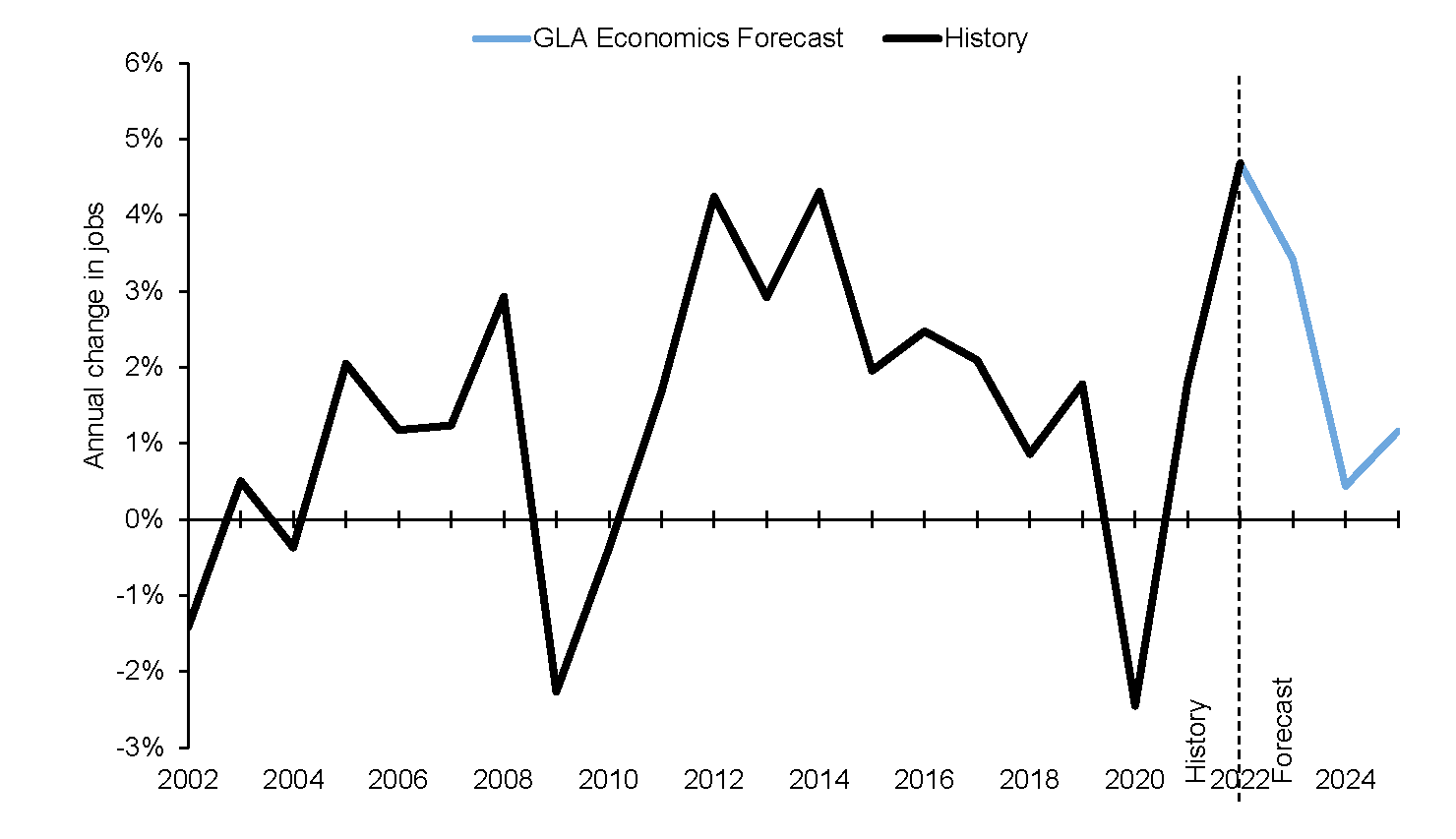

- London is forecast to see a 3.4% rise in the number of workforce jobs[2] in 2023, although this will slow sharply in 2024 (0.4%) and ease towards longer-term averages in 2025 (1.2%).

