London's Economy Today editorial - October 2025

UK inflation remains steady in September

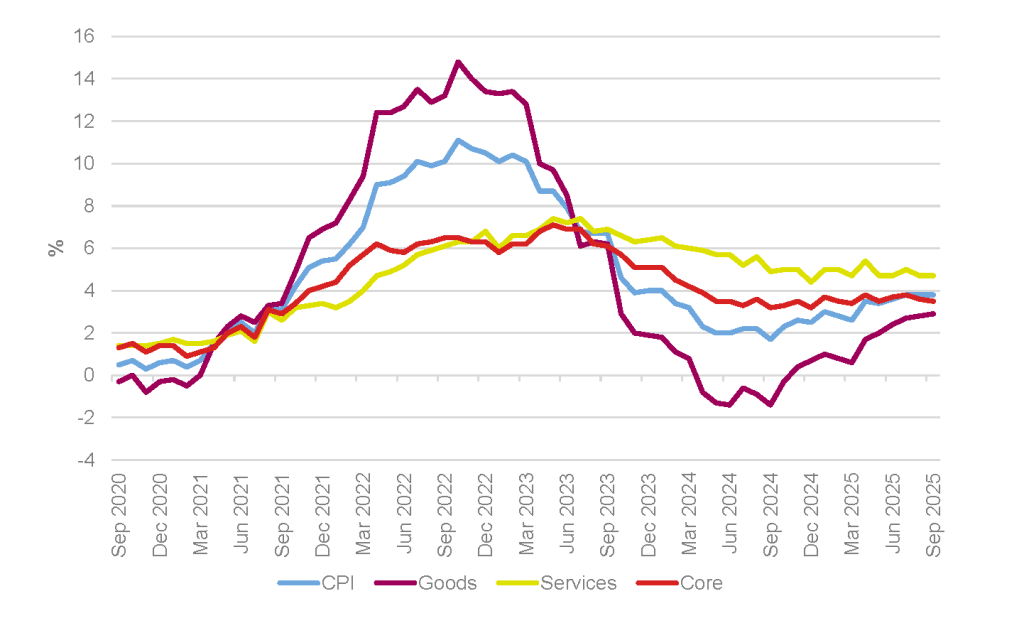

The Office for National Statistics (ONS) published data on September’s Consumer Price Index (CPI) inflation this month. This showed that CPI inflation remained unchanged at 3.8% in the 12 months to September 2025; it has remained at this level since July (Figure 1). This was lower than anticipated by most surveyed economists who had expected it to rise to 4%. Inflation however continues to remain significantly above the Bank of England’s central symmetrical target of 2% ±1%.

Figure 1: CPI, goods, services and core annual inflation rates, UK, September 2020 to September 2025

Source: ONS, GLA Economics

The September CPI numbers are of particular importance as these are typically used for the raising of a number of benefits in the following financial year. Looking at the data in more detail the ONS observed that “transport made the largest upward contribution to the monthly change [in the annual rate]; recreation and culture, and food and non-alcoholic beverages made the largest offsetting downward contributions”. UK inflation remains above that seen in other countries with the ONS noting that “the UK’s CPI inflation rate of 3.8% was higher than the inflation rates for Germany (2.4%), France (1.1%) and the EU (2.6%), in September 2025. The last time the UK rate was lower than the EU rate was December 2024”.

Beyond the headline inflation figure other inflation measures generally remained steady. Core CPI (excluding volatile energy, food, alcohol and tobacco prices) inflation slowed slightly to 3.5% over the year to September 2025, down from 3.6% in August. The CPI goods annual rate rose to 2.9%, up from 2.8%. While the CPI services annual rate remained unchanged at 4.7%.

