London's Economy Today editorial - December 2025

UK GDP shrinks in October

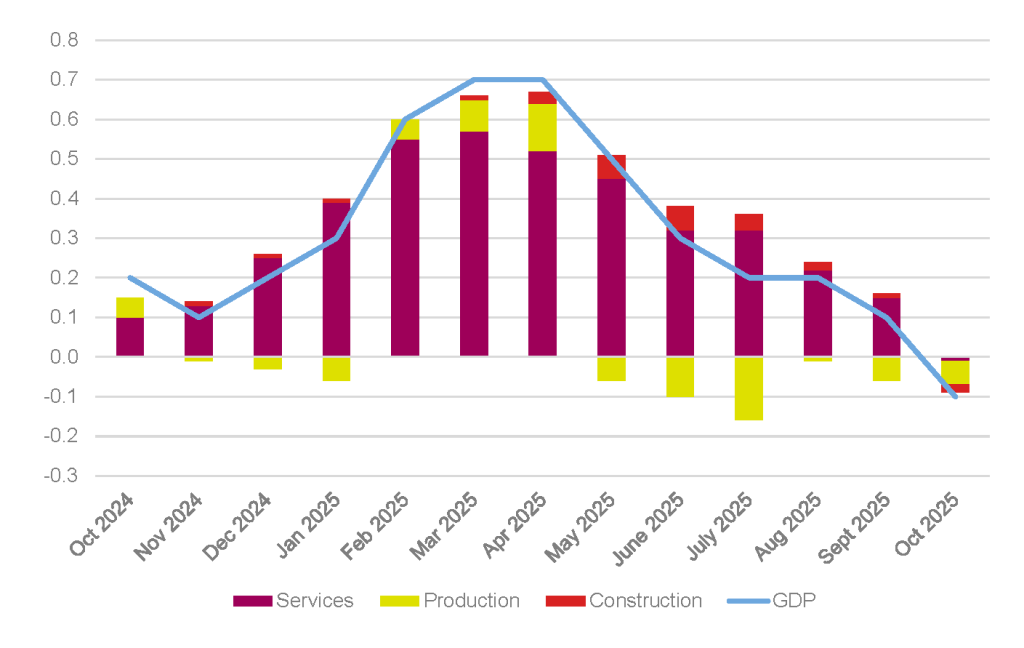

Data published this month by the Office for National Statistics (ONS) showed that the UK economy contracted in October. Output fell by 0.1% in the three months to October 2025 after growing by 0.1% in the three months to September (Figure 1). This was the first fall in three-monthly GDP since December 2023.

Figure 1: UK real three month GDP growth, October 2024 to October 2025

Source: ONS

On a monthly basis GDP also fell by 0.1% after falling by 0.1% in September and not growing in August. This compares to an expectation of 0.1% growth from polled economists. Looking at the three-monthly data in more detail the ONS observes that the services sector, an important sector for London, didn’t grow in the three months to October 2025. Also, both the production and construction sectors shrunk over the three months by 0.5% and 0.3% respectively. Still, compared to October 2024, GDP is estimated to be 1.1% higher in October 2025.

UK inflation slows further in November as the Bank reduces interest rates

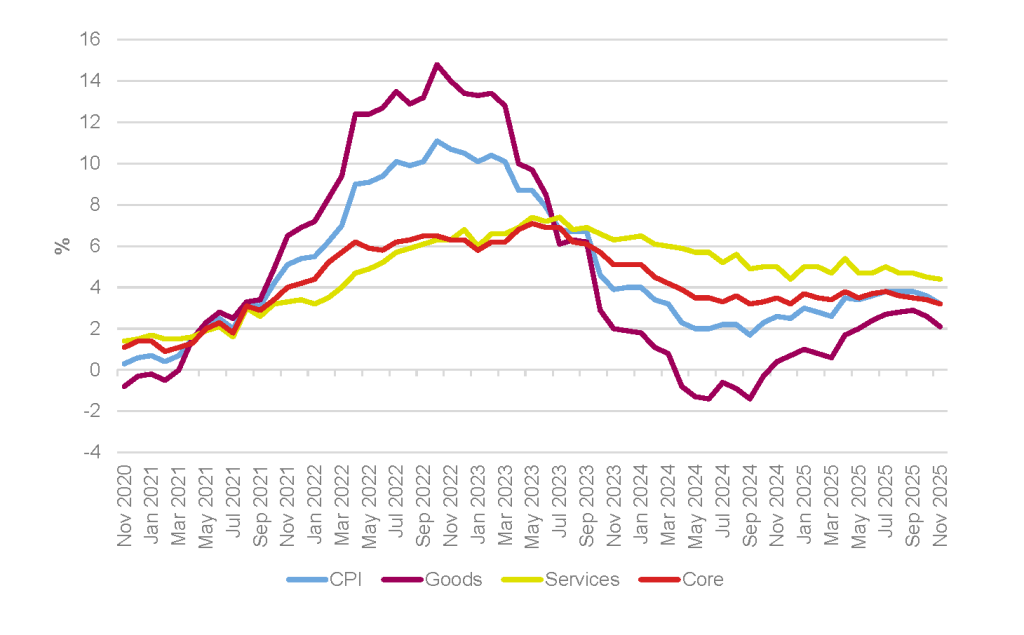

The ONS also published data on November’s Consumer Price Index (CPI) inflation this month. This showed that CPI inflation slowed to 3.2% in the 12 months to November 2025; down from 3.6% in October (Figure 2). This was lower than anticipated by most surveyed economists who had expected it to decline to just 3.5%. Inflation however continues to remain above the Bank of England’s central symmetrical target of 2% ±1%.