- Household income is forecast to decline this year by 0.5%, after a contraction in 2022, followed by a firm recovery, with growth of 2.5% in 2024 and 2.9% in 2025.

- Household spending barely grows in 2023 (up 0.3%), as despite the cost of living crisis households release savings accrued during the pandemic. Expenditure rises 1.6% in 2024 and 3.1% in 2025.

Table 1.1 summarises this report’s forecast growth rates for GVA, jobs, household expenditure, and household income. Unprecedented levels of uncertainty prevail due to the cost of living crisis, the war in Ukraine and the aftermath of the pandemic. As a result, the forecasts presented in this document should be interpreted as a baseline scenario for London’s economy in the medium-term. This is the most likely scenario in GLA Economics’ judgement, but there are a wide range of plausible alternatives.

Table 1.1: Summary of economic forecasts under GLA Economics reference scenario

| Annual growth rates (per cent) | 2022[3] | 2023 | 2024 | 2025 |

| London GVA (constant 2019, £ billion) | 7.2% | 1.1% | 1.8% | 2.2% |

| Consensus (average of independent forecasts) | 0.4% | 1.3% | 1.9% | |

| London workforce jobs | 4.6% | 3.4% | 0.4% | 1.2% |

| Consensus (average of independent forecasts) | 0.5% | 1.0% | 1.3% | |

| London household expenditure (constant 2019, £ billion) | 6.8% | 0.3% | 1.6% | 3.1% |

| London household income (constant 2019, £ billion) | -0.5% | -0.5% | 2.5% | 2.9% |

| Memo: Projected UK RPI[4] (Inflation rate) | 11.6% | 9.1% | 3.9% | 2.6% |

| Projected UK CPI[5] (Inflation rate) | 9.1% | 6.8% | 2.9% | 2.0% |

Source: GLA Economics’ Spring 2023 forecast

Since the Autumn 2022 LEO[6], economic news has centred on two trends: inflation and economic activity both running higher than expected. Russia’s invasion of Ukraine is a humanitarian disaster, and the disruption to energy supply it has created has had dire consequences for the global economy. In the UK, this has led to a cost of living crisis as weaker purchasing power makes us all poorer. Yet UK economic data has shown continued resilience to this shock, leading to widespread near-term forecast upgrades. A strong labour market and a buffer of savings left over from the pandemic among richer households seem to be supporting consumer spending and overall activity. London has outperformed the wider UK in recent data, so upside surprises for the country should mean a resilient outlook in the capital.

But celebrations would be premature. While a UK recession now appears less likely, the outlook is still weak. Projections from the Bank of England and the Office for Budget Responsibility (OBR) point to little growth momentum this year. And medium-term challenges persist due to the UK’s low investment compared to other major economies, a lingering increase in economic inactivity after the pandemic and slower trade growth after Brexit. London remains the UK’s region with the highest productivity, and a hub for foreign investment and trade, but it is unlikely to escape these long-term challenges entirely.

The latest UK economic data demonstrate the balance between easing pessimism, but limited optimism. After contracting 11% in 2020 due to the pandemic shock, UK GDP grew 7.6% in 2021 and 4.1% in 2022. Yet this strong growth still leaves the UK economy slightly smaller than before the pandemic. Since Q2 2022, GDP has stagnated, with quarterly growth between +0.1% and -0.1%. So while the UK has avoided two successive quarters of contraction – technically dodging a recession – the cost of living crisis has ground the economy to a halt. The latest data show flagging momentum going into the spring, with GDP falling 0.3% in March 2023, after a flat month in February and 0.5% growth in January. While consumer spending overall increased in Q1 2023, consumer-facing sectors of the economy have struggled.

Employment data also reflect weaker momentum across the UK. The unemployment rate ticked down to 3.8% in the three months to April 2023, though this is higher than last summer’s lows of 3.5%. Vacancies fell by 7% in the three months to May, suggesting the demand for workers is cooling. Yet the average number of unemployed people per vacancy, at 1.2, is still near record lows. Employment increased 0.8% in the three months to April, with a decline in economic inactivity making up part of the improvement. It is possible that some workers may be propelled back into the labour market as the cost of living makes joblessness unaffordable. The inactivity rate has fallen gently since last summer, but labour market participation remains lower than before the pandemic. Immigration may be another part of the explanation for higher participation and employment. Total UK net migration reached a record annual level of 606,000 in 2022, surprising on the upside.

