The State of London’s Economy and Society

On the 17th of June, the GLA’s City Intelligence Unit released the fifth edition of its State of London report[1], a publication that provides the most up-to-date statistics on London’s performance across a range of economic and social outcomes. The report brings together an array of datasets that are organised thematically. The aim is to present some of the most important indicators informing the work of the Mayor, the London Assembly, and stakeholders in London – thereby presenting an updated snapshot of how the capital is performing.

The report sheds light on how London’s people, businesses and localities are addressing current economic and social challenges. Data are also provided on some of London’s longer-term structural challenges as identified and prioritised by the Mayor, including but not limited to environmental sustainability, housing affordability and transport.

This LET supplement provides a high-level summary of the report’s economic findings. Readers are encouraged to read the full report at https://data.london.gov.uk/dataset/state-of-london to access detailed information on London’s current economic as well as social outcomes.

Economy and Labour Market

The ONS recently released annual regional output figures for 2022, along with revised figures from 1998 to 2021. London’s GVA for 2020 and 2021 was revised down by 3.65% and 5.18%, respectively. GLA Economics made corresponding sector-level adjustments to ONS quarterly figures for London and developed a projection for 2023.

The ONS estimates that London’s real GVA grew by 4.8% in 2022, outpacing the UK’s real GDP growth of 4.3%. Among the UK’s regions, London experienced the largest output increase. GLA Economics estimates that London’s GVA increased by 0.7% in 2023 – higher than the UK’s 0.1% GDP increase.

Meanwhile, consumer confidence in London, while volatile since 2020, has generally been higher than it is across the UK. It is also worth noting that Mastercard data shows that London’s retail spending in inflation-adjusted terms grew and peaked in Q4 2023. Subsequently, it slowed during weekdays and weekends. These figures have not yet recovered to late-2023 levels, although weekend spending rebounded more strongly. This would suggest that card spending on retail remained resilient despite the cost-of-living crisis.

