London's Economy Today editorial - July 2025

UK’s GDP contracts for a second month in a row in May

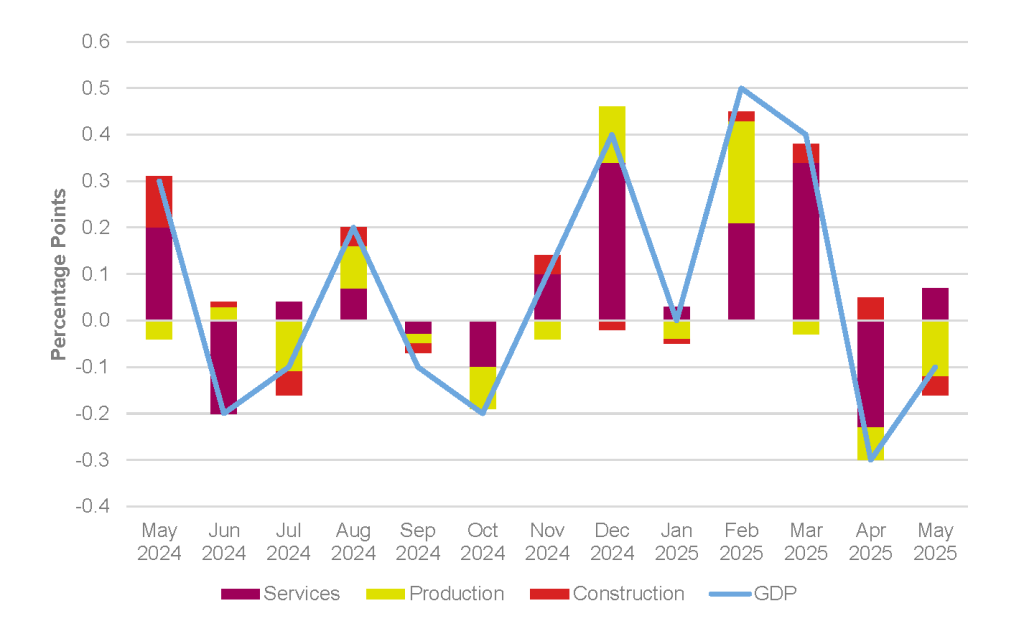

The latest monthly UK GDP data from the Office for National Statistics (ONS) showed an unexpected contraction of 0.1% in May 2025 (Figure 1). This was the second monthly decline in a row following a 0.3% drop in April and was counter to the expectations of polled economists who had expected a 0.1% expansion.

Figure 1: Contributions to monthly UK GDP growth, May 2024 to May 2025

Source: GDP monthly estimate from the ONS

Looking at the main components of GDP only services saw growth in May with its output increasing by 0.1% after declining by 0.3% in April. Output in the production sector fell by 0.9% in May after falling by 0.6% in April. Construction output declined by 0.6% in May after growing by 0.8% in April. Still, looking at a slightly longer time period the ONS notes that “real GDP is estimated to have grown by 0.5% in the three months to May 2025, compared with the three months to February 2025, largely driven by growth in the services sector in this period”.

