London’s workforce exposure to generative artificial intelligence

Generative Artificial Intelligence (GenAI) is evolving quickly, with the potential to reshape London’s labour market. But its overall impact on employment remains uncertain. This supplement summaries the findings of recent GLA Economics research into the topic.

Introduction

How will artificial intelligence change London’s labour market? In a new GLA Economics Working Paper, ‘London’s workforce exposure to generative artificial intelligence’ we use measures of GenAI exposure at a task level to help answer this question. The publication provides high-level estimates of the degree to which different types of occupations are most likely to be affected – but we note that AI has the potential to have both positive and negative impacts on jobs and the labour market. Together with near real-time job postings and business survey data, we document changes that are already happening.

This evidence base provides a foundation for further work. The Mayor has just launched the London AI and Jobs Taskforce, established to generate more real-world evidence on how AI is affecting the capital’s labour market – and to respond with effective policy measures. Bringing together a wide range of stakeholders, it will help identify both the near-term risks and opportunities for Londoners and guide a focused set of practical policy interventions. The taskforce will take forward the analysis of this report to better understand AI-specific effects on jobs, productivity, inclusion, and job quality.

Key points

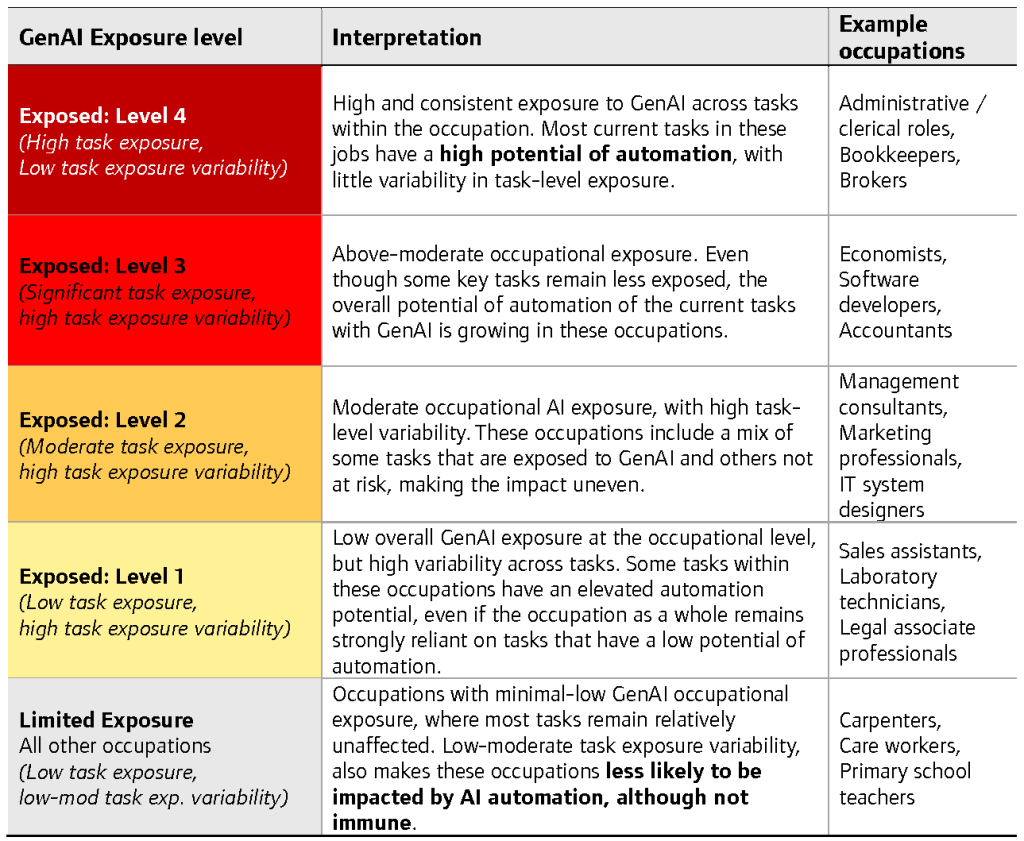

- The analysis starts by using the International Labour Organization (ILO) framework for classifying occupational exposure based on the potential for GenAI to automate tasks. All occupations are assigned to one of five levels (Table A1).

