London's Economy Today editorial - February 2026

UK GDP grows sluggishly at the end of the year

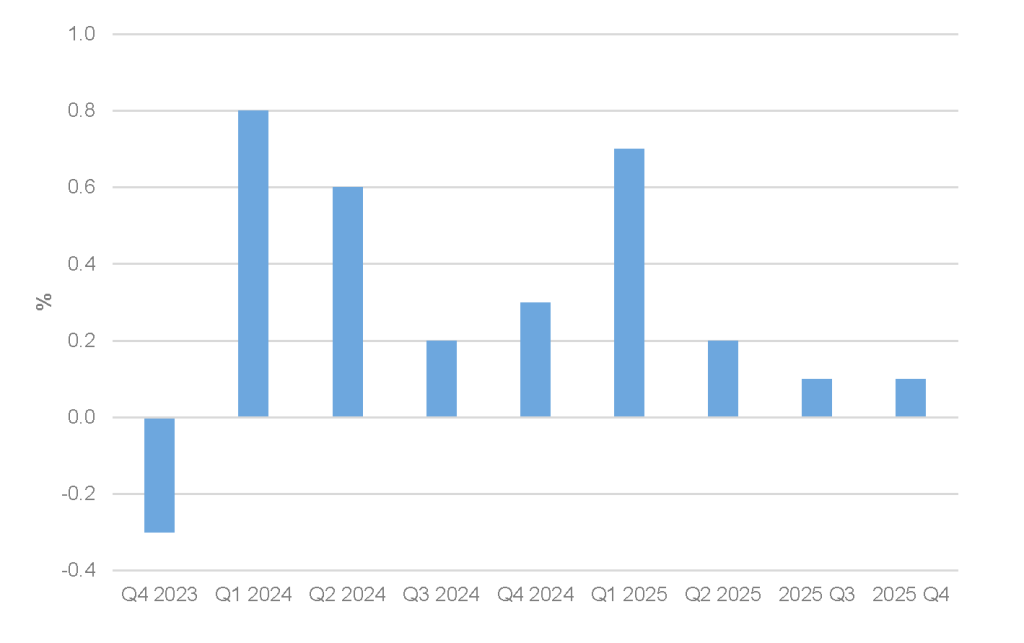

Data published this month by the Office for National Statistics (ONS) showed that the UK economy continued to grow at the end of 2025. Output increased by 0.1% in Q4 2025 after also growing by 0.1% in Q3 2025 (Figure 1). This rate of growth was slower than the average expected from surveyed analysts who had anticipated the economy to grow by 0.2%.

Figure 1: UK real quarterly GDP growth, Q4 2023 to Q4 2025

Source: ONS

On an annual basis GDP is estimated to have grown by 1.3% in 2025 as a whole, slightly faster than the 1.1% annual growth seen in 2024.

Looking at the major sectors of the economy the ONS observes that the services sector, an important sector for London, did not grow in the final quarter, while the construction sector fell by 2.1%. However, the production sector saw growth of 1.2%.

Compared to the same quarter a year earlier GDP is 1.0% higher. But real GDP per head contracted for the second quarter in a row with it declining by 0.1% after falling by the same amount in Q3 2025. Still compared to the same quarter a year earlier GDP per head was 0.6% higher and is estimated to have increased by 1.0% in 2025 as a whole, following no growth in 2024.

