London's Economy Today editorial - March 2026

Conflict in the Middle East triggers global commodities shock amid fears for the cost of living

The US and Israel began attacks on Iran on 28 February. Iran has responded by attacking several countries around the Persian Gulf and elsewhere and declaring the Strait of Hormuz closed to most shipping. The Strait usually has around 20% of the world’s oil exports pass through it. Its closing has been called the “the largest supply disruption in history” by the International Energy Agency (IEA).

Putting the impact of the conflict into context, the IEA has said that it has caused “a larger loss of oil supply than in the oil crises of the 1970s and a larger loss of natural gas supply than during the 2022 energy crisis linked to Russia’s invasion of Ukraine”. Other commodities have been impacted as well with exports of nitrogen fertilizers (made from ammonia using natural gas), urea and sulphur (which are used amongst other things in the production of semiconductors and phosphate fertilizers) also being heavily hit. International air travel has seen severe disruptions. The economies of the Gulf states and some Asian nations that are heavily dependent on Gulf energy exports have also been negatively impacted by the conflict.

In response to this war Brent Crude oil prices have risen from just under $80 a barrel before the conflict to over $110 a barrel as the conflict progressed, although it has since fallen back a bit. Gas prices have also been rising following Israel’s attack on Iran’s South Pars gas field and Iran’s attacks on oil and gas facilities in the region. This has seen household costs already rise with average petrol prices increasing by over 30p per litre since the start of the conflict according to RAC data. Borrowing rates have also been rising; the cost of a typical 25-year mortgage on £250,000 increased by £788 since the start of the war according to analysis by the financial information service Moneyfacts. UK Government borrowing costs have also heavily fluctuated during the conflict.

The Government has already intervened to provide help to some households with a £53m support package to help “vulnerable” households hit by the rise in heating oil costs. The Chancellor of the Exchequer, Rachel Reeves, has said that “contingency planning is taking place for every eventuality so we can keep costs down for everyone and provide support for those who need it most”. Still, concerns remain about wider household energy bills when the UK energy price cap is renewed in July should the disruption caused by the conflict continue. The energy consultancy Cornwall Insight calculated that a typical annual household energy bill may rise by £322.

Looking at the possible impact on the UK of the war, the National Institute of Economic and Social Research (NIESR) have modelled possible scenarios. They found that “a temporary jump in energy prices would lead to a 0.3pp increase in inflation alongside a negligible impact on GDP for 2026”. However, they further note that “a one-year persistent shock would push inflation up by 0.7pp and dampen output growth by 0.2% in 2026” with this leading to pressure on the Bank of England to raise interest rates “back above 4%”. In a sign that the war has already affected the Bank’s thinking on monetary policy its Monetary Policy Committee declared at its March meeting that it was “ready to act as necessary” to keep inflation on target.

UK inflation remains steady in February

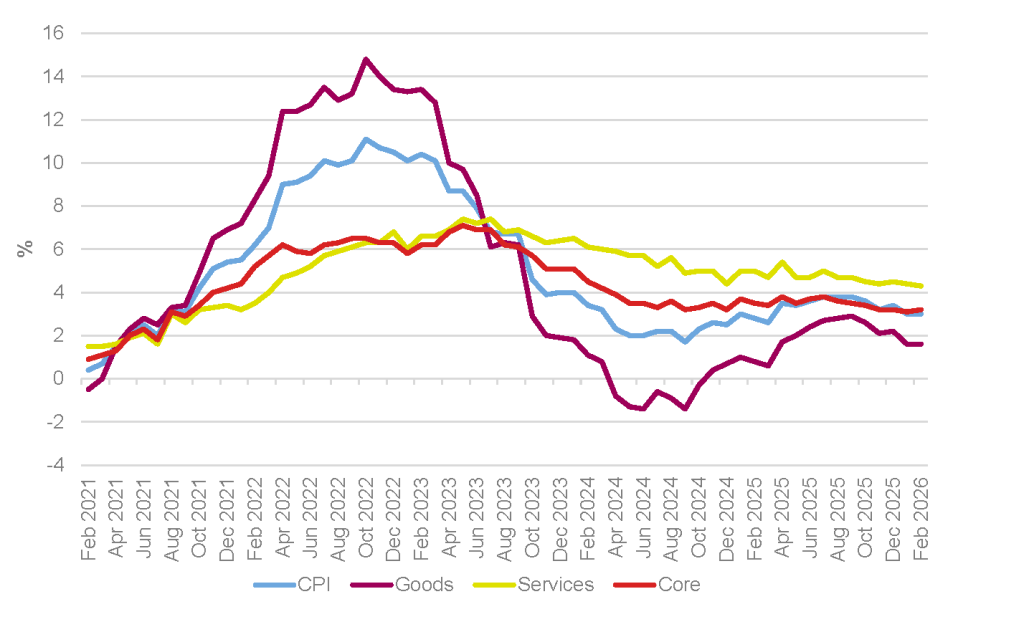

Looking at how prices were behaving just before the conflict started, data published this month by the Office for National Statistics (ONS) showed that Consumer Price Index (CPI) inflation was 3.0% in the 12 months to February 2026, unchanged from the 12 months to January (Figure 1). This was in line with the expectations of most surveyed economists. Inflation remains above the Bank of England’s target of 2% but also remains just within the margin for fluctuation of ±1% around this central symmetrical target. However, the ONS also noted that “the UK’s CPI inflation rate of 3.0% was higher than that of the EU (2.1%), Germany (2.0%) and France (1.1%) in February 2026. The last time the UK rate was lower than the rate for the EU overall was December 2024”.

