London's Economy Today editorial - January 2026

UK inflation picks up in December

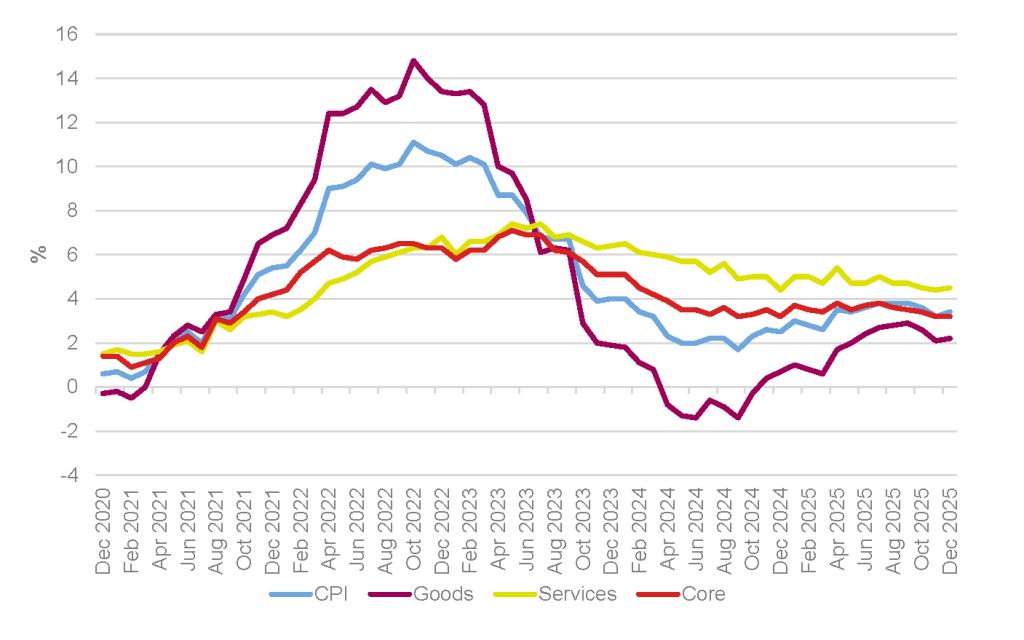

The Office for National Statistics (ONS) published data on December’s Consumer Price Index (CPI) inflation this month. This showed that CPI inflation rose by 3.4% in the 12 months to December 2025; up from 3.2% in November (Figure 1). This was higher than expected by most surveyed economists who had anticipated it to rise to 3.3%. Inflation continues to remain above the Bank of England’s central symmetrical target of 2% ±1%.

Figure 1: CPI, goods, services and core annual inflation rates, UK, December 2020 to December 2025

Source: ONS, GLA Economics

Looking at the data in more detail the ONS notes that “alcohol and tobacco, and transport made the largest upward contributions to the monthly change”. UK inflation also remains above that seen in other countries with the ONS observing that “the UK’s CPI inflation rate of 3.4% was higher than Germany’s (2.0%) and France’s (0.7%) in December. The last time the UK rate was lower than the rate in Germany was December 2024”.

Beyond the headline inflation figure other inflation measures also generally ticked up. Core CPI (excluding volatile energy, food, alcohol and tobacco prices) inflation stood at 3.2% over the year to December 2025, unchanged from November. The CPI goods annual rate increased to 2.2%, up from 2.1%. While the CPI services annual rate rose slightly to 4.5% in December up from 4.4% in November.