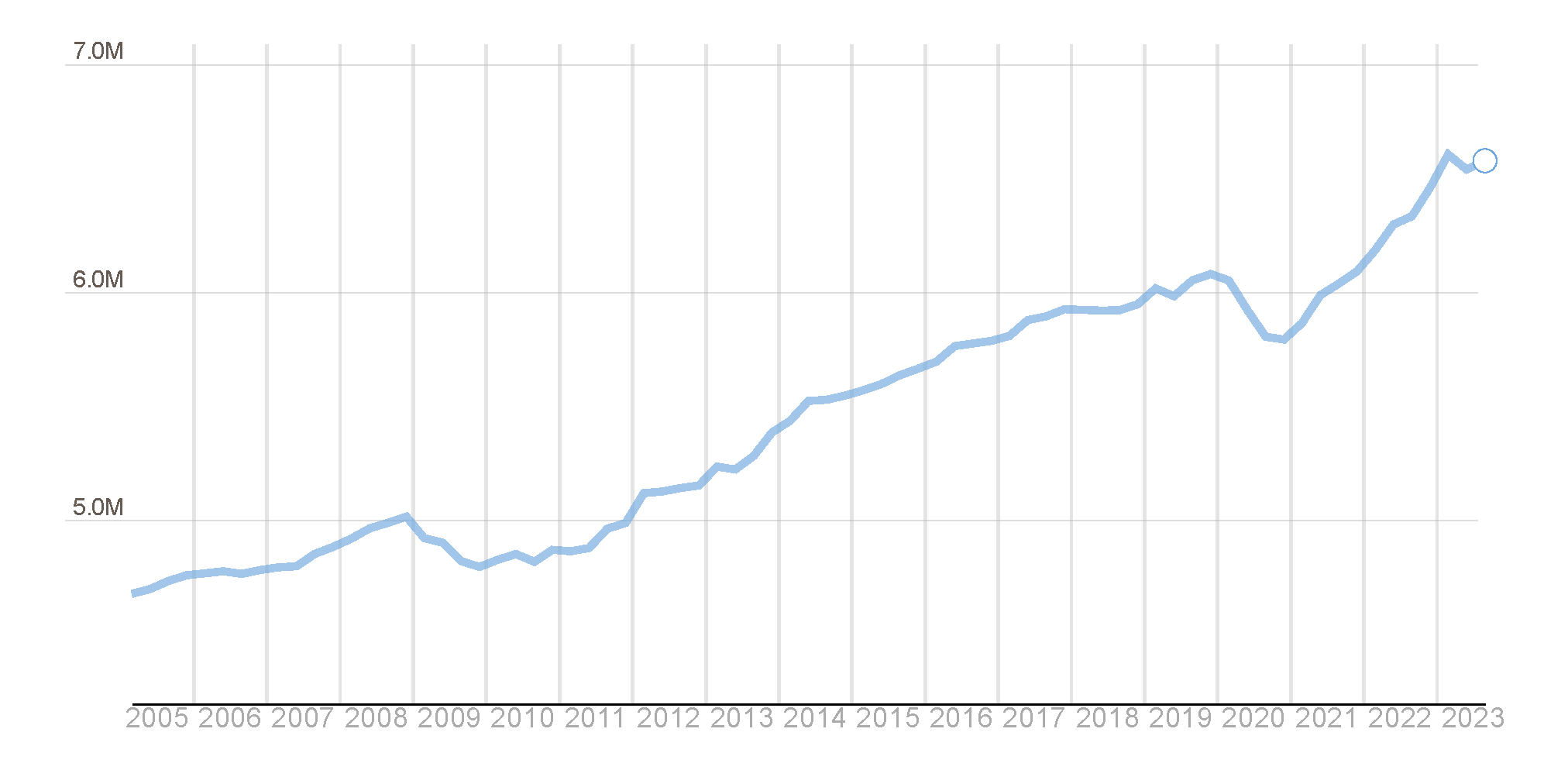

As for jobs and labour-market outcomes, ONS Workforce Jobs data shows that there were approximately 6.58 million workforce jobs in London in September 2023, nearly 500,000 more than in December 2019 and a rise of 8.1% over the period (see Figure A1). London accounted for 44% of the UK’s workforce jobs increase between December 2019 and September 2023.

Figure A1: Total Workforce Jobs

Number of jobs (millions) as of September 2023

Source: ONS Workforce Jobs. Note: Sampling variability (95% confidence interval). This is a workplace-based measure.

For the three months to February 2024, the employment rate in London was estimated at 75.3%, a 1.2 percentage point (pp) increase on the previous quarter and on the same time last year. London’s employment rate was also higher than the UK’s (74.5%).

Moreover, for December 2023 to February 2024, the unemployment rate for London was estimated at 4.4%. It constitutes a decrease of 0.1pp on the previous quarter and 0.6pp from a year earlier. It is slightly higher than the UK unemployment rate (4.2%). It is worth adding that claimant counts were up by 1.9% in the month up to March 2024, by 9.8% on the year, and by 67% from March 2020 (to reach 313,000 claimants).

As for economic inactivity, for the three months to February 2024, the rate of economic inactivity in London was estimated at 21.4%, 1pp down from the previous quarter and 0.6pp down from a year earlier. There were around 1.3 million inactive working-age Londoners, a slight rise from pre-pandemic levels (1.28 million). In the three months to February 2024, the UK rate (22.2%) was higher than London’s. Although London’s inactivity rate reached a ten-year high in mid-2023, it has since returned to pre-pandemic levels.

Income, poverty and destitution

The latest data on income and poverty shows that income inequality within London remains stark, with the top decile of Londoners having 9 times the income (after housing costs) of those in the bottom decile.

In addition, the reduction in number of Universal Credit claimants in London seen to mid-2022, from the height of the pandemic, has reversed, climbing back to over one million in April 2024, and is 11% higher than the same month a year prior. It is now also higher than it was at the highest peak during the pandemic. Within this, there were rising numbers of claimants out of work and searching for work, while there has been an uptick for those seeking additional work. The number of claimants not expected to work accounts for the majority of the increase since mid-2022 (82%), which likely reflects changes in the welfare system (as Universal Credit replaces previous benefits), rather than solely being due to a real increase in numbers.