UK inflation unexpectedly rises

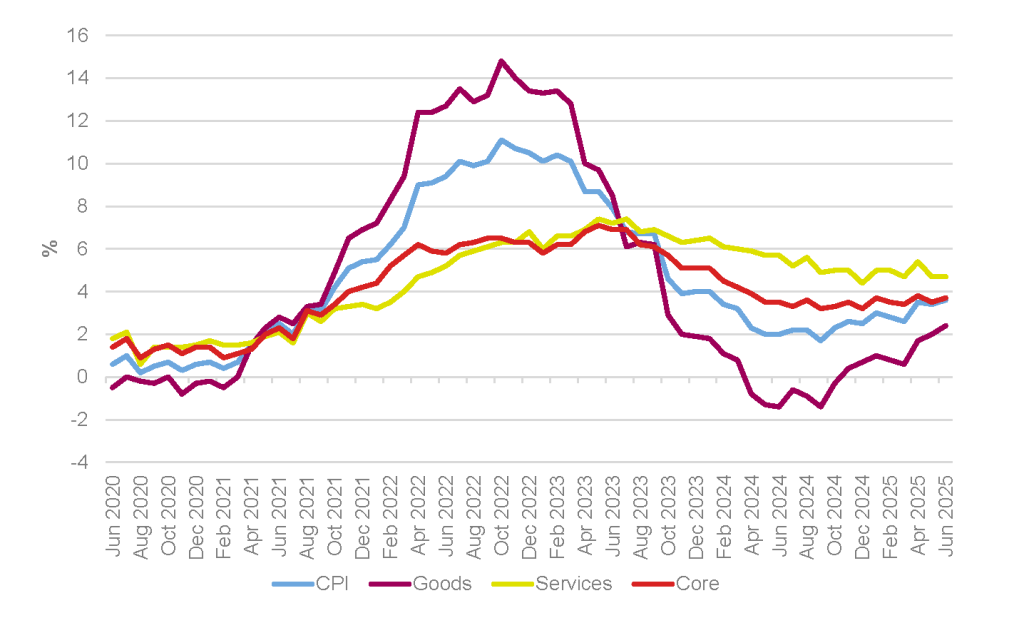

The ONS has also published data on June’s Consumer Price Index (CPI) inflation this month. This showed that CPI inflation increased to 3.6% in the 12 months to June 2025, up from 3.4% in the 12 months to May (Figure 2). This was higher than expected by most surveyed economists who had anticipated it to stay at 3.4%. Inflation now stands at an 18-month high and continues to remain significantly above the Bank of England’s central symmetrical target of 2% ±1%.

Figure 2: CPI, goods, services and core annual inflation rates, UK, June 2020 to June 2025

Source: ONS, GLA Economics

Looking at the data in more detail the ONS observed that the largest upward contribution to inflation came from “transport, particularly motor fuels”. Beyond the headline inflation figure other inflation measures generally rose. Core CPI inflation (excluding volatile energy, food, alcohol and tobacco prices) rose to 3.7% over the year to June 2025, up from 3.5% in May. The CPI goods annual rate rose to 2.4% up from 2.0%. However, the CPI services annual rate remained unchanged at 4.7%.

The OBR highlights some long-term fiscal risks

The Office for Budget Responsibility’s (OBR) Fiscal Risks and Sustainability Report (FSSR) is an annual assessment of the long-term risks and pressures to the UK’s public finances. The latest report was published this month and highlights two key issues of particular relevance to London:

- Demographic Pressures & Pensions: the report discusses how the UK’s ageing population will raise spending pressures in the long run, projecting pension and health costs to increase their share of public expenditure to roughly 26% of GDP by 2070 (up from roughly 15% in 2025). While London’s median age is lower than the UK average, the falling ratio of working-age to retired residents in the UK will impact London through (1) changes to national redistributive funding formulas, leading to more of London’s fiscal surplus being used to meet the rest of the UK’s rising pensions bill, and (2) relative falls in GLA (and other regional) grant settlements.

- Public Sector Balance Sheet & Investment: this edition of the FSSR was also the first to place Public Sector Net Financial Liabilities (PSNFL) as the “replacement yardstick for Public Sector Net Debt” – and use it as a headline measure for long-term fiscal risk. Given the volume of public investment in London, this shift in measurement puts major infrastructure schemes under tighter scrutiny. Project costs and impacts will now need framing beyond annual cost, and on their impact on the UK’s whole balance sheet over time. This will in theory lead to Treasury funding for London’s infrastructure projects being more competitive, prioritising initiatives with demonstrable, lasting productivity benefits that offset their long-term fiscal risks.

The Government announces that it will abolish Ofwat

This month, the government unveiled “the most significant reform to water regulation since privatisation”. Ofwat is set to be abolished, with its responsibilities (alongside those of the Environment Agency, Natural England and the Drinking Water Inspectorate) consolidated into a single regulator. This reset aims to improve investment, fast-track infrastructure funding and ultimately lower costs for consumers, but the sector hasgone through institutional resets and reshuffles before – and meaningful change will depend on the new regulator’s willingness (and capacity) to enforce standards and resist regulatory capture.