UK inflation falls back sharply in January

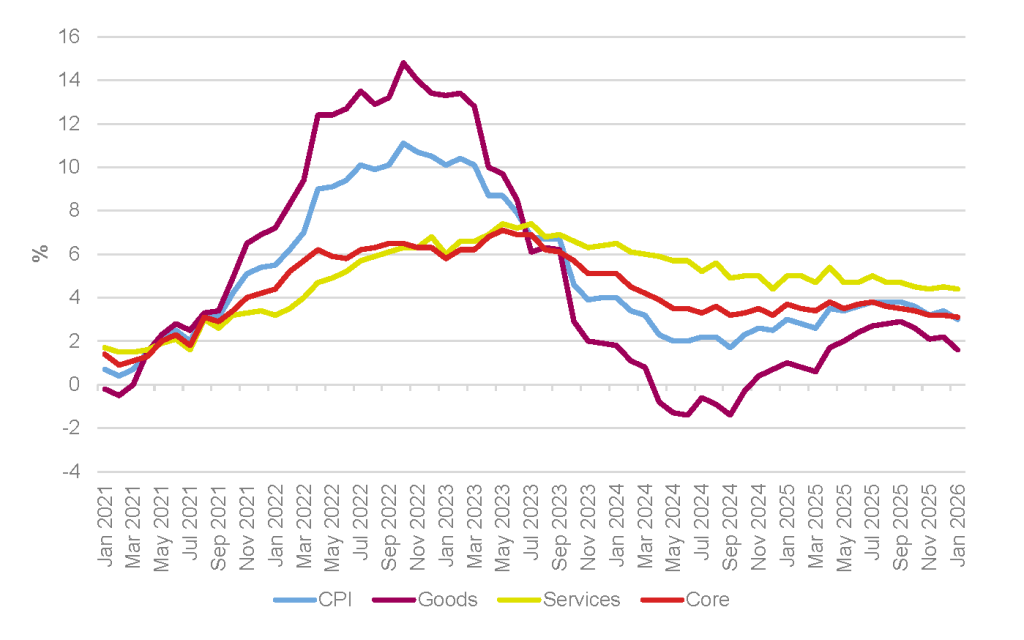

The ONS also published data on January’s Consumer Price Index (CPI) inflation this month. This showed that CPI inflation slowed to 3.0% in the 12 months to January 2026; down from 3.4% in December 2025 (Figure 2). This was in line with the estimations of most surveyed economists who had expected it to fall to this level. Inflation remains above the Bank of England’s target of 2% but is now just within the margin for fluctuation of ±1% around this central symmetrical target.

Figure 2: CPI, goods, services and core annual inflation rates, UK, January 2021 to January 2026

Source: ONS, GLA Economics

Looking at the data in more detail the ONS noted that “transport, and food and non-alcoholic beverages made the largest downward contributions to the monthly change”. UK inflation however remains above that seen in other countries with the ONS observing that “the UK’s CPI inflation rate of 3.0% was higher than that of Germany (2.1%) and France (0.4%) in January. The last time the UK rate was lower than the rate in Germany was December 2024”.

Beyond the headline inflation figure other inflation measures also dropped back. Core CPI (excluding volatile energy, food, alcohol and tobacco prices) inflation stood at 3.1% over the year to January 2026, down from 3.2% in December 2025. The CPI goods annual rate slowed to 1.6%, down from 2.2%. And the CPI services annual rate slowed slightly to 4.4% in January down from 4.5% in December.

While in forward looking inflation and cost of living news household energy costs are set to fall with Ofgem announcing a decrease in the energy price cap from April. The new cap will mean a typical annual household energy bill for a dual-fuel customer paying by direct debit will cost £1,641, a decrease of £117, or 7%, from the current level.

Bank of England holds interest rates at 3.75% while expecting inflation to soon hit target

The Bank of England’s Monetary Policy Committee (MPC) voted 5–4 to hold the Bank Rate at 3.75% in February, with four members preferring an immediate cut to 3.5%. The accompanying Monetary Policy Report marks a notable shift in tone: the balance of risks has moved away from persistent inflation towards weaker demand.

The MPC expects CPI inflation to fall to 2.1% by Q2 2026 – a 0.7 percentage point (pp) revision downwards from November’s forecast. Much of that reflects the energy bills package announced in Budget 2025, which alongside falling wholesale gas prices will bring the Ofgem price cap down in April. Governor Bailey noted that “we now expect inflation to be back to our 2% target this spring”. On pay, they stated that private sector earnings growth has already slowed and is projected to ease further by mid‑2026. The growth picture is also subdued. Underlying GDP growth was low in Q4 2025, with a modest pickup to 0.2% expected in Q1. The unemployment rate has risen to just over 5%, and the MPC now sees a wider output gap (the difference between actual and non-inflationary GDP) than it projected in November.