The key reason for caution in the near term is rising prices. CPI inflation eased to 8.7% year on year in April, but this was higher than projected. Given that energy bills surged in April 2022, the year-on-year comparison in April 2023 should have sharply improved. But the upward surprise was broad-based. Food inflation is at its highest since the 1980s, and this is beginning to exceed the pressure from energy bills. Stripping away volatile price categories, core inflation reached a new 31-year high of nearly 7% in April. And the poorest households are hit hardest by the surging costs of essential goods. As a result, news of avoiding a recession may prove scant comfort for those on low incomes.

To fight these impacts, macroeconomic policy has had to respond dramatically. The Bank of England is engaged in its sharpest rate hiking cycle since the 1980s, and fiscal policy has seen another injection of spending to help protect households from the surge in energy costs. Both these are essential measures, but they may have challenging implications for the outlook. The longer inflation continues to outpace expectations, the higher interest rates are likely to go, dragging on the economy over time. To maintain fiscal credibility, the Government is raising taxes to their highest share of income since the 1960s, and plans painful spending cuts from next year onwards.

Tighter monetary policy is also affecting the financial sector. As interest rates rise and central banks unwind their post-pandemic asset purchases, some banks are seeing their balance sheets come under strain. Three medium-sized US banks have gone under, along with the collapse of Credit Suisse in Europe. These lenders stood out as risky, and a wider financial crisis may not be brewing. But less-regulated, non-bank parts of the financial system could pose risks. And the US Federal Reserve recently trimmed its forecast to suggest that tighter lending conditions will put the US into a mild recession later this year. International headwinds offer another reason for caution in the outlook.

London’s economy shows more grounds for optimism, though it faces many of the same risks as the wider UK. The capital’s economic output exceeded pre-pandemic levels by the end of 2021 in a rapid recovery. Revised figures show London’s Gross Value Added (GVA) rose 7.8% in 2021, after a 10.6% drop in 2020. While this is only slightly better than the national average, experimental quarterly data suggest that the capital’s momentum was very strong across 2021. The data has continued to show firm growth, with London’s GDP up 6.8% year-on-year in Q3 2022. While we expect momentum to have pulled back in late 2022 and into 2023, our baseline sees London continuing to outpace the wider UK.

Jobs growth has been even more striking. With the Coronavirus Job Retention Scheme (CJRS), or ‘furlough’ cushioning the labour market, workforce jobs fell only 2.3% in London in 2020. While the 1.6% increase in 2021 was moderate, 2022 saw jobs surge 4.7%. At the start of 2023, jobs growth reached a record rate of increase of 6.4% on the year. Yet in London too, the unemployment rate has been rising, reaching 4.5% in April 2023, up from lows of 4% last summer. Inactivity rates have been volatile.

Survey data also point to greater resilience in London. Businesses in the capital have largely shrugged off the disruptions from higher inflation, with the headline PMI only dipping below neutral for two months in late 2022. The index is now back to its post-pandemic levels, and above long-term averages. Meanwhile households look surprisingly optimistic. Consumer confidence, where 0 indicates a neutral reading, rocketed from -19 in March to +13 by May. This is the fastest increase on record, and stands in stark contrast to the national average, still languishing at -27. The rapid improvement is even more surprising considering that the GLA’s own polling shows that more than one in five Londoners (22%) are financially struggling, with the share increasing slightly in the last two months[7].

