London's Economy Today editorial - August 2025

UK GDP growth beats expectations in second quarter

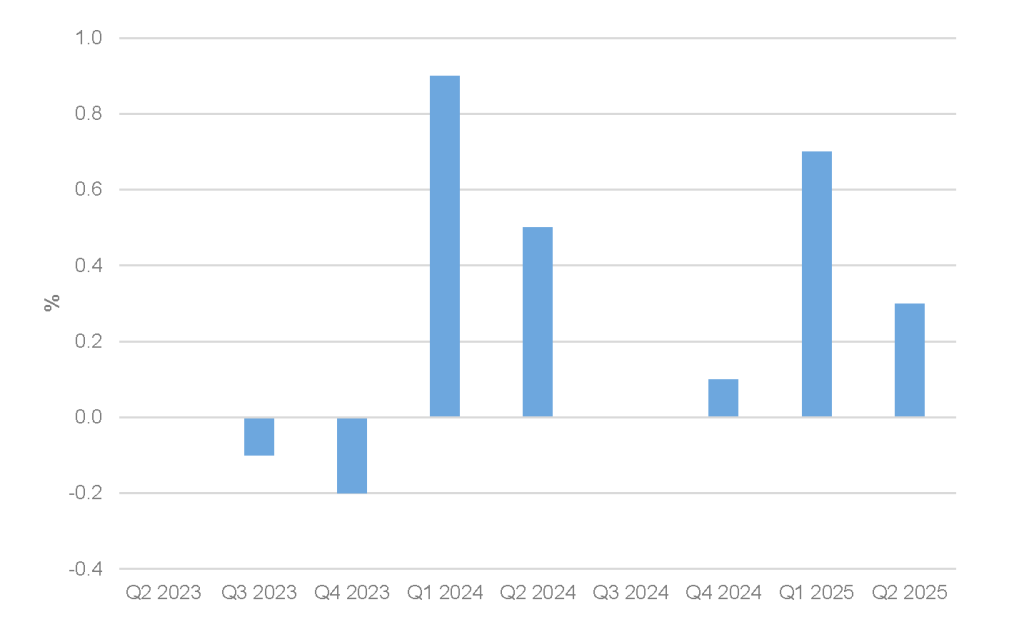

Data published this month by the Office for National Statistics (ONS) showed that the UK economy continued to grow in the second quarter of 2025. Output increased by 0.3% in Q1 2025 after growing by 0.7% in Q1 2025 (Figure 1). This rate of growth was higher than the average anticipated from surveyed analysts who had expected the economy to grow by just 0.1%.

Figure 1: UK real quarterly GDP growth, Q2 2023 to Q2 2025

Source: ONS

The ONS observes that the services sector, an important sector for London, grew by 0.4% in the quarter, while the construction sector grew by 1.2%. However, the production sector shrank by 0.3%. Compared to the same quarter a year earlier GDP is 1.2% higher and it is expected that the UK will have had the fastest annualised growth rate in the G7 for the first half of 2025. Real GDP per head also saw growth on the quarter of 0.2% and is 0.7% larger than the same quarter in 2024.

