London's Economy Today editorial - September 2025

UK sees no growth in July

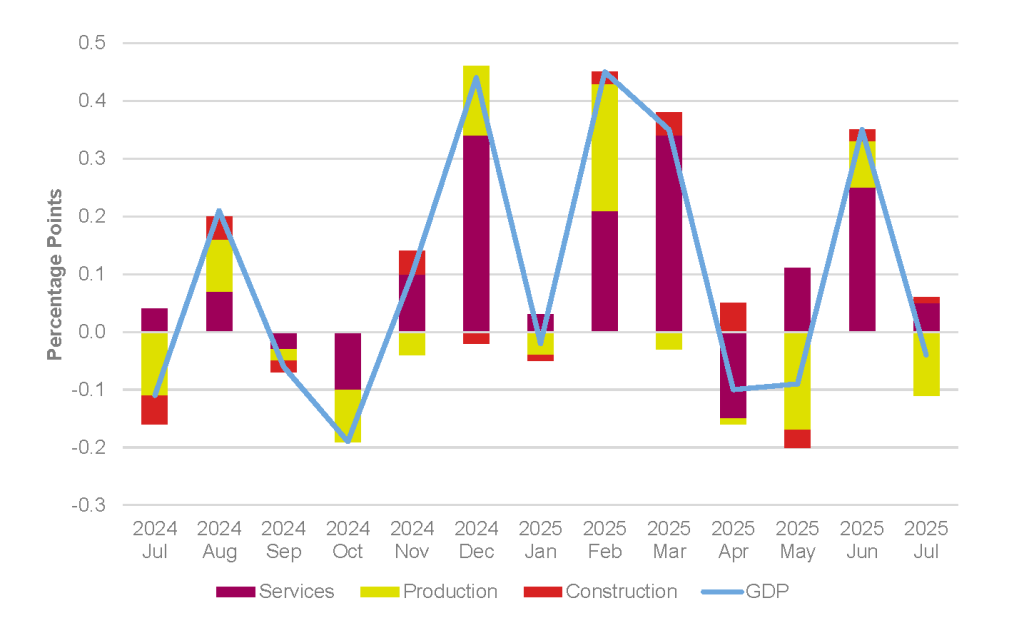

Data published this month by the Office for National Statistics (ONS) showed that the UK economy didn’t grow in July (Figure 1). This followed growth of 0.4% in June although this lack of growth was what had been expected by surveyed economists.

Figure 1: Contributions to monthly UK GDP growth, July 2024 to July 2025

Source: GDP monthly estimate from the ONS

Looking at the main components of GDP, services and construction saw growth in July with their outputs increasing by 0.1% and 0.2% respectively. However, output in the production sector fell by 0.9% in July. Looking at a slightly longer time period the ONS noted that “real gross domestic product (GDP) grew by 0.2% in the three months to July 2025 compared with the three months to April 2025, down from three-month-on-three-month growths of 0.3% in June 2025 and 0.6% in May 2025”. The services sector, an important sector for London’s economy, was the main driver of growth over the three months.