UK GDP sees slight monthly growth in August

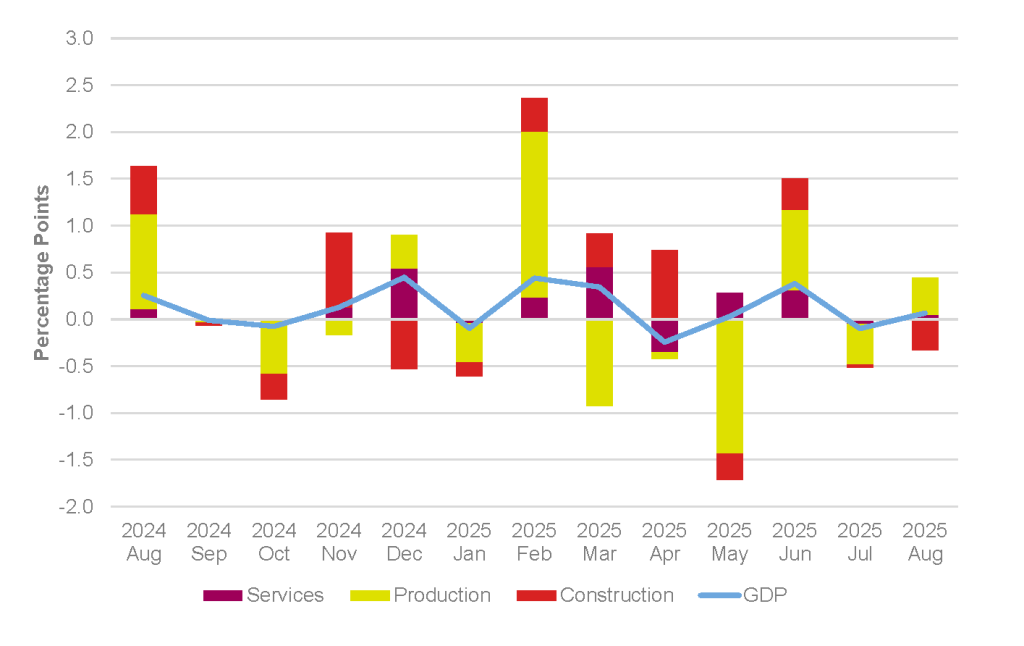

The latest monthly UK GDP data from the ONS showed that the UK economy grew by 0.1% in August (Figure 2). This followed a revised down contraction of 0.1% in July and was in line with the expectations of polled economists.

Figure 2: Contributions to monthly UK GDP growth, Aug 2024 to Aug 2025

Source: GDP monthly estimate from the ONS

Looking at the main components of GDP only production saw growth in August with its output increasing by 0.4%. Output in the services sector saw no growth in August while output in construction fell by 0.3%. Still, looking at a slightly longer time period the ONS notes that “real gross domestic product (GDP) is estimated to have grown by 0.3% in the three months to August 2025, compared with the three months to May 2025”.

Fiscal speculation as budget nears

As the Chancellor of the Exchequer, Rachel Reeves, prepares next month’s Autumn budget, she is faced with plugging an expected shortfall in public finances – largely a result of higher-than-expected borrowing costs and slow economic growth. There is much speculation over how she could close this gap, with credible chatter suggesting that the Treasury is considering (1) a targeted wealth tax, (2) reforms to capital gains tax, (3) levies on quantitative easing, and/or (4) bank surcharge increases.

Any new wealth tax would disproportionately affect London’s economy, given a quarter of UK household wealth (about £2.5 trillion) is concentrated in the capital. Proponents argue a wealth tax could potentially raise £10bn annually from property and financial assets, capturing “unearned” gains largely accrued by the wealthiest. However, past experience (and orthodox economic theory) point to risks of capital flight, lower business investment, and reduced economic growth.

Some of the other potential revenue options under consideration (listed above) would also land on London’s property and banking sectors. With nearly a third of all UK Capital Gains Tax liabilities generated in London, changes would affect buy-to-let markets and high-value residential sales in the capital. Beyond property, reforms would also impact London’s financial services sector, affecting how private equity managers are paid, the stock options tech workers receive, the sale prices of small businesses etc. A levy on quantitative easing could provide £5–8 billion in annual revenues. Increased taxes on the financial sector could generate £1.5–2 billion yearly (through higher banking surcharges, increased corporation tax rates, or additional Stamp Duty on premium London assets) – but all of these measures would inevitably alter investment and lending behaviour.