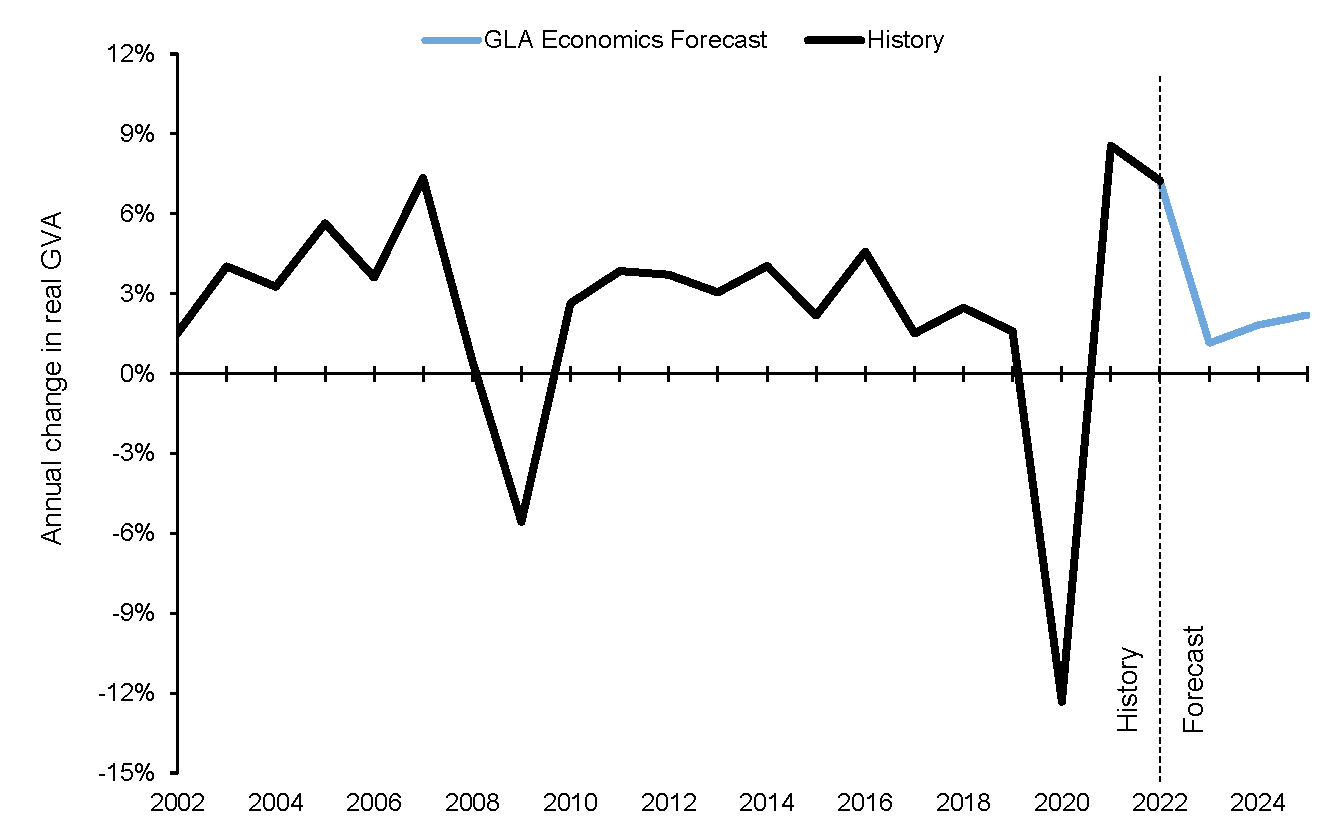

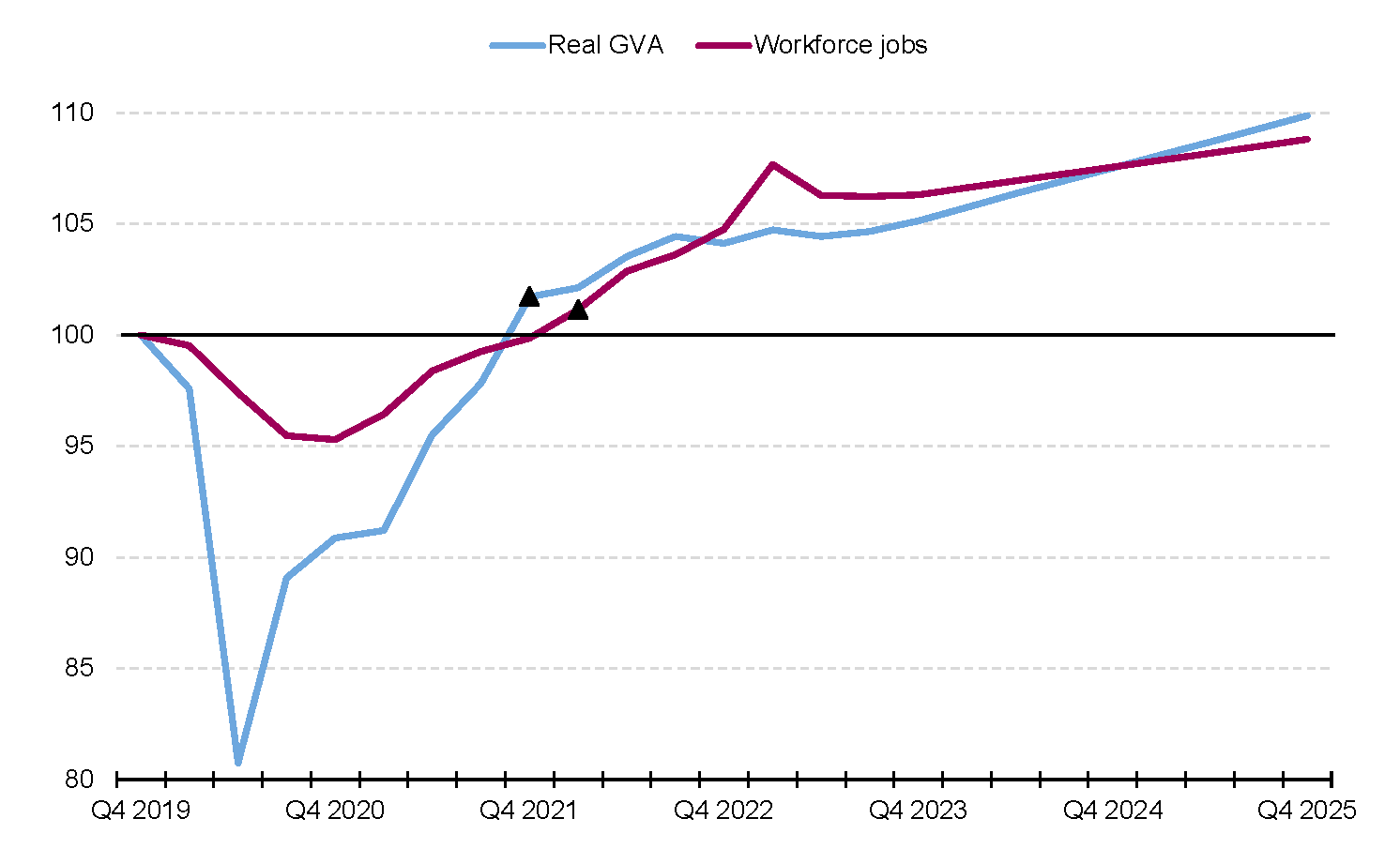

Given this background, the GLA Economics reference scenario for London sees the capital’s output slowing this year, but to an upwardly-revised 1.1%. Growth should recover near to long-term rates in 2024. Employment growth is expected to outpace output this year given the momentum from 2022 (see Figures 1.1 & 1.2 for more detail). The continued effects of high inflation on incomes are likely to drag on consumer-facing sectors in the near term. Higher interest rates will hit manufacturing and real estate, and pose challenges to the financial sector. But we expect other core services to prove resilient due to an improved global outlook and London’s continued agglomeration benefits. Neither jobs nor output are set to fall into a recession, let alone return below pre-pandemic levels (Figure 1.3).

The economic outlook for both London and the UK is subject to a high level of uncertainty. Inflation has likely peaked, but how long it takes to reach the 2% target is unclear. The slower this convergence, the harsher is the likely reaction from monetary policy, and the greater the risk of financial dislocations. An impending US recession could also affect London worse than the rest of the UK due to its higher trade exposure to the world’s largest economy. And the housing market represents a risk to the outlook. London house prices, which are down nearly 4% since last August[8], are a shock to owner-occupiers’ household wealth, while average rents up nearly 5% on the year[9] cuts into other households’ budgets.

