London's Economy Today editorial - November 2025

Chancellor announces significant revenue raising measures in the Budget

The Chancellor’s Autumn Budget introduces £26 billion in tax rises by 2029-30, to fund £11 billion in spending increases and cut borrowing from 4.5% to 1.9% of GDP over the forecast period. Spending commitments include removing the two-child benefit limit (costing £3 billion and lifting 450,000 children out of poverty) – which is particularly important for London, where 70,000 households are subject to the two-child limit (the most of all UK regions).

In its accompanying Economic and Fiscal Outlook, the Office for Budget Responsibility (OBR) forecasts that Budget measures will reduce inflation by 0.4 percentage points next year (the largest single-Budget reduction outside of a crisis), while raising the tax burden to an all-time high of 38% of GDP by 2030-31. They forecast government borrowing falling from 4.5% to 1.9 % of GDP over the forecast period and the Chancellor meeting her fiscal rules with £22 billion headroom (double the headroom figure earlier this year).

Freezes to personal tax thresholds will create 780,000 more basic-rate taxpayers, 920,000 higher-rate taxpayers, and 4,000 additional-rate taxpayers in the UK by 2029-30. With London contributing 27% of UK income tax revenues from 14% of the population, the capital’s higher-than-average salaries mean more workers will be pushed into higher tax brackets through threshold freezes compared to other regions. Other revenue-generating measures include National Insurance on salary-sacrificed pensions above £2,000 (forecast to raise £4.7 billion) and council tax surcharges on properties valued at more than £2 million, of which 70% are located in London.

The Chancellor also announced an extension of the fuel duty freeze until September 2026 (costing £2.4 billion), EV mileage charges from April 2028 (3p per mile, raising £1.4 billion), rail fare freezes, and funding for the DLR Thamesmead extension. For London, the fuel duty freeze has less of an impact compared to the rest of the UK – with only 56% of households owning cars, compared to 80% across England. The EV charge will affect London’s 193,000 registered electric vehicles, forecast to rise to roughly 1.1-1.4 million by 2030. With almost half of London’s workers commuting to work by public transport compared to 12% nationally, the fare freeze provides significant relief.

The Government also set London’s Integrated Settlement allocations for 2026/27-2028/29, continuing the £337 million annual Adult Skills Fund, providing £46 million yearly for Connect to Work, and increasing the National Housing Development Fund to £120 million by 2029/30.

The Autumn Budget’s combination of record tax rises and increased public spending marks a clear break from the previous decade. We’ll examine the London-specific impacts in further detail in next month’s London’s Economy Today.

UK’s GDP sees slight growth in August

Usually in London’s Economy Today, we lead by reporting on monthly GDP figures, as monthly data provides the latest snapshot of economic activity. This month, however, we’ll focus on newly released (and less volatile) three-month GDP figures, for a clearer understanding of underlying growth trends.