Figure 2: CPI, goods, services and core annual inflation rates, UK, November 2020 to November 2025

Source: ONS, GLA Economics

Looking at the data in more detail the ONS observed that “food and non-alcoholic beverages, and alcohol and tobacco made the largest downward contributions to the monthly change”. UK inflation still however remains above that seen in other countries with the ONS noting that “the UK’s CPI inflation rate of 3.2% was higher than the first (or “flash”) estimate of inflation for Germany (2.6%) and France (0.8%) in November. The last time the UK rate was lower than the rate in Germany was December 2024”.

Beyond the headline inflation figure other inflation measures also declined. Core CPI (excluding volatile energy, food, alcohol and tobacco prices) inflation slowed to 3.2% over the year to November 2025, down from 3.4% in October. The CPI goods annual rate slowed to 2.1%, down from 2.6%. While the CPI services annual rate slowed slightly to 4.4% in November down from 4.5% in October.

In response to the easing of inflation and in relation to the general economic environment the Monetary Policy Committee (MPC) of the Bank of England voted to lower interest rates by 0.25 percentage points to 3.75% from 4% on 18 December. The MPC voted 5-4 in favour of this move with 4 members voting to keep the rate unchanged. Commenting on the inflationary situation they noted that although inflation remains “above the 2% target, it is now expected to fall back towards target more quickly in the near term. Reflecting restrictive monetary policy, and consistent with evidence of subdued economic growth and building slack in the labour market, pay growth and services price inflation have continued to ease”.

The OECD forecasts modest UK growth, but highlights three key structural barriers

The OECD’s December Economic Outlook projects UK growth of 1.2% in 2026 (up from the 1.0% for 2026 that they forecast in June) and 1.3% in 2027. They forecast the deficit (the gap between public spending and revenues) to fall from 5.9% of GDP now to 5.1% by 2027 and public debt to stay above 100% of GDP – meaning total government debt will remain larger than the UK’s entire annual economic output. The OECD warns that this leaves the UK with “very thin fiscal buffers” – and unable to provide economic stimulus in a downturn without breaking fiscal rules. They identify three structural constraints to UK growth potential: low productivity growth, slow working-age population growth (partly due to reduced migration), and persistent skills mismatches.

For the United States, the OECD projects growth of 2.0% in 2025, 1.7% in 2026 and 1.9% in 2027. A sharp slowdown in net migration, coupled with average tariffs at 17% on imports (the highest “effective tariff rate” since 1935) are seen as key constraints to growth. Despite December’s Federal Reserve rate cut to a range of 3.5-3.75% (from 3.75%-4.0%), the OECD expects inflation to “rise further through mid-2026” as tariffs feed through to prices – limiting the scope for further rate cuts to stimulate growth.

For the Eurozone, growth is forecast at 1.3% in 2025, 1.2% in 2026 and 1.4% in 2027. The OECD cites increased trade frictions and geopolitical uncertainty as key drags on investment (and growth), though this is partially offset by European Central Bank (ECB) rate cuts lowering the cost of borrowing and investment. The OECD expects a looser labour market and weak demand to bring Eurozone inflation to 1.9% by 2026, allowing the ECB to keep cutting rates to stimulate growth – unlike the inflation-constrained US and UK.

Steady growth in London’s output, employment, and household finances forecast for the coming years

Twice a year, GLA Economics produces medium-term forecasts of key macroeconomic variables:

- London’s output (real Gross Value Added)

- Employment levels (total Workforce Jobs)

- Household spending (real Household Expenditure)

- Household income (real Household Disposable Income)

These forecasts are used in various internal business planning processes – and presented as central, upside, and downside scenarios. This section of London’s Economy Today outlines the key figures from the latest central scenario, which we have published this month in the latest London’s Economic Outlook.

- Annual output growth has been weak in recent years, with London’s economy growing 0.3% in 2023 and 1.1% in 2024 – but our forecast projects stronger growth in the coming years. Output is forecast to grow by 1.9% in 2025, 1.7% in 2026, and 2.1% in 2027 – a return toward pre-pandemic growth rates. In absolute terms, this takes the value of London’s output from £548bn in 2025 to £569bn in 2027 (+£21bn). This reflects easing inflation, a more stable interest rate environment, and continued expansion in London’s service sectors.

- Workforce jobs growth has been steady in recent years, growing 1.6% in 2023 and 0.9% in 2024. Jobs are forecast to grow 0.9% in 2025, 1.1% in 2026, and 1.2% in 2027. In absolute terms, this takes total jobs from 6.5 million in 2025 to 6.6 million in 2027 (+100k jobs).

- Household spending has declined over recent years, falling by 1.6% in 2023 and 2.4% in 2024 – primarily due to the persistent effects of high inflation and resulting cost-of-living pressures. As inflation eases, spending is forecast to return to growth, growing 0.6% in 2025, 2% in 2026, and 1.9% in 2027.

- Household income grew 3.2% in 2023 and 3.0% in 2024, due to sustained wage growth. Income growth is forecast to continue at 2.1% in 2025, 1.5% in 2026, and 1.3% in 2027, as the labour market loosens and wage growth slows.

The central scenario assumes no structural shocks, but three risks warrant monitoring. International risks from collapsing trade growth and tariff escalation could hit London’s globally exposed sectors. Fiscal uncertainty may weigh on business confidence and investment. And while AI adoption offers productivity gains for London’s tech-heavy economy, displacement in exposed roles has already begun.

GLA Economics will continue to monitor these (and other) aspects of London’s economy over the coming months in our analysis and publications, which can be found on our publications page and on the London Datastore.