Table A1: Definitions and interpretation of GenAI exposure levels

Note: Occupational GenAI exposure scores are not forecasts of jobs losses. Rather they indicate only the technical potential for tasks within roles to be automated by GenAI.

-

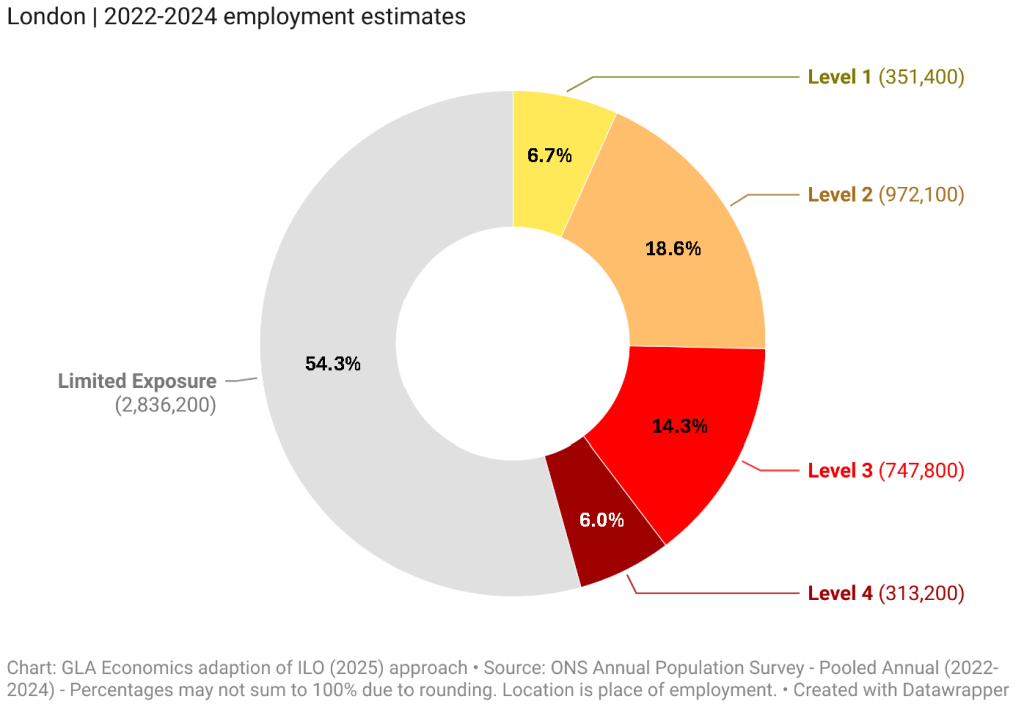

At least 46% of London’s workers (around 2.4 million people) are in roles where GenAI could automate a share of their tasks (Figure A1), based on the International Labour Organization’s (ILO) occupational exposure estimates.[1] This is substantially higher than the UK average of 38%.

However, high exposure, as defined in the report, does not signal definitive job losses, nor does low exposure guarantee job and occupational security.

- Around 6% of workers (313,000) are in Level 4, the highest-exposure group, where most tasks could be automated using current GenAI capabilities. A further 14% (748,000) are in Level 3, where exposure is high but varies across tasks, with some key tasks remaining less exposed. Together, these groups make up just over one-fifth of London’s workforce and are the most likely to experience earlier and more pronounced role changes as GenAI adoption grows.

Figure A1: Almost half of London’s workforce is in GenAI-exposed occupations

-

London’s high exposure to GenAI presents both opportunity and risk. The technology could deliver productivity gains by improving task efficiency, but it may also create a risk of disruption and reduced demand for some roles, even while increasing the need for some new or existing roles.

In addition to the technology’s capabilities, longer-term GenAI labour market impacts will depend on a range of other factors, including adoption patterns, the availability of complementary skills, public trust in AI outputs and business integration strategies, as well as wider economic conditions.