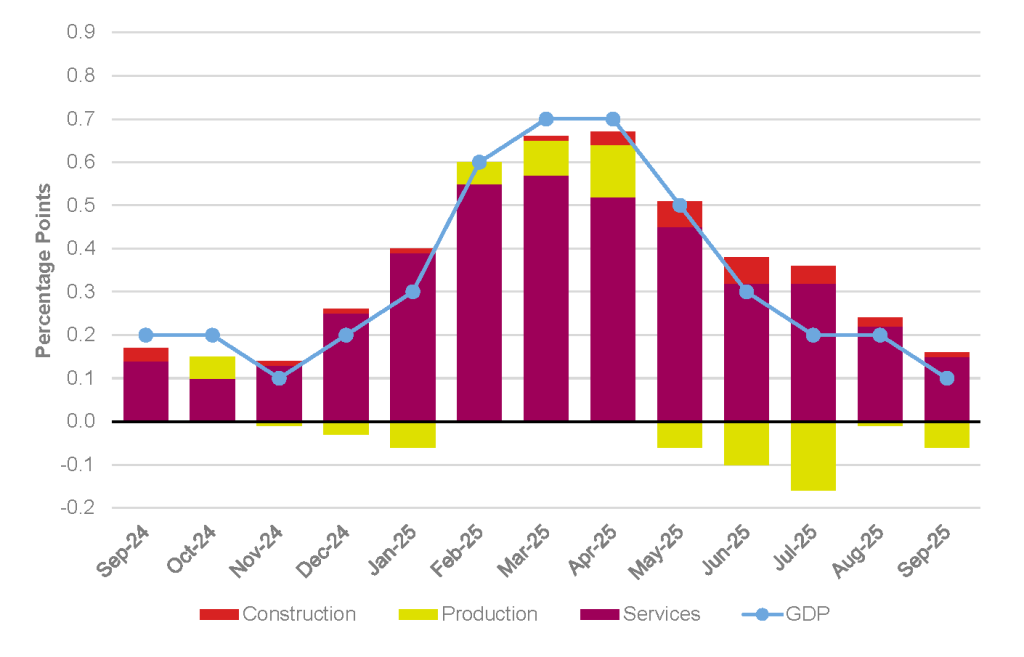

The UK economy grew by 0.1% in the three months to September 2025, a slight fall from the growth rate of 0.2% seen in August (revised down from 0.3%), and significantly below the 0.7% growth seen earlier this year. The service sector, an important sector of London’s economy, remained the driver of GDP growth, contributing 0.15 percentage points to growth, while the production sector contracted and construction grew marginally. This extends the UK’s reliance on services for growth, with production and construction contributing little to overall growth for over a year.

Figure 1: Contributions to three-month UK GDP growth, Sep 2024 to Sep 2025

Source: ONS, Contributions to three-month GDP growth, UK

Note: Sum of component contributions may not sum to total growth due to ONS rounding.

Monetary policy holds steady as risks become more balanced

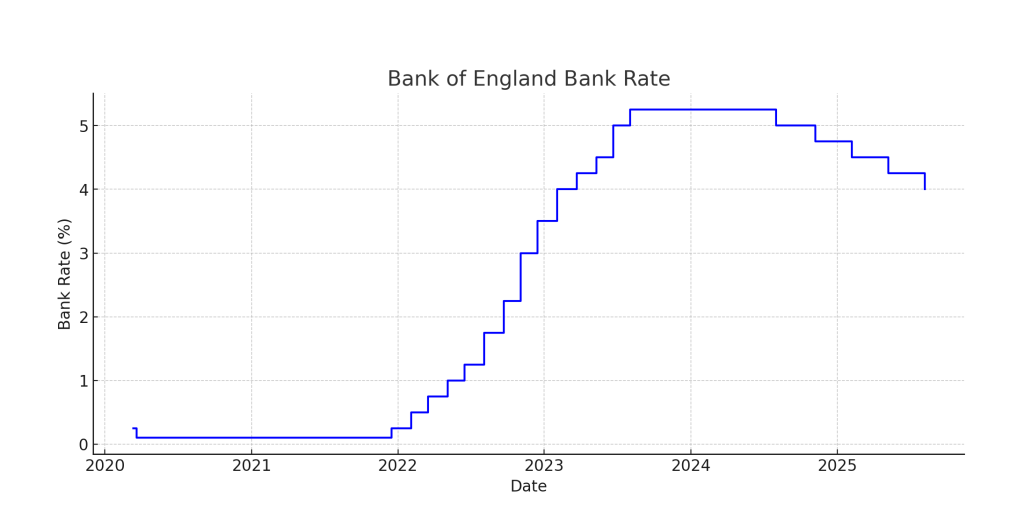

At its November meeting, the Bank of England’s Monetary Policy Committee (MPC) voted by a narrow majority to maintain interest rates at 4% (Figure 2), with four members preferring a reduction to 3.75%. The decision reflects the Committee’s wish to see firmer evidence that Consumer Price Index (CPI) inflation is returning sustainably to the Bank’s target of 2%±1%. Interest rates have moved off their peak but remain restrictive, indicating a gradual shift toward easing while maintaining vigilance against renewed price pressures.

Figure 2: Bank of England’s Bank Rate

Source: Bank of England

Inflation is judged to have peaked, with CPI easing to 3.6% in October down from 3.8% in September in line with the Bank’s projection that it will fall close to 3% early next year. Wage growth and services price inflation have continued to moderate, and firms’ cost pass-through appears to be diminishing. However, the MPC stresses that underlying pressures must ease further before rates can be reduced again, particularly as inflation expectations remain elevated and services inflation remains above historical norms.