Dissenting MPC members pointed to cumulative forecast revisions over the past year delivering consistently lower inflation paths than previously expected, while the majority cautioned that forward-looking wage indicators remain above rates consistent with the 2% target. The path for the Market-implied rate (inferred from interest rate futures and swaps) suggest the Bank Rate will be a little above 3.3% by late 2026, implying two or three further rate cuts.

UK FDI is strong, but growth gains depend on project delivery claims new report

A new report from McKinsey argues that delivered foreign direct investment (FDI) can help support UK growth and create wider productivity gains across the economy. It places this in the context of the UK’s longer-term challenges: weak productivity growth, low investment, and limited capital deepening, which have all weighed on economic performance.

A key point in the report is its measurement approach. It focuses on announced greenfield FDI (new projects that add productive capacity), rather than total FDI flow data. The report uses this measure because it is more forward-looking, but it also clearly notes the limitation: announced projects can be delayed, scaled back, or cancelled, so announcements are not the same as completed investment.

The report finds that the UK remains one of the world’s top destinations for announced greenfield FDI, with inflows significantly above pre-pandemic levels. However, it also shows that UK FDI is highly concentrated in clean energy and communications/software (including AI-related digital infrastructure such as data centres), with a growing share coming from very large “megadeals.” This reflects real strengths, but also creates risks if a small number of major projects fail to progress.

Overall, the report concludes that FDI should be treated as a “seed” for growth, not a complete solution. To maximise the benefit, the UK must improve delivery conditions, especially planning, permitting, grid access, and policy consistency, while also ensuring domestic firms, workers, and supply chains benefit from technology adoption and spillovers. In short, the report says the UK is strong at attracting investment, but the bigger challenge is converting it into broad-based, sustained growth.

US Supreme Court tariff ruling leaves UK facing a tougher deal

The US Supreme Court has struck down the administration’s use of the International Emergency Economic Powers Act (IEEPA) to impose “reciprocal” tariffs. The 6–3 ruling removes the legal basis for much of the country-specific tariffs introduced last year. The Yale Budget Lab estimates the ruling reduces the overall US effective tariff rate from roughly 16% to 9%, while the Tax Foundation estimates that over $160bn in tariffs collected under IEEPA may now be subject to refund claims – though the Court did not rule on refunds. Following the ruling, the Trump administration invoked Section 122 of the Trade Act of 1974, initially imposing a 10% blanket tariff on products from all countries, before raising the rate to 15%.

The ruling has left the UK in a weaker relative position. Under IEEPA and the Economic Prosperity Deal, the UK had effectively locked in a 10% baseline tariff on most goods, alongside carve‑outs for the automotive sector and other industrial products. The new flat 15% rate leaves the UK facing higher effective rates, although further adjustments using other, longer‑lived US trade powers are expected to follow. For now, the 15% Section 122 tariff functions as a temporary bridge, but the medium‑term aim is likely to restore similar terms to those previously negotiated. US Treasury Secretary Scott Bessent has stated that eventual replacement measures will yield “virtually unchanged tariff revenue in 2026”.

London’s unemployment rate rises

Labour market data published this month by the ONS continued to show a weakening of both the London and UK labour markets with them both recording their highest rates of unemployment in five years. This was offset to some extent by economic activity rates edging down. These changes left the employment rate in London at its lowest level since October 2023. In more detail London’s unemployment rate was estimated at 7.6%, an increase on the quarter and an increase of 1.5pp from a year earlier. The UK average was 5.2%. The employment rate in London was estimated at 73.7% for the three months ending December 2025, a decrease of 0.6pp on the same period in the previous year, and a decrease on the quarter. London’s employment rate was slightly lower than the UK average (75.0%).

GLA Economics will continue to monitor all these and other aspects of London’s economy over the coming months in our analysis and publications, which can be found on our publications page and on the London Datastore.