Figure 1: CPI, goods, services and core annual inflation rates, UK, February 2021 to February 2026

Source: ONS, GLA Economics

Looking at the data in more detail the ONS observed that “clothing made the largest upward contribution to the monthly change in … [the CPI annual rate]; motor fuels made the largest, offsetting, downward contribution”. Beyond the headline inflation figure other inflation measures stayed relatively steady. Core CPI (excluding volatile energy, food, alcohol and tobacco prices) inflation stood at 3.2% over the year to February 2026, up from 3.1% in January 2026. The CPI goods annual rate was unchanged at 1.6%. And the CPI services annual rate slowed slightly to 4.3% in February down from 4.4% in January.

UK GDP growth remains weak

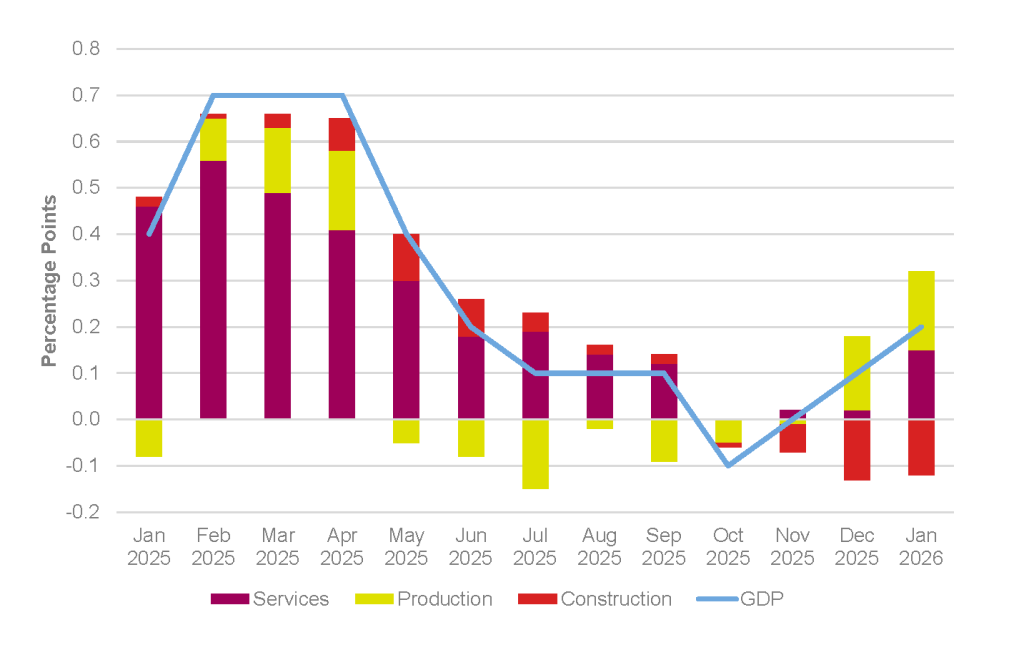

The ONS has also this month published data on the UK economy which showed that it has continued to grow sluggishly. The data shows that GDP grew by 0.2% in the three months to January 2026 after growing by 0.1% in the three months to December and not growing at all in the three months to November (Figure 2).

Figure 2: UK real three-month GDP growth, January 2025 to January 2026

Source: ONS

On a monthly basis GDP didn’t grow at all after growing by 0.1% in December and 0.2% in November. This compares to an expectation of 0.2% growth from polled economists. Looking at the three-monthly data in more detail the ONS observes that the services sector, an important sector for London, grew by 0.2% in the three months to January 2026, after not growing in the three months to December. The production sector saw growth of 1.3% in the three months to January 2026. However, the construction sectors shrunk with its output falling by 2.0% over the three months.

The ONS also observed that “looking over the longer term, GDP is estimated to have grown by 0.9% in the three months to January 2026, compared with the three months to January 2025. Services grew by 0.9%, production grew by 1.0%, and construction fell by 0.3% over this period”.

Devolved mayors could be given control over some tax revenue

In a lecture earlier this month the Chancellor said that she has asked Treasury officials to work with regional mayors and business on plans to devolve some tax revenues. In her Mais Lecture, at the Bayes Business School, the Chancellor said “they will look at income tax alongside other taxes, with reforms initially targeted at those places that have the greatest capacity to deliver them and the greatest potential to benefit”. Further details of this work will be outlined in the Autumn Budget. The plans are part of wider Government plans to grow the economy including closer ties to the EU and support for new technologies including AI and quantum computing.

GLA Economics will continue to monitor these (and other) aspects of London’s economy over the coming months in our analysis and publications, which can be found on our publications page and on the London Datastore.