IMF projects UK growth improvement, but fiscal and financial pressures remain high

The IMF’s October 2025 World Economic Outlook delivered mixed news for the UK and London. The report revised projected UK GDP growth upwards to 1.3% in 2025 and 2026, to reflect stronger-than-expected growth in the first half of the year. However, the IMF also caution that living standards will remain flat, as households face ongoing cost-of-living pressures (particularly from utility costs). Trade frictions could shave 0.1–0.3 percentage points off UK GDP, with London’s open, finance-driven economy particularly exposed to such external shocks. Inflation is also forecast to remain elevated at 3.4% in 2025, well above the G7 average (2.7%) and the Bank of England’s 2% target. These elevated rates, coupled with April’s employer-side national insurance hike, are expected to constrain growth through persistently high UK borrowing costs.

Globally, the IMF forecasts subdued but steady growth. World output growth is projected at 3.2% in 2025 and 3.1% in 2026. Advanced economies will grow around 1.6% in both years, and emerging markets and developing economies are expected to grow by 4.2% and 4.0% respectively. Fiscal pressures are also forecast to persist, with the IMF Fiscal Monitor forecasting public debt in advanced economies to on average exceed 100% of their GDP by 2029. For the UK, the report highlights the limited flexibility in the UK’s fiscal headroom – a result of relatively large public sector wage bills (“current spending”) and lower discretionary capital spending. Central government current expenditure is currently £557.2 billion (September 2025), up 9.3% on the year. In contrast, net public investment (capital expenditure) fell to £44 billion, down nearly £12 billion from a year earlier and representing less than 8% of current total government outlays.

The IMF echoes the usual sentiment: rebalance spending toward productive public investment and encourage it through streamlined review and procurement processes. Overall, the IMF portrays a UK economy that is constrained, with recent stronger-than-expected performance offset by structural fiscal pressures.

SME financing under pressure

Recent trends in Small and Medium sized Enterprise (SME) financing point to rising financial strain for smaller firms. Roughly a quarter of UK SMEs now reports insufficient revenues or savings, up from 18% in 2023. Survey data highlight particular vulnerability among sole traders and businesses under 50 employees, many of whom state they are delaying borrowing amid policy uncertainty and high input costs. Over 30% cite energy and wage bills as their biggest external pressures, while taxation remains the main obstacle for roughly 60% of SMEs with employees.

Although gross SME lending (i.e., the total value of supplied credit) has seen a modest uptick, volumes (the number of new loan agreements) remain below pre-pandemic levels. Notably, only about 10% of firms plan to apply for new finance, with another 15% considered “future seekers” – those held back by the tough trading environment. London’s SME base is especially sensitive, because so many SMEs operate in lower-margin service, creative, and consumer-facing sectors. These businesses tend to have less pricing power, fewer tangible assets to secure borrowing, and are more exposed to swings in customer demand and input costs.

London consumer confidence remains high

Consumer confidence in London, as measured by the GfK index of consumer confidence, has shown strength in recent months. Thus, it hit a high not seen in two decades in August and although it has slightly moderated since then remains elevated compared to historic averages. This compares sharply with the UK as a whole which has not seen positive measures of consumer confidence since 2016.

Business confidence in the capital also seems to be holding up according to the Q3 2025 London Quarterly Economic Survey for the London Chamber of Commerce and Industry by Savanta. This polled over 500 business leaders in the capital and found that “business confidence among London firms slightly eased in Q3, although overall sentiment remains positive”. While in terms of the economic outlook “London businesses remain more optimistic about the capital’s prospects than the UK as a whole, signalling a recovery from the earlier decline in confidence. The proportion of firms expecting an improvement in their own outlook remained steady at 37%, in line with previous quarters”.

GLA Economics will continue to monitor all these and other aspects of London’s economy over the coming months in our analysis and publications, which can be found on our publications page and on the London Datastore.