UK inflation holds steady in August

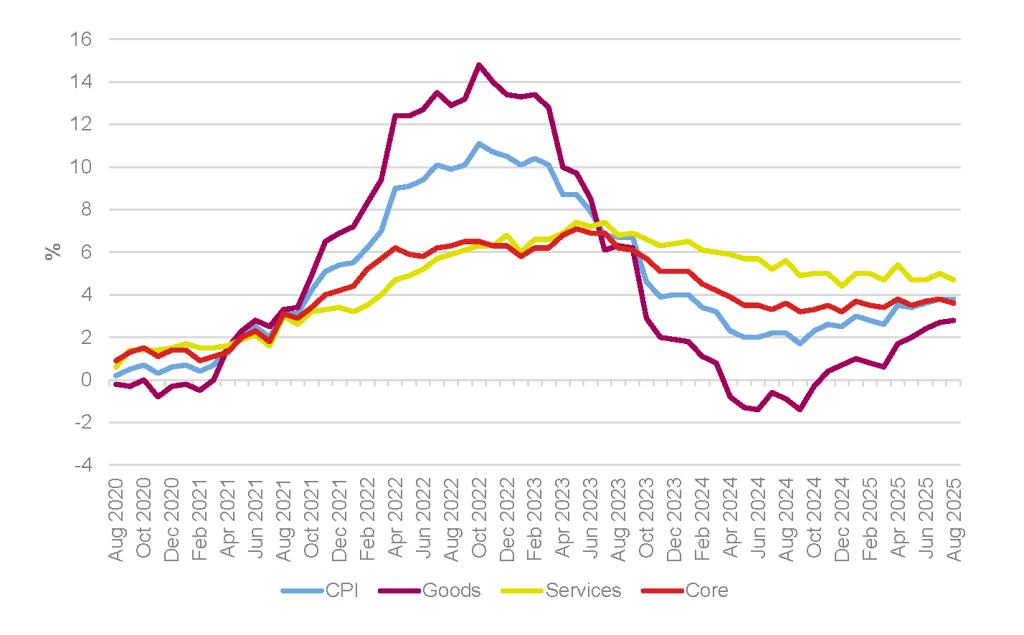

The ONS has also published data on August’s Consumer Price Index (CPI) inflation this month. This showed that CPI inflation remained steady at 3.8% in the 12 months to August 2025, unchanged on the 12 months to July (Figure 2). This was in line with what surveyed economists had expected, but UK inflation continues to remain significantly above the Bank of England’s central symmetrical target of 2% ±1%. The ONS noted that “the UK’s CPI inflation rate of 3.8% was significantly higher than the first (or “flash”) estimate of inflation for France (0.8%) and Germany (2.1%) in August 2025. The UK rate has been above that of the other two countries in each month of 2025 to date.”.

Figure 2: CPI, goods, services and core annual inflation rates, UK, August 2020 to August 2025

Source: ONS, GLA Economics

Looking at the data in more detail the ONS observed that “air fares made the largest downward contribution to the monthly change in [the CPI annual rate] …; restaurants and hotels, and motor fuels made large, partially offsetting, upward contributions”. Beyond the headline inflation figure other inflation measures also remain elevated. Core CPI (excluding volatile energy, food, alcohol and tobacco prices) inflation slowed to 3.6% over the year to August 2025, down from 3.8% in July. The CPI goods annual rate rose to 2.8% up from 2.7%. The CPI services annual rate slowed from 5.0% in July to 4.7% in August.

UK government borrowing costs rise

UK long-term government borrowing costs hit their highest level since 1998 early this month, although have since dropped back a bit. Developed economy bond yields have risen for a number of countries recently driven in part due to geopolitical tensions and the impact of US trade policy. However, UK medium- and long-term costs are the highest in the G7 in part due to higher inflation and interest rates, although other factors such as a decline in demand from defined benefit pension funds has also had an impact.

These higher borrowing costs are likely to reduce the Chancellor’s room for manoeuvre in the Autumn Budget on 26 November. It also came as there were reports that the Office for Budget Responsibility (OBR) would down grade their productivity forecast at the Budget. The Financial Times reported that this downgrade “could create an additional £9bn or more shortfall in public finances”. This additional shortfall is based on an assumption that the OBR reduces its productivity growth forecast by 0.1 percentage points (pp) from its current forecast rate of 1.1% per year on average over the medium term. If the OBR were to reduce its forecast by 0.2pp this would lead to an £18billion shortfall everything else remaining constant.

UK study visa applications decline

Home Office data published this month showed that study visa applications stood at 120,100 in August this year a decrease of 1.5% on the same month last year and down 18% on 2023. The summer sees a lot of study visa applications with about a third of total annual applications happening in the month. This decline came at the same time that stricter rules on study visa applications have come into effect. Institutions now have to make sure that less than 5% of student visa applications are rejected rather than the 10% threshold previously set. Nevertheless, study visa applications were 1% higher in the three months to August this year compared to the same period last year, although they are 17% below their summer 2023 peak. Fees from international students have recently been used by UK universities to meet increasing funding pressures and the decline in foreign student numbers is likely to put further pressure on the university sector.

London’s labour market continues to show some loosening

The ONS also published data this month looking at the recent performance of London’s labour market which showed signs of loosening continuing to build, though not sharply. For the quarter up to June 2025 the total number of workforce jobs in London was estimated at 6.5 million, down 40,600 jobs on the quarter but up 16,200 on the year. Employee jobs rose by 9,790 on the quarter but self-employed jobs fell by 39,500, with government trainees and HM Forces accounting for the balance. On the year, employee jobs rose by 67,400 and self-employment jobs fell by 46,100. Looking more recently, the count of payrolled employees from HMRC’s Pay As You Earn (PAYE) RTI dataset offers a timely measure of labour market trends. Early estimates of this indicate that there were around 4.4 million payrolled employees living in London in August 2025, a fall of 3,810 from July. The latest London estimate represents a decrease of 35,300 (0.8%) on the previous year (August 2024) compared to a decrease of 0.4% UK-wide. Compared to the pre-pandemic (February 2020) level, the number of payrolled employees in London was up by 218,000 or 5.3%. This compares to an increase of 4.3% across the UK.

Government gives go-ahead for second runway at Gatwick

The Government has given its approval for a £2.2 billion plan for a second runway at Gatwick airport. It is hoped that this new facility will be completed by the end of the decade. The project was given approval after the airport agreed to plans on noise abatement and the use of public transport by passengers to reach the airport. Other conditions on the second airport runway include helping affected households by providing triple glazing or covering moving costs. The airport estimates that once complete passenger numbers could rise to 80 million compared to the 46.5 million record set in 2019.

GLA Economics will continue to monitor these (and other) aspects of London’s economy over the coming months in our analysis and publications, which can be found on our publications page and on the London Datastore.