Risks around the inflation outlook have become more balanced, but the degree of slack in the economy remains difficult to measure. The Bank notes that model-based estimates vary widely: indicators linked to recent price behaviour point to residual demand pressure, while labour market and capacity-utilisation measures suggest emerging excess supply. This uncertainty is compounded by risks to labour force participation and the possibility that the natural rate of unemployment has risen following recent shocks. If slack proves smaller than assumed, inflation could be more persistent; if demand weakens more sharply, inflation may fall below target.

International conditions add further uncertainty. Global growth remains steady but subdued, while higher US tariffs, volatile energy prices and shifting financial conditions continue to influence the UK outlook. Rising global bond yields and elevated market volatility increase the possibility that external shocks could transmit through gilt markets and financial institutions. Against this backdrop, the Bank judges that holding the Bank Rate at its current level is appropriate while it evaluates incoming data. The MPC will reassess the balance of risks and the inflation outlook at its December meeting.

Brexit impact worse than previously forecast

A new paper was published this month looking at the economic impact of Brexit on the UK economy. In it the authors estimate that the UK leaving the EU “reduced UK GDP by 6% to 8%, with the impact accumulating gradually over time”. They further estimated a 12-18% reduction in investment compared to staying in the EU and a 3-4% reduction in both employment and productivity. This they note “reflect a combination of elevated uncertainty, reduced demand, diverted management time, and increased misallocation of resources from a protracted Brexit process”. While in terms of the accuracy of forecasts at the time of the 2016 referendum they observe that “that these forecasts were accurate over a 5-year horizon, but they underestimated the impact over a decade”.

New ONS data highlights London’s sustained housing market divergence from the UK

London’s housing market continues to break from the national trend, with ONS data showing average non-seasonally adjusted prices in the capital falling by 1.8% over the past year, while UK prices rose by 2.6%. This makes London the only English region to see annual house price declines, in sharp contrast to growth in Yorkshire and the Humber (+4.5%) and the Northeast (+3.9%). Meanwhile, annual rental price growth in London has slowed to 4.3%. Although rents remain the highest of any nationally, London is no longer leading UK regional rental price growth, which is now strongest in the Northeast and Yorkshire and the Humber.

This lull in price growth is likely demand related. Although mortgage rates have fallen (following five Bank of England rate cuts) and thus eased mortgage affordability pressures – house price-to-income ratios in London sit at 11.1, well above the England average of 7.7. So, despite falling borrowing costs, prices have continued to decline as households struggle to afford entry to the market. However, as real incomes eventually rise, interest rates drop further, or lending criteria are loosened, demand will inevitably rebound – returning London to a familiar cycle of rising housing costs. Oxford Economics forecasts that London house prices will reach their lowest point this year (around 9% below 2022’s peak) before gradually recovering. Lasting changes to affordability will only be achieved by expanding housing delivery and addressing structural supply barriers.

Unemployment in London has risen

The latest labour market data from the ONS showed a weakening of conditions in London and across the UK. Unemployment in London, which had seemed to have peaked early in 2025, rose to its highest level in a decade excluding the pandemic. Most other regions of the UK also saw fast-rising unemployment and declines in payrolled employees. In the three months to September 2025 London’s unemployment rate was estimated at 6.5%, an increase on the quarter and an increase of 0.6 percentage points (pp) from a year earlier. The more timely estimate of payrolled employees (which is subject to revision) showed a decrease of 14,400 (-0.3pp) in the number of payrolled employees in London between September and October 2025, and a decrease of 1.1% on the year.

Heathrow third runway plan

Elsewhere the Government announced on 25 November that it had chosen Heathrow Airport’s plan for a 3.5km long runway which will require moving part of the M25 motorway. This was in preference to another plan put forward by the Arora Group which would not have required moving the M25. The Department for Transport said Heathrow’s plan had the “greatest likelihood” of getting planning approval in this parliament.

GLA Economics will continue to monitor these (and other) aspects of London’s economy over the coming months in our analysis and publications, which can be found on our publications page and on the London Datastore.