UK GDP returned to growth in November

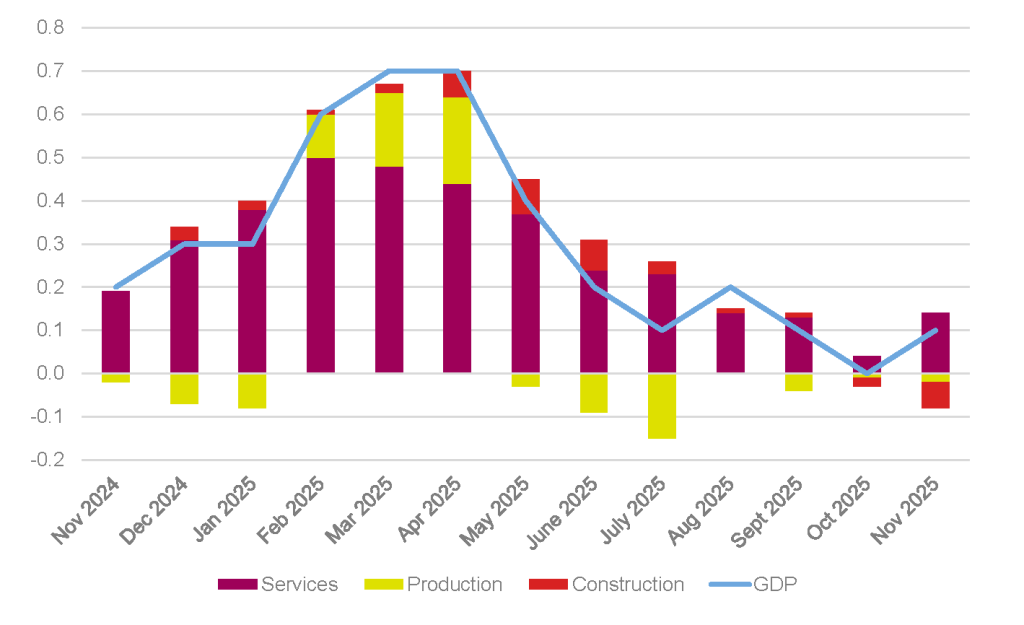

The ONS also published data this month which showed that the UK economy returned to growth in November. Output grew by 0.1% in the three months to November 2025 after not growing (revised up from a contraction) in the three months to October (Figure 2).

Figure 2: UK real three month GDP growth, November 2024 to November 2025

Source: ONS

On a monthly basis GDP grew by 0.3% in November after falling by 0.1% in October and growing by 0.1% September. This compares to an expectation of 0.1% growth from polled economists. Looking at the three-monthly data in more detail the ONS observes that the services sector, an important sector for London, grew by 0.2% in the three months to November 2025, after growing by an upwardly revised 0.1% in the three months to October. However, both the production and construction sectors shrunk over the three months to November by 0.1% and 1.1% respectively following falls of 0.1% and 0.3% in the three months to October. Compared to November 2024 GDP is estimated to be 1.3% higher in November 2025.

The IMF forecasts UK economic growth this year, while inflation returns to target

The latest IMF World Economic Outlook Update (January 2026) forecasts UK growth at 1.4% for 2025, 1.3% for 2026, and 1.5% for 2027 – these forecasts are unchanged from its October forecast. Growth in the Eurozone is forecast at a near-identical trajectory of 1.4% for 2025, 1.3% for 2026, and 1.4% for 2027. Global growth is projected at 3.3% for 2026, revised upwards by 0.2 percentage points (pp) due in part to (1) increased Asian exports of semiconductors and related manufacturing equipment, and (2) increased “AI-related investment in both hard and soft infrastructure” by the US.

UK inflation, which rose last year partly due to one-off regulatory price changes, is forecast to return to the Bank of England’s 2% target by the end of 2026, as a softening labour market eases wage growth and thus domestic inflationary pressures. Eurozone headline inflation is already hovering around 2%, while US inflation is not expected to return to 2% until 2027. Monetary policy reflects these inflationary paths: the Bank of England and Federal Reserve are expected to continue cutting rates (though more gradually in the US) while the European Central Bank is expected to hold steady.

Growth in global trade volumes is expected to slow from 4.1% in 2025 to 2.6% in 2026, as front-loading (i.e., the rush to move goods ahead of anticipated tariffs) unwinds and trade flows adjust to shifting policies. In its forecast, the IMF stresses the downside risk of growth driven by a handful of US technology firms. If AI fails to deliver expected productivity gains, a sharp price correction could follow – tightening credit conditions and hitting household wealth. Under this IMF scenario, this combination reduces global growth by 0.4 pp.

London’s financial services (responsible for roughly a quarter of London’s overall output) are embedded in the global AI investment cycle – with its investment banks, law firms, and asset managers underwriting debt and managing portfolios that are increasingly weighted towards US tech firms. A sharp correction in AI-related asset prices would hit London through rising business uncertainty, tightening credit conditions, and falling fee incomes (and thus financial services output). London’s degree of exposure depends on the compositions of portfolios across its firms (data on which is not publicly available) – but the direction is clear. Although some firms have started to hedge against US tech firm exposure, the capital’s asset managers run globally diversified portfolios as standard. If a price correction happens, spillovers to the capital’s financial sector seem likely.

London’s labour market remains soft

The data for London’s labour market continues to be soft with the number of payrolled employees living in London falling again in December, with younger workers and those living in inner London boroughs seeing the steepest falls over the last year. Nominal pay growth for employees ticked up in December on an annual basis but recent months have seen real pay drop. The timely estimate of payrolled employees (which is subject to revision) showed a decrease of 10,700 (-0.2 pp) in the number of payrolled employees in London between November and December 2025, and a decrease of 1.1% on the year. London also saw a decline in the less timely measure of the employment rate, while the unemployment rate in London rose close to its pandemic-era high. However, London’s inactivity rate (the measure of those not looking and/or not available to work) was estimated at 20.3%. This was a decrease of 0.1pp on the previous year, and a decrease on the quarter. It is lower than the UK-wide estimate of 20.8%.

GLA Economics will continue to monitor these (and other) aspects of London’s economy over the coming months in our analysis and publications, which can be found on our publications page and on the London Datastore.