UK inflation continues to track upwards

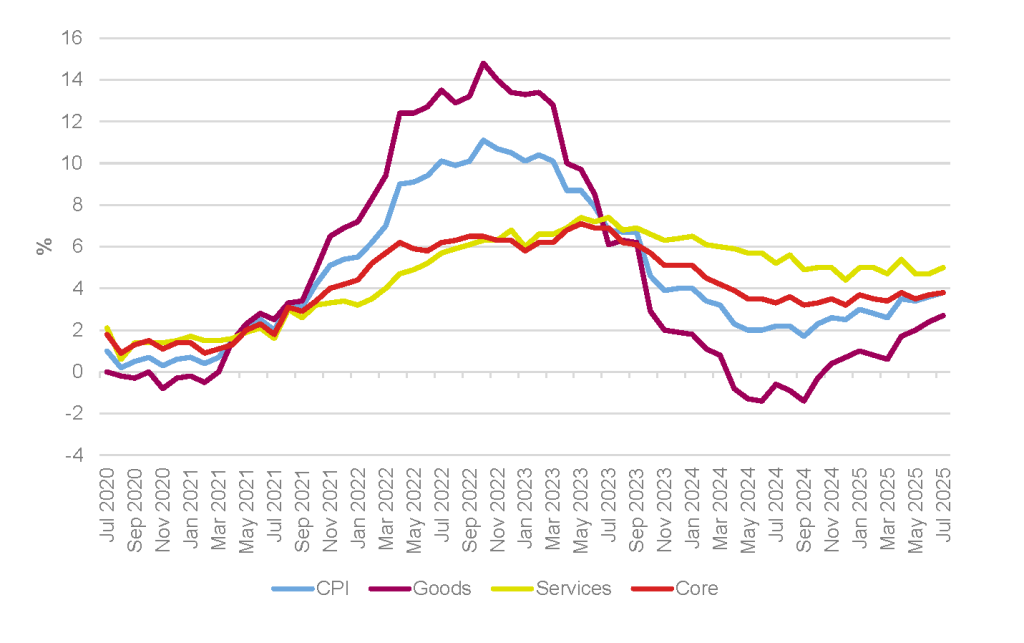

The ONS has also published data on July’s Consumer Price Index (CPI) inflation this month. This showed that CPI inflation increased to 3.8% in the 12 months to July 2025, up from 3.6% in the 12 months to June (Figure 2). This was higher than expected by most surveyed economists and UK inflation continues to remain significantly above the Bank of England’s central symmetrical target of 2% ±1%. The ONS also noted that “the UK’s CPI inflation rate of 3.8% was significantly higher than the first (or “flash”) estimate of inflation for France (0.9%) and Germany (1.8%) in July 2025”.

Figure 2: CPI, goods, services and core annual inflation rates, UK, July 2020 to July 2025

Source: ONS, GLA Economics

Looking at the data in more detail the ONS observed that “transport, particularly air fares, made the largest upward contribution to the monthly change”. Beyond the headline inflation figure other inflation measures also rose. Core CPI (excluding volatile energy, food, alcohol and tobacco prices) inflation rose to 3.8% over the year to July 2025, up from 3.7% in June. The CPI goods annual rate rose to 2.7% up from 2.4%. The CPI services annual rate climbed from 4.7% in June to 5.0% in July. The Retail Price Index (RPI) also rose and stood at 4.8% in July. The July RPI rate is often used by the government to set train fare increases for the coming year.

In other cost of living pressures, household energy costs are set to rise with Ofgem announcing an increase in the energy price cap from October. The new cap will mean a typical annual household energy bill for a dual-fuel customer paying by direct debit will cost £1,755, an increase of £35 from the current level of £1,720.

Bank of England cuts interest rates to 4%

Despite inflation remaining above its target, the Monetary Policy Committee (MPC) of the Bank of England voted, by 5 votes to 4, to lower interest rates by a quarter of a point to 4.0% in August. This is the fifth cut in rates since the Bank started lowering rates from their recent high of 5.25%. However, the MPC observed that “to ensure inflation stays low, we will judge how far and how fast to cut interest rates”. Adding “if the economy evolves as expected, we expect to reduce interest rates further over time” although “there are risks around the path of inflation, which we will continue to assess carefully”.

The Bank also published its latest economic forecast this month. It said that inflation will likely peak at 4% in September before gradually falling back to target by 2027. While in terms of output it observed that “four-quarter GDP growth is projected to remain close to its recent average level, of around 1¼%, before picking up in the second half of the forecast period” into 2027.

Some mixed signals on US inflation

In the US, inflation held steady with consumer prices rising by 2.7% in the year to July. This was the same rate as in June. However, core inflation did pick up to its fastest rate in six months to stand at 3.1% indicating that some of the recent tariff rises may be being passed on to consumers. US wholesale prices also rose in July by 3.3% compared to a year earlier, up from 2.4% in June and significantly higher than the 2.5% expected by surveyed economists.

While in signs of a slowing economy US labour market statistics published by the Bureau of Labor Statistics (BLS) showed that only 73,000 jobs were added in July and the number of jobs added in May and June were revised down by a combined 258,000. These revisions indicate that only 106,000 jobs were added to the US economy between May and July.

Recent fiscal forecasts point to “an impossible trilemma” of problems for the Chancellor

In its latest UK economic outlook, the National Institute of Economic and Social Research (NIESR) warned that the chancellor faced an “impossible trilemma” of (1) meeting self-imposed fiscal rules, (2) maintaining spending commitments, and (3) honouring manifesto tax pledges. NIESR forecasts the government will breach its stability rule by £41 billion by 2029-30, and needs to raise an additional £51 billion in revenue to restore fiscal headroom. This counters the more optimistic headroom projected in March by the OBR.