In the longer term, the impact of Brexit continues to pose a risk to the economic outlook. The agreement of the Windsor framework on the movement of goods through Northern Ireland has eased the risk of a full-blown trade war. However, with the UK-EU trade agreement not covering services, non-tariff barriers (NTBs) making imports more expensive and the end of freedom of movement cutting EU migration, many issues remain. In particular, recent evidence suggests NTBs have raised the price of food[10], making Brexit a meaningful factor in the cost of living crisis. And while nationally, the fall in EU net migration has been outweighed by the rise in non-EU net migration, London has benefited less from this trend.

Other risks could also play a role in the medium term. At home, a large fiscal deficit and high levels of debt could prompt further tax rises and spending cuts, dragging on the economic recovery. And cuts to planned public investment projects could dent the economy’s long-term potential. Productivity growth remains an issue for the UK economy, and London’s has been even weaker than the national average since 2008. Further stagnation could put the capital’s status as a global city and a business hub at risk. Across the world, US-China decoupling, slowing globalisation and a trend towards protectionism threaten global potential growth. The rise of green technologies offers upside potential in the medium term, but the race to cut carbon emissions also carries risks around trade, capital scrappage and sectoral reallocation. The war in Ukraine has shown how major conflicts can affect the global economy, so if rising geopolitical tensions spilled over into armed clashes, this could rapidly change the outlook. And the impact of Artificial Intelligence technologies on work and the economy remains unclear.

In response to elevated uncertainty, GLA Economics has developed macroeconomic scenarios[11] around our baseline, which we update regularly to reflect changing conditions.