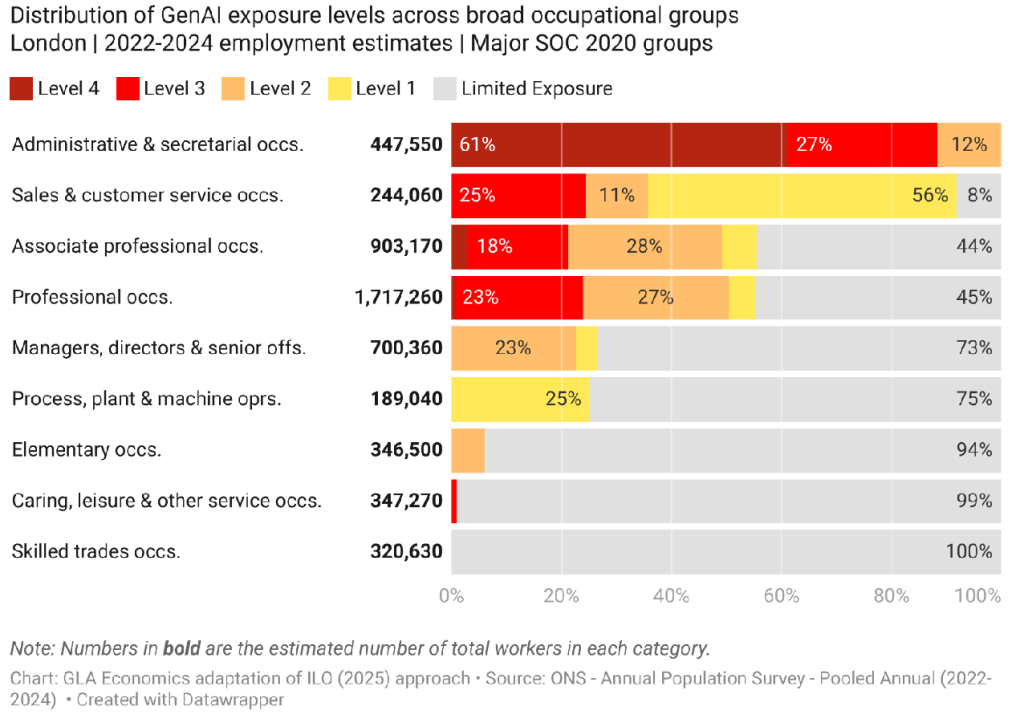

- GenAI exposure – and its potential impact – is heavily concentrated within specific occupations and industries. Over 300,000 workers – predominantly in routine administrative roles – face the highest levels of exposure and risk of AI automation, as their clerical tasks align most closely with GenAI capabilities (Figure A2). Many professional white-collar occupations are also highly exposed, reflecting the language-, digital- and analysis-intensive nature of their work. However, roles requiring high-stakes judgement, accountability and client interaction are considered by the ILO measures to be less directly automatable. They are more likely to be reshaped through augmentation than replaced by GenAI.

Figure A2: Administrative roles at most risk of GenAI disruption, with large numbers of workers in professional roles also exposed

- ICT, finance, professional services, and public administration sectors face the highest overall exposure to GenAI. There are industries that are fundamental to London’s economy. Sectors that rely on physical presence, skilled trades, or direct interpersonal care are less directly exposed, though no sector is likely to remain entirely unaffected. Some sectors with relatively low direct exposure to GenAI – such as transport – may see faster change in the future when other forms of AI such as computer vision advance, increasing the potential of robotics and other automation technologies.

- Exposure estimates suggest uneven impacts are likely across London’s workforce. Differences in exposure across groups largely reflect existing occupational patterns, although no group is entirely insulated from potential effects. Workers with higher levels of educational attainment are among the most exposed, reflecting their concentration in professional, knowledge-intensive occupations. Women are overrepresented in highly exposed administrative and clerical roles.