With departmental budgets already agreed and strong internal resistance to further welfare cuts, tax rises now seem almost unavoidable. NIESR highlights (but does not explicitly recommend) that even a five-percentage-point increase in basic and higher rates of income tax could theoretically close the gap – but it is more likely that a package of “moderate but sustained” increases are on the table (e.g., extensions of income tax threshold freezes, higher employer national insurance contributions, changes to pension allowances).

Channels of impact for London are two-fold: for households, whether changes (expected to occur from 2026-28) are explicit or stealth taxes, they will reduce disposable household income, and most severely affect those nearer the bottom of the income distribution. For firms, London’s attractiveness for investment and growth will be further undermined by persistently elevated borrowing costs and investor perceptions of fiscal uncertainty.

Data centres will deliver growth, but will strain grid demand

Data centre construction in the UK is ramping up, with forecasts pointing to the number of sites in the UK growing from 500 to 600 by 2030 (a doubling in market size to roughly £17bn). London is expected to account for almost 60% of new national capacity and will remain the primary data centre hub, with 17 new centres planned for the Greater London area (and another 39 in surrounding counties) due to proximity to the capital’s finance, tech, and AI-related firms.

The expansion is projected to add £44 billion in GVA to the UK economy by 2035, by (1) enabling broad-based productivity gains and digital transformation across manufacturing, finance, logistics, and health, and (2) directly adding over 40,000 high-value operational jobs and 18,200 construction roles. However, energy demand remains the main hurdle for data centre capacity. With UK data centre power consumption forecast to rise sixfold by 2035 to 35 TWh (6% of the entire UK grid), planning frameworks will need to adapt to allow these industrial-scale developments to connect to the grid. To address these pressures, National Grid has already announced up to £35 billion of transmission upgrades over the next five years, which includes new substations for dedicated data centre clusters. Planning reforms such as classifying data centres as Critical National Infrastructure are also already underway to speed up delivery and simplify grid-application permissions.

The construction sector faces a shortfall of workers

The latest Construction Industry Training Board (CITB) workforce outlook points to continuing labour supply pressures, with UK construction needing 48,000 extra workers yearly (1.8% of the 2024 construction workforce) to meet growing demand in housing and infrastructure. There are currently more than 140,000 unfilled construction sector jobs nationwide, and a third of construction workers are set to retire by 2036. The sector’s labour force is also an ageing demographic, with 35% of the sector already over 50 and just 20% under 30 years old.

In London, the problem is exacerbated by the loss of EU labour post-Brexit, with over 200,000 European workers leaving the UK construction sector in total. Industry surveys show that tendering activity has declined, due to contractors facing the resulting high input costs and a shrunken skilled talent pool. Surveys also point to a change in the type of roles demanded, projecting that nearly half of forecasted roles required by 2029 will be in skilled trades (e.g., carpenters, joiners, and electricians), a shift away from the recent demand for professional/managerial roles.

Labour shortages (and resulting higher wage incentives) drive up costs, slow project delivery, and ultimately lead to failed infrastructure and housing targets in London. Firms are responding by expanding internal training, partnering with colleges, and recruiting more apprentices, but low completion rates remain an issue, with just under 50% of apprentices finishing their training.

IFS says that inner London boroughs could lose out in proposed funding reforms

The Institute for Fiscal Studies (IFS)published analysis this month looking at the possible impact of the proposed new system for funding councils from central government that is due to be implemented in 2026-27. This system is designed to take account of new assessments of the councils’ spending needs and their ability to fund them via council tax. There will be a three-year transition period with funding floors to limit losses for those receiving less funding under the new system. The IFS’s analysis found that councils would fair differently under these changes and that “the biggest losers are set to be inner London boroughs, and especially those in inner West London. In particular,…Camden, Hammersmith & Fulham, Kensington & Chelsea, Wandsworth and Westminster would see funding fall by over a quarter if the reforms were introduced immediately, and would all be on the lowest funding floor and so face a real-terms cut of 11–12% over the next three years even if they increased their council tax by the maximum allowed each year”. While on a regional level it found that “London is the biggest loser, with a cash-terms increase in funding of only 8% over the next three years… driven by large losses in inner London (–1%), with outer London as a whole set to fare slightly better than average (+15%)”.

GLA Economics will continue to monitor these (and other) aspects of London’s economy over the coming months in our analysis and publications, which can be found on our publications page and on the London Datastore.