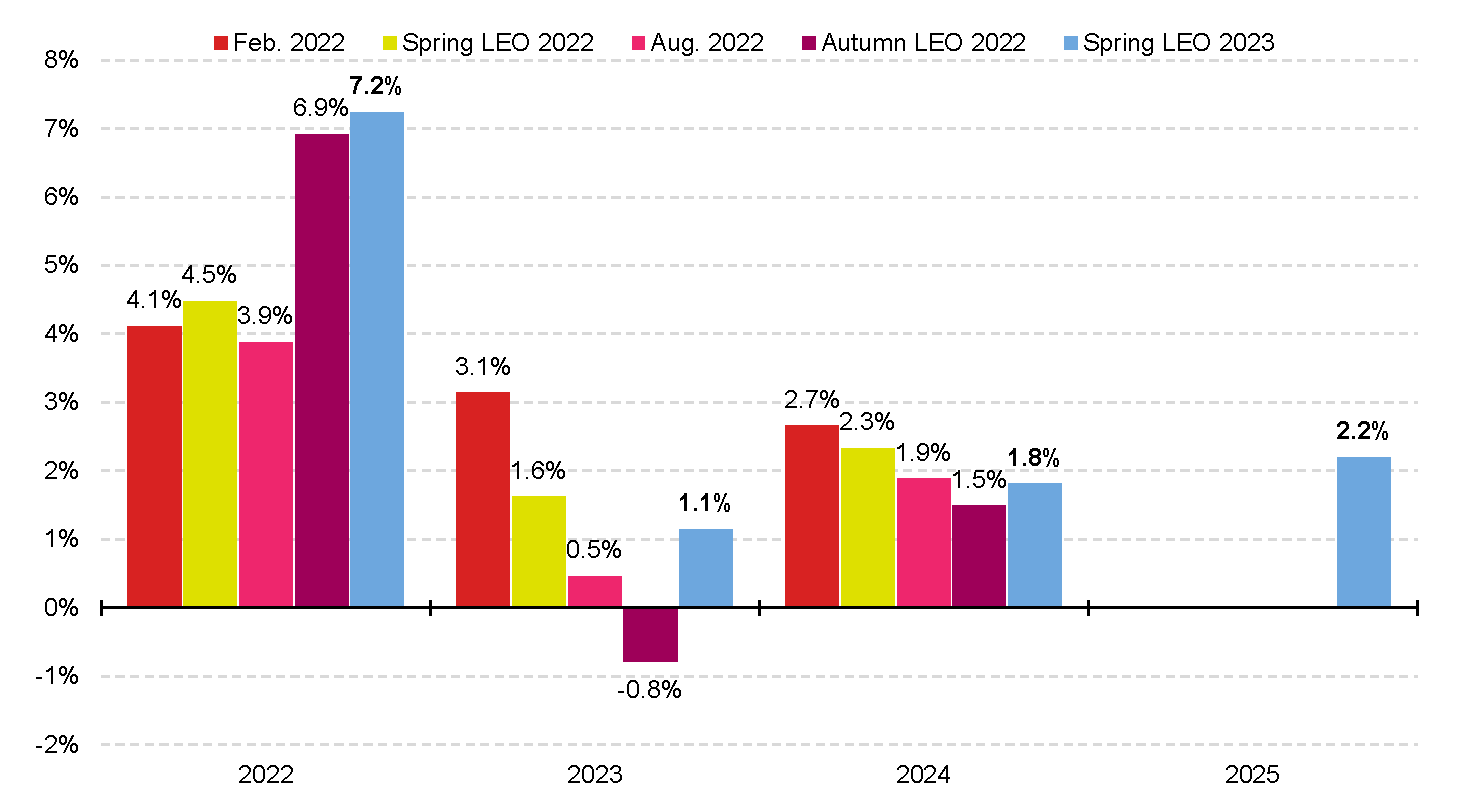

In conclusion, the macroeconomic environment has improved, despite the cost of living crisis, as shown in the evolution of our London Forecast (Figures 1.4 & 1.5). After an unprecedented drop in output in 2020, there has been a good recovery. But growth is expected to slow significantly this year, and output looks unlikely to return to pre-pandemic trends. Jobs growth has been strong, and while we expect a sharp deceleration, employment looks unlikely to go into reverse. London, along with the UK, looks likely to avoid a recession, but many risks cloud the outlook. Inflation, the war in Ukraine, rising interest rates, Brexit and other pressures combine with the still-evolving fallout from the pandemic. As London’s economy restructures in response, it is still unclear what the ‘new normal’ will look like.

Figure 1.1: Historic and forecast output growth (GLA Economics reference scenario)

Source: GLA Economics estimates for historic data and GLA Economics’ calculations for forecast

Figure 1.2: Historic and forecast employment growth (GLA Economics reference scenario)

Source: GLA Economics estimates for historic data and GLA Economics’ calculations for forecast

Figure 1.3: Expected shape of economic recovery under the GLA Economics reference scenario (index)

Source: GLA Economics; Note: Triangles mark the point at which pre-pandemic levels reached