The reset is seen as in part a response to Thames Water’s financial issues – and the new regulator is expected to (in time) help stabilise Thames Water by providing clearer, more supportive rules for recapitalisation. London’s wider water system faces severe strain from ageing infrastructure, frequent sewer overflows, and rising flood risk – and the new regulator’s aims to “cut through planning bottlenecks” and unlock new investment will benefit upgrades like the Thames Tideway Tunnel and flood resilience works. It is, however, likely that the initial transition period will hamper investment activity in the short-term due to regulatory uncertainty. For consumers, the change has come with repeated commitment that the new regulator is to “stand on the side of customers”, giving it a mandate to control bills, allocate resources equitably, and ensure value for vulnerable groups.

IMF turns slightly more upbeat on global growth

The International Monetary Fund (IMF) has released its July 29 update to their World Economic Outlook forecast, offering a cautiously optimistic view of the global economy and a modestly improved outlook for the United Kingdom.

Globally, the IMF attributes its slightly upgraded growth forecast for 2025 and 2026, now projected at 3.0% and 3.1% respectively, to the front-loading of economic activity prompted by US tariff announcements. Businesses and consumers accelerated production and spending to get ahead of potential trade disruptions. The tariffs that were ultimately implemented turned out to be milder than expected, while a weaker US dollar and looser global financial conditions helped reduce borrowing costs, particularly in emerging markets. In addition, fiscal expansion in several major economies contributed further to short-term global demand.

For the UK, the IMF raised its 2025 GDP growth forecast from 1.1% in its April forecast to 1.2% now, with growth expected to reach 1.4% in 2026, making it the third fastest-growing G7 economy, behind the United States and Canada. The IMF also mentions that the UK’s monetary policy path is expected to be shallower, and the Bank of England will continue easing interest rates, with around two more cuts expected this year. However, it warned that persistent productivity challenges and heightened uncertainty could continue to weigh on the medium-term outlook.

Looking ahead, the IMF notes that risks to the global outlook remain tilted to the downside. These include renewed tariff increases, prolonged trade uncertainty, geopolitical disruptions, and tighter financial conditions—any of which could weaken growth and trigger market volatility. Nonetheless, upside potential exists if trade negotiations lead to greater predictability, inflation continues to ease, and structural reforms are effectively implemented.

London business confidence falls amid rising economic pressures

Business confidence in London fell into negative territory in Q2 2025 for the first time since Q2 2023, according to the Institute of Chartered Accountants in England and Wales (ICAEW) latest Business Confidence Monitor. The index dropped to -6.7, notably below both the national average (-4.2) and London’s historical average (+5.7). Despite relatively strong growth in domestic sales and exports, sentiment weakened significantly due to intensifying concerns about a rising tax burden and heightened global trade uncertainty.

This weakening of confidence was echoed by Novuna Business Finance, which found that optimism among London’s small businesses dropped sharply from 48% last quarter to 37% in July. Official ONS data also pointed to a slowdown in the capital, with London’s unemployment rate standing at 6.2% in the three months to May up 1.0 percentage points on the year although this was down on the previous quarter. And the London Quarterly Economic Survey Q2 2025 by the London Chamber of Commerce and Industry (LCCI) found that “after a brief reprieve in Q1, the proportion of London businesses reporting a rise in business costs increased across all key areas in Q2”. However, by contrast, the Lloyds Business Barometer highlighted a more positive outlook with a sharp gain in business confidence in London.

The contrasting trends across London’s business landscape underscore the complexity facing policymakers. While larger firms maintain cautious optimism about staffing and investment, smaller enterprises and key service sectors are under significant pressure.

GLA Economics will continue to monitor all these and other aspects of London’s economy over the coming months in our analysis and publications, which can be found on our publications page and on the London Datastore.