- Many younger workers, those at the start of their professional careers, are concentrated in high-exposure digital and knowledge-intensive roles. GenAI may also affect “stepping-stone” jobs that traditionally provide entry routes into careers, with implications both for young people trying to gain a foothold in the labour market and for longer-term talent pipelines into more senior roles.

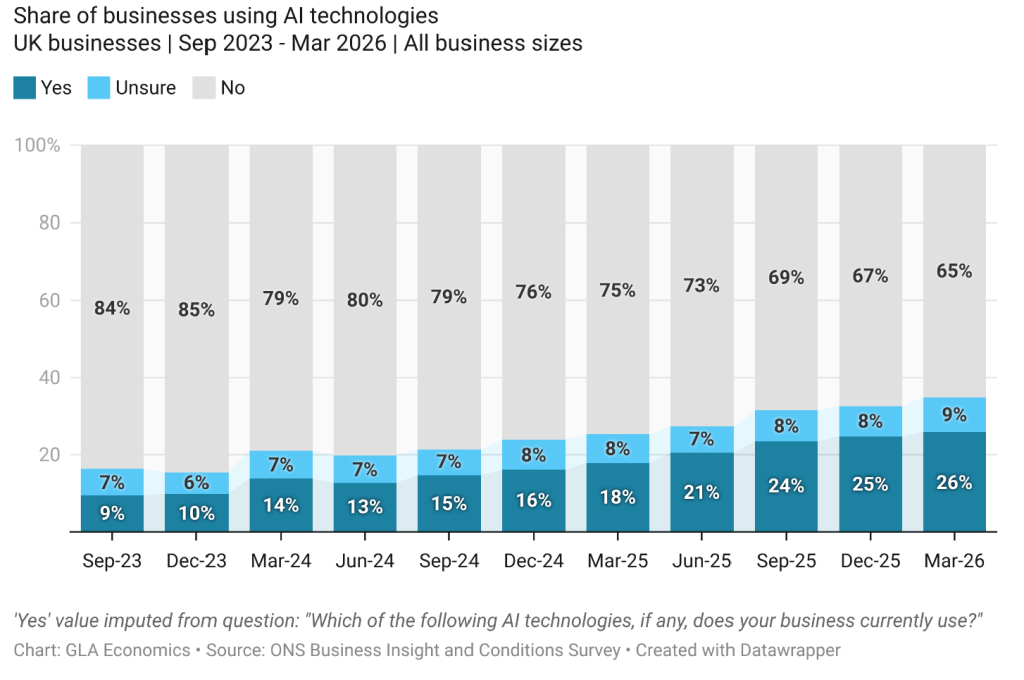

- Exposure alone does not drive labour market change, but early signals from GenAI adoption trends suggest it is beginning to translate into tangible workplace impacts. Worker- and business-reported AI adoption has almost doubled over the last two years to between 26%-35% and continues to steadily rise as use cases become clearer, particularly in highly exposed knowledge-intensive sectors (Figure A3).

Figure A3: AI adoption rates are rising steadily among UK firms

- Adoption (and intensity of adoption) remains uneven, with larger and more digitally mature businesses leading the uptake. Organisations’ ability to manage change and the risks around data protection, quality, and accountability may be slowing use in some settings.