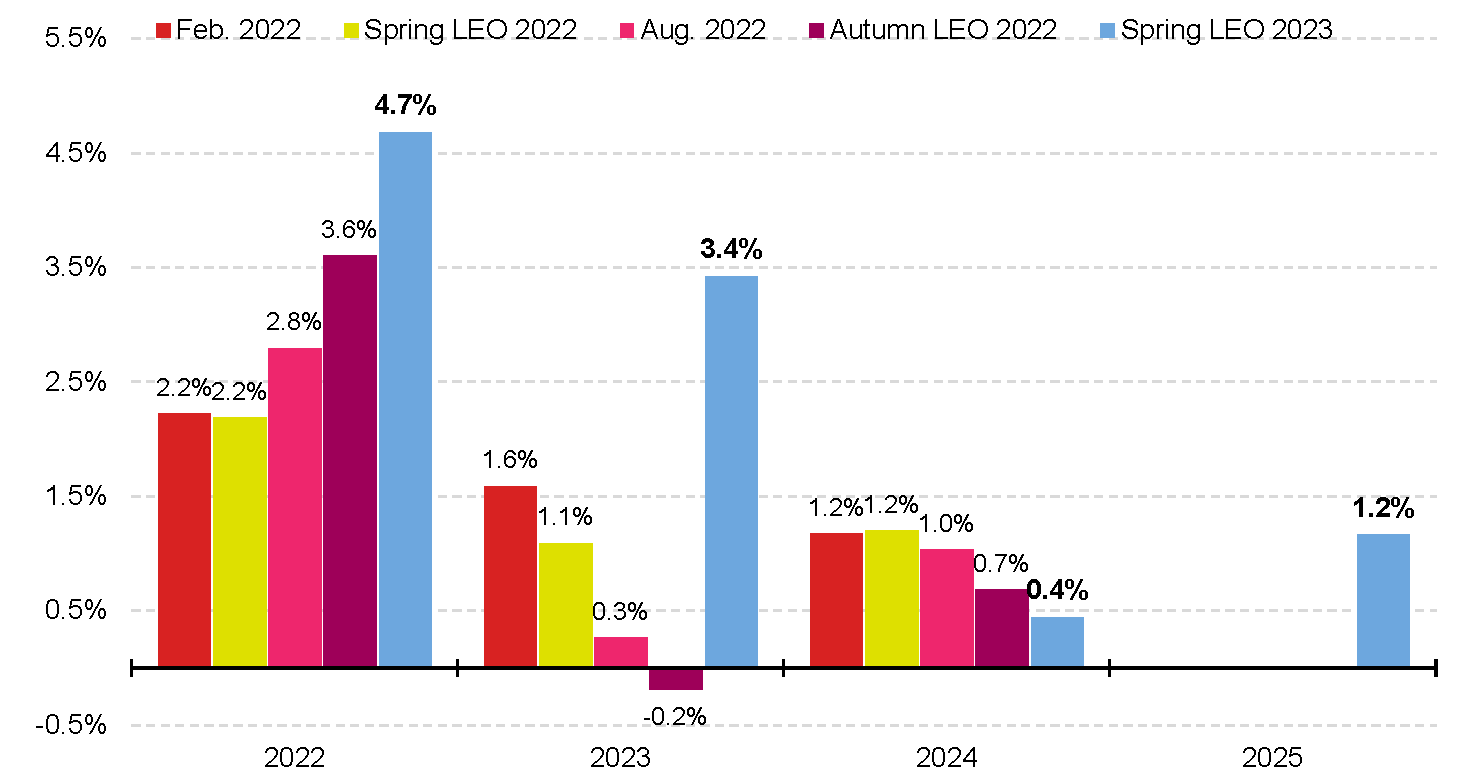

Figure 1.4: Development of reference scenarios for London annual real GVA growth rates 2022-2024

Source: GLA Economics

Figure 1.5: Development of reference scenarios for London annual jobs growth rates 2022-2024

Source: GLA Economics

[1] The forecast is based on judgements and a recently updated econometric model built by GLA Economics. For more details see ‘The new GLA Economics forecast models for London’s economy, GLAE Working Paper n°98, June 2020’.

[2] Unless stated otherwise, any reference to jobs in the main text refers to total workforce jobs.

[3] Historic data for London’s real GVA and workforce jobs are based on ONS actual data, while household spending and household income are based on GLA Economics estimates.

[4] RPI = Retail Price Index. Although not part of the GLA Economics forecast for London. Instead, the consensus forecasts provided by HM Treasury are reported here. See: HM Treasury (2023), ‘Forecasts for the UK economy: a comparison of independent forecasts’, May 2023. Data for 2022 is from the ONS and GLAE estimates, Inflation and price indices – Office for National Statistics.

[5] CPI = Consumer Price Index. Although not part of the GLA Economics forecast for London. Instead, the consensus forecasts provided by HM Treasury are reported here. See: HM Treasury (2023), ‘Forecasts for the UK economy: a comparison of independent forecasts’, May 2023. Data for 2022 is from the ONS and GLAE estimates, Inflation and price indices – Office for National Statistics. Since December 2003, the Bank of England’s symmetrical inflation target is annual CPI inflation at 2%.

[6] GLA Economics (2022), London’s Economic Outlook: Autumn 2022, December 2022

[7] GLA (2023), “GLA cost of living polling”, May 2023. YouGov on behalf of GLA. All figures, unless otherwise stated, are from YouGov Plc. See online for sample sizes and fieldwork dates. The survey was carried out online. Figures have been weighted and are representative of all London adults (aged 18+). ‘Financially struggling’ is a composite category of ‘having to go without basic needs and / or rely on debt to pay for them’ and ‘struggling to make ends meet’.

[8] ONS (2023), “UK House Price Index: March 2023”, May 2023

[9] ONS (2023), “Index of Private Housing Rental Prices, UK: April 2023”, May 2023.

[10] Bakker J et al (2023), Brexit and consumer food prices: May 2023 update, London School of Economics Centre for Economic Performance

[11] London Datastore (2023). ‘Macroeconomic scenarios for London’s economy post COVID-19’.