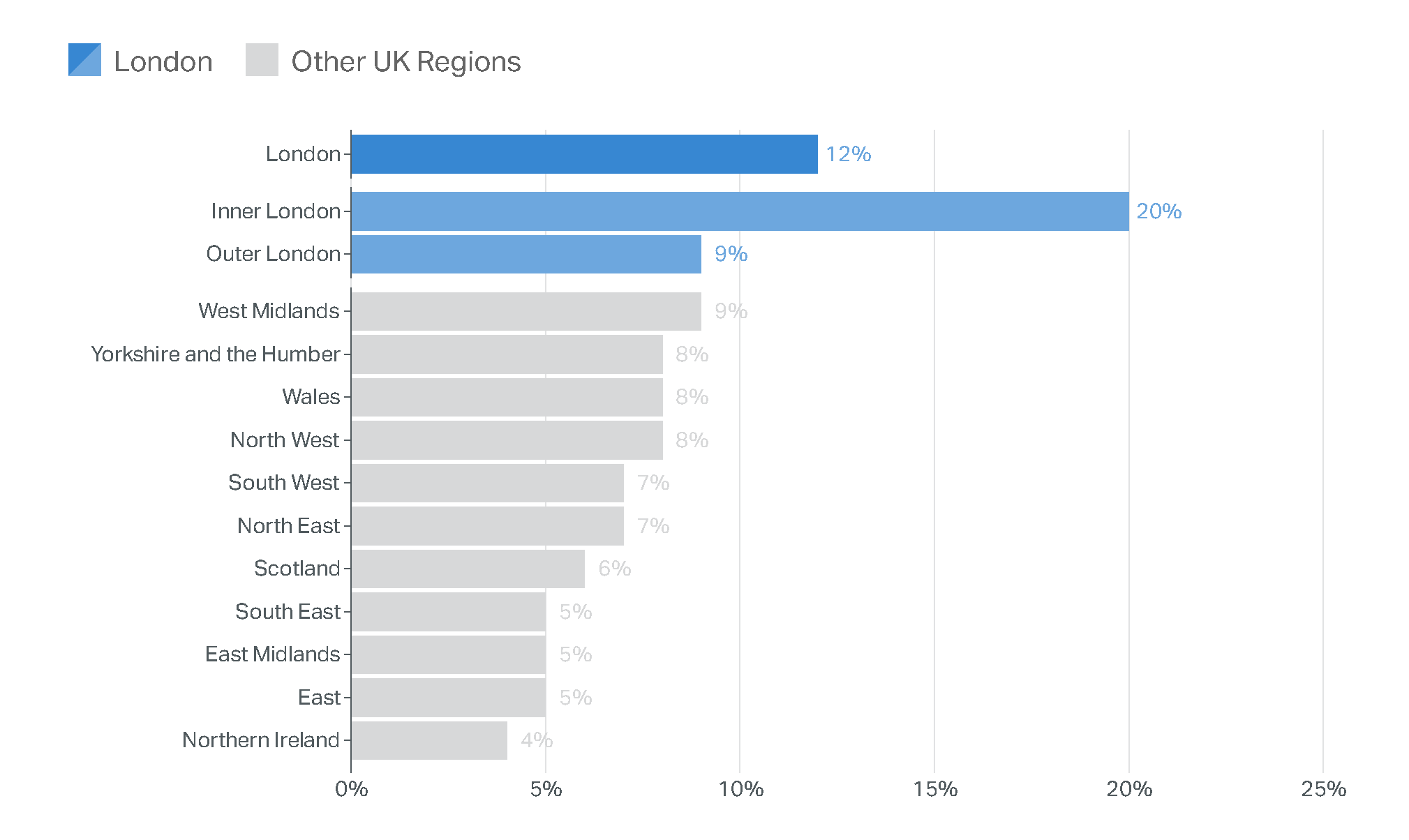

Material deprivation is consistently more prevalent among London’s pensioners than elsewhere in the UK (see Figure A2), while the proportion of London’s children living in poverty remains higher than elsewhere in the UK, despite the latest estimates showing a further drop to 32% in London and decreases in many other regions. The child poverty rate also decreased in Inner London, but at 37% remains relatively high.

Figure A2: Percentage of pensioners with material deprivation by UK region

(2020/21-2022/23)

Source: DWP Households Below Average Income 2020/21-2022/23

Graphic: GLA City Intelligence

Final considerations

The above sections only presented London’s latest economic outcomes as outlined in the report. More broadly, the report finds that London can point to several areas of success and resurgence since the onset of COVID-19: the city remains the UK’s most economically-productive region and its principal jobs creator. Meanwhile, it outperforms the rest of the country on several important social measures, including healthy life expectancy at birth, feeling of communal belonging, and progress towards reducing air pollution.

Nevertheless, the pandemic highlighted acute pre-existing challenges and problems that London has and continues to suffer from. Chief amongst these are the following:

- London remains more vulnerable to the cost-of-living crisis than other regions. While London’s macroeconomic performance remains solid and inflation rates in the capital have dropped (as they have nationally), the city’s economic success comes with a price. Prices for necessities continue to be much higher in London than elsewhere in the UK. With housing costs taking up a much bigger share of household income in London than elsewhere and core inflation persisting more in the UK than in comparable countries, Londoners are likely to feel the financial pressure more substantially. This would suggest that many of London’s affordability crises – from housing to food and necessities – may persist for longer than initially thought. This would have implications for the subsequent point.

- London’s economic and social inequalities remain starker than they are elsewhere in the UK. Income inequality remains pronounced in the city, and poverty rates (whether relative or persistent) are still high – something that the aforementioned cost-of-living crisis is likely to aggravate. This has had ramifications on educational attainment (whether for children or adults), health and wellbeing outcomes, access to transportation and infrastructure, and even feelings of community trust and welfare differ significantly across financial, ethnic and other strata. Londoners with protected demographic and economic characteristics still do not enjoy as much of the city’s economic success, while suffering disproportionately from its adverse realities. Further growth in such inequalities could risk neutralising the very attributes on which London’s success is constructed.

- London’s short-to-medium term future is still precarious. History shows that in times of affordability pressures, it is the most disadvantaged in society who will unfortunately bear a disproportionate burden. At a time when around half of Londoners report concerns about affording their housing and the bottom decile’s income after housing costs is nearly nine times lower than the top decile’s, this would signal a negative development, especially when more research is demonstrating the adverse ramifications of inequality on economic growth, individual wellbeing and societal prosperity.

Therefore, there is some way to go not only to address the key problems the city faces, but to ensure that such problems do not worsen and do not undermine the very strength that London can still enjoy.

[1] GLA Economics (2024). ‘State of London: Version 5’, June 2024.