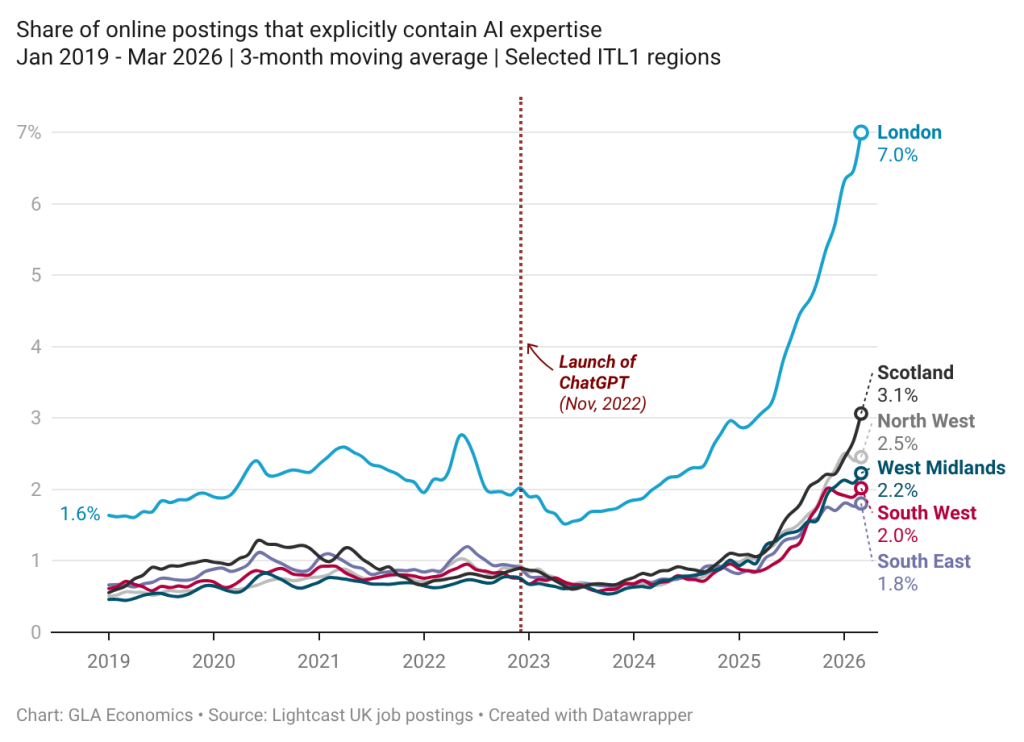

Figure A4: Employer demand for AI skills is growing exponentially, particularly in London

- So far, task change within roles appears to be the main employment effect, with early adoption evidence to date pointing to tentative productivity gains, sub-task automation and role redesigns, rather than wholesale job replacement with AI. Business-reported impacts of AI adoption on specific roles broadly align with the ILO’s occupational exposure patterns, with limited evidence of changes in headcount. Firms report prioritising training and upskilling of existing staff in complementary skills, and increasingly expect AI expertise when recruiting across a wide range of occupations.

- Job postings evidence aligns with rising adoption trends. Demand for specialist AI roles is growing rapidly, although these jobs remain a relatively small part of the overall labour market, while AI-focused firms are also expanding quickly, generating new employment opportunities. By end of March 2026, 7% of London’s online job postings were explicitly seeking AI-related skills from prospective candidates (Figure A4).

- Demand may be softening for some highly exposed roles in administration and some professional services, but the evidence remains inconclusive. The slowdown may partly reflect AI-related change, but it remains difficult to disentangle these effects from the wider labour market cooling of recent years. While reported AI-related headcount reductions remain limited to date, employers in some industries anticipate that automation-related efficiencies arising from AI adoption will allow them to reduce their hiring needs or workforce size over time.

Conclusions

London’s potential exposure to GenAI is relatively high, reflecting the capital’s concentration of professional and knowledge-intensive work. However, exposure is not a forecast of job losses, but an indication of where job content is most likely to change.

The data suggests that employers are increasingly using GenAI to support workers and automate parts of jobs – such as drafting, summarising, analysis and routine processing – rather than replacing whole roles at this stage. This aligns with the expectation that, at least initially, GenAI is more likely to be complementary: it is driving task reallocation and augmentation in many occupations, with displacement risk more concentrated in a narrower set of routine roles.

Overall, early evidence points to several dynamics occurring in parallel: (i) changing task content within existing jobs, (ii) the emergence of new AI-related specialist roles, and (iii) early signs of softer labour demand in some highly exposed routine administrative occupations

This report serves as a foundational evidence base on what is increasingly becoming a pivotal issue for businesses and policymakers alike. The analysis presented in the report, while rigorous, is preliminary given the nature and evolution of GenAI’s capabilities.

[1] Classified as exposed to GenAI (exposure levels 1–4), see appendix in report